Introduction

Every time a customer buys a service contract or extended warranty from your business, a portion of that premium leaves your ecosystem — permanently. It funds a third-party provider's underwriting profit, investment returns, and overhead. You get a commission. They keep the rest.

Extended warranty reinsurance programs give contractors and dealers a way to restructure how warranty revenue flows — keeping underwriting profits, investment income, and customer relationships inside the business instead of funding someone else's bottom line.

The U.S. auto extended warranty market alone reached $32.7 billion in revenue in 2025, which illustrates the scale of profits moving through these programs. For HVAC contractors, recurring service agreements already represent 55% of HVACR industry revenue — making the opportunity to capture reinsurance profits from that volume significant.

This article covers the program structures available, strategies to maximize profitability, how reserve funds work, and the practical steps to transition from a third-party model to one you own.

TL;DR

- Extended warranty reinsurance shifts underwriting profits and investment income from third-party providers to your business.

- Programs range from commission-only arrangements to fully contractor-owned or dealer-owned structures, each offering greater profit potential.

- The biggest profit levers are structure selection, loss ratio management, and active reserve fund investment.

- Transitioning requires an administrative partner who manages entity formation, compliance, claims, and reporting on your behalf.

- Start early — every contract written grows the reserve fund you own.

What Is an Extended Warranty Reinsurance Program?

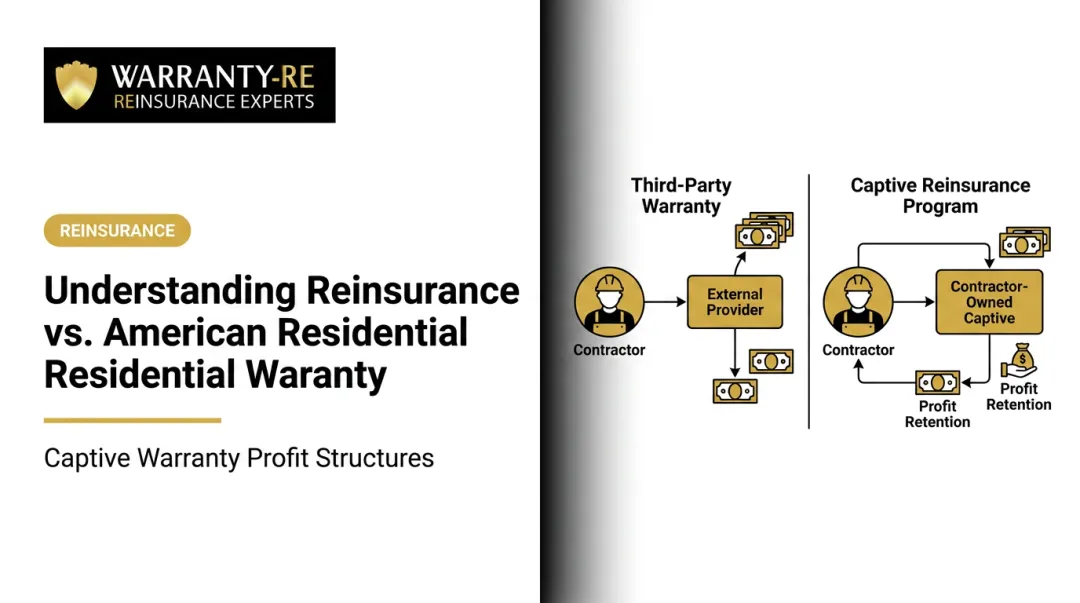

When a customer buys a service contract or extended warranty, the premium follows a predictable path: it's collected, held in reserve for future claims, and after the risk period expires, whatever remains becomes profit. The question is who keeps that profit.

In a standard third-party arrangement, the answer is the warranty provider. In a reinsurance program, you restructure that flow so your own business entity captures the reserves, investment income, and underwriting profit.

How the Premium Flow Works

The basic structure looks like this:

- Customer pays a warranty or service contract fee

- Premium flows to a fronting carrier (an A-rated insurer that provides regulatory and licensing compliance)

- The fronting carrier cedes a portion of the risk to your reinsurance entity

- Your entity holds the reserves and earns investment income while claims are still possible

- Once the risk period expires, remaining funds become earned surplus — distributable to you

The fronting carrier stays in the structure throughout, backed by A-rated insurers, meeting all regulatory and financial compliance obligations. The underwriting economics, though, belong to the business owner.

Who This Applies To

This model works for both auto dealers (vehicle service contracts, GAP, ancillary protection products) and home service contractors (HVAC, roofing, plumbing, and electrical labor warranties and service plans). The regulatory framework varies by state and structure type, but the core principle holds across both industries: whoever holds the risk captures the profit.

NAIC Model #685 defines service contracts as regulated agreements to repair, replace, or maintain property — and explicitly treats them as distinct from insurance. That distinction creates the compliance framework within which reinsurance structures operate.

Understanding Program Structure Options: From Walkaway to Contractor-Owned

Not every business starts with the same structure. The right entry point depends on volume, risk tolerance, and how much of the underwriting profit you want to keep.

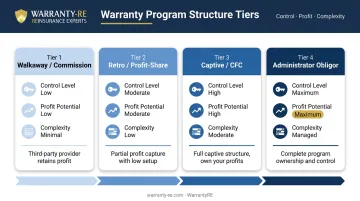

Commission-Only (Walkaway) Programs

The simplest model: you sell a third party's warranty product, earn a commission or markup, and have no participation in underwriting results. Low administrative burden, but the majority of program profit leaves your business permanently.

Retro (Profit-Sharing) Programs

A step up: the business shares in a portion of underwriting profit after claims run out, while the insurer absorbs excess losses. More upside than walkaway, but the insurer retains a significant share and sets the terms.

Reinsurance Captive Structures

Here, the business owner forms a captive entity (domestic or offshore) that accepts ceded underwriting risk from the fronting insurer. The captive holds premium reserves and earns both underwriting profit and investment income.

One relevant tax consideration: IRS Rev. Proc. 2025-32 sets the Section 831(b) premium limit at $2.9 million for tax years beginning in 2026. Property and casualty insurance companies under that threshold may elect to be taxed only on investment income — a real advantage for smaller programs.

Consult a qualified CPA familiar with captive structures before making tax elections.

Administrator Obligor / Contractor-Owned Model

The most comprehensive option. The business becomes the obligor on the warranty contract itself — not just a reinsurer of someone else's policy. A Contractual Liability Insurance Policy (CLIP) from an A-rated carrier provides the backstop if the entity cannot meet obligations. This structure gives maximum control over:

- Pricing and contract terms

- Claims handling and approval

- Customer experience

- Profit retention

WarrantyRE builds and administers this model for home service contractors and auto dealers. One common misconception: this structure requires high volume to work. It doesn't. Programs are designed to be viable across a wide range of business sizes.

Choosing the right structure:

| Structure | Control Level | Profit Potential | Complexity |

|---|---|---|---|

| Walkaway/Commission | Low | Low | Minimal |

| Retro/Profit-Share | Moderate | Moderate | Low |

| Captive/CFC | High | High | Moderate |

| Administrator Obligor | Maximum | Maximum | Managed by administrator |

Strategies to Maximize Profitability from Your Reinsurance Program

Choose the Right Structure for Your Volume and Growth Stage

Entering a structure before you have sufficient premium volume means setup costs may outweigh benefits. Staying in a commission-only model too long means compounding profit lost year after year. The progression from walkaway to retro to captive to administrator obligor follows a clear logic: each stage maps to your volume, risk appetite, and management capacity.

Work with a reinsurance administrator who can evaluate your current numbers and identify where you fit.

Control Your Loss Ratio Through Active Claims Management

Warranty Week's combined ratio analysis illustrates the mechanics clearly: a 25% expense ratio plus a 65% loss ratio produces roughly 10% underwriting profit. Adjust the loss ratio and the profit changes proportionally.

When you own the reinsurance structure, you can actively influence claims outcomes:

- Approve legitimate claims quickly to protect customer relationships

- Manage borderline or fraudulent claims more carefully than a passive third-party insurer would

- Drive warranty service calls back to your own service facility, keeping labor revenue in-house

WarrantyRE's full-service model handles claims adjudication from initial contact through resolution, while tracking performance metrics so owners can monitor their loss position over time.

Build Premium Volume Consistently to Accelerate Reserve Accumulation

Reserves compound over the life of service contracts. A consistent volume of new contracts each month creates an expanding base of invested reserves. Contracts sold today generate investment returns for years before claims exhaust them — that's the time-value advantage of building early and building consistently.

For HVAC contractors, framing service agreements as a core revenue stream rather than an afterthought positions the business to scale reserve accumulation at scale. Recurring service agreements are typically one of the largest revenue categories in an HVAC business — and the foundation that makes a reinsurance program worth building.

Price Your Warranty Products to Reflect Your Actual Risk

Third-party providers price to their own profit requirements. When you own the structure, pricing can be calibrated to your actual data — not someone else's margin targets.

That calibration creates two simultaneous advantages:

- Set prices based on your equipment failure history, service geography, and labor costs

- Stay competitive in the market while protecting program margin

- Adjust pricing over time as your claims data matures

Use the Warranty Program as a Customer Retention Engine

A contractor-owned warranty program creates recurring touchpoints that a third-party arrangement simply doesn't deliver to you:

- Annual service visits tied to maintenance agreements

- Renewal conversations at contract expiration

- Claims resolution moments where fast, fair handling builds loyalty

- Direct relationship between the customer and your brand throughout the warranty period

That combination of recurring contact and in-house service revenue is what separates a well-run warranty program from a passive product add-on.

Benchmark Program Performance Regularly

Key metrics to monitor with your administrator:

- Loss ratio — claims paid as a percentage of premiums earned

- Claims frequency — how often contracts generate claims

- Premium per contract — average warranty fee per job or vehicle

- Contract penetration rate — percentage of transactions generating warranty enrollment

- Investment yield on reserves — return on trust account assets

WarrantyRE provides monthly financial statements and performance analysis as part of their full-service model, giving owners clear visibility into program health.

Reserve Fund Investment Strategies and Tax Advantages

Investing the UPR vs. the Surplus Account

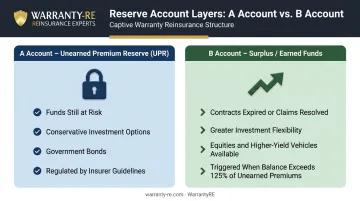

Reinsurance trust structures typically involve two account layers:

The A Account (Unearned Premium Reserve / UPR): Holds reserves still at risk for paying future claims. Investment options are conservative — typically government bonds — per insurer and regulatory guidelines. In WarrantyRE's structure, the Trust Company invests these funds in conservative instruments following restrictions set by the underwriting insurance carrier.

The B Account (Surplus / Earned Funds): Once contracts expire or run out and claims are no longer expected, those funds convert to earned surplus. Per WarrantyRE's trust structure, once balance sheet cash exceeds 125% of unearned premiums, excess funds may be invested more aggressively at the direction of company ownership. This can include equities and higher-yield vehicles.

The B account is where many business owners leave money on the table by leaving surplus in cash rather than actively managing it toward higher returns.

Tax Advantages of the Reinsurance Structure

Premiums collected into the reinsurance entity are generally treated as deferred within the structure until claims are paid or profits are distributed. That means reserves compound on a pre-tax basis — money that would have gone to the IRS stays inside the structure building value for the business instead.

For smaller programs, the 831(b) election allows property and casualty insurance companies under the $2.9 million annual premium threshold to be taxed only on investment income, not underwriting income. This can reduce the annual tax burden substantially during the reserve-building phase.

Important: Tax treatment should be reviewed with a CPA experienced in captive insurance structures. IRS Notice 2016-66 identifies certain micro-captive arrangements as transactions of interest — compliance and proper structure matter.

Long-Term Wealth Building Through Compounding

These tax advantages accelerate what makes reinsurance structures genuinely valuable over time: the accumulation of a capital pool entirely separate from the operating business. Reserve assets keep earning through slow seasons, economic cycles, and competitive pressure — independent of what's happening in the field.

Common uses for accumulated surplus:

- Retirement income diversification

- Funding business expansion or equipment investment

- Succession planning capital

- Key employee retention programs

How to Transition to a Contractor-Owned Reinsurance Program

Step 1: Audit Your Current Program and Quantify the Profit Leak

Before making any structural change, calculate what's actually leaving your business:

- What total premiums are collected annually across warranty products?

- What's paid out in claims?

- What does the third-party administrator retain?

The gap between claims paid and premiums collected — minus expenses — is the underwriting profit currently funding someone else's business. WarrantyRE offers a no-cost business analysis as the starting point for contractors and dealers evaluating this transition.

Step 2: Select the Right Structure and Administrator

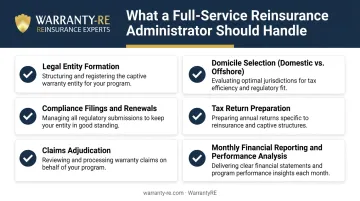

The administrator you choose matters as much as the structure itself. Look for a partner who handles:

- Legal entity formation

- Domicile selection (domestic vs. offshore)

- Compliance filings and renewals

- Tax return preparation

- Claims adjudication

- Monthly financial reporting and performance analysis

WarrantyRE's full-service model covers every item on that list — no hidden fees. With 30+ years of experience and 400+ clients served across HVAC, roofing, plumbing, electrical, and automotive, we've built this process to be straightforward for contractors.

Step 3: Form the Entity and Set Up the Trust Structure

Key formation decisions include:

- Domicile selection: domestic and offshore options carry different regulatory, capital, and reporting requirements — choosing correctly matters for long-term compliance

- Trust account establishment: funds are held with a qualified U.S. financial institution as trustee, regardless of domicile

- Fronting carrier relationship: an A-rated insurer provides the CLIP or backing policy, giving the program legal standing

- Compliance readiness: IRS 831(b) election if applicable, plus state service contract licensing

WarrantyRE manages this entire process on your behalf. All funds remain in the United States regardless of domicile selection.

Step 4: Train Your Team and Begin Enrolling Contracts

Entity formation is just the starting point — your team needs to be ready to sell and service the program from day one:

- Service advisors, installation crews, and F&I staff need to understand how to present and enroll customers

- Pricing needs to reflect warranty fees built into proposals or F&I menus

- Staff need to know how claims are handled and what customers can expect

WarrantyRE provides online and in-person training as part of onboarding, covering program development, customer-facing presentation, and claims workflow — so your team launches confident, not guessing.

Frequently Asked Questions

What is the difference between a retro program and a reinsurance captive?

A retro program pays a profit-share back from the third-party insurer after claims run out — you're still participating in someone else's structure. A reinsurance captive is an entity you own that actually accepts ceded risk, holds reserves, and retains full underwriting profit and investment income directly.

How much premium volume does a contractor or dealer need to start a reinsurance program?

Volume thresholds vary by structure. Retro programs have a lower bar, while administrator obligor models benefit from consistent annual premium flow. WarrantyRE works with contractors and dealers at various growth stages — a business analysis is the best way to evaluate your specific situation.

What is an administrator obligor reinsurance company?

It's a structure where your own entity is the obligor — the party contractually responsible for honoring the warranty. A CLIP from an A-rated carrier provides the financial backstop, giving you full control over pricing, claims handling, and profit retention.

What happens to reserve funds that are never used to pay claims?

Once the risk period for a contract expires and claims are no longer expected, unearned premium reserves convert to earned surplus. Those funds can be moved to a less-restricted account, invested for higher returns, or distributed to the business owner.

How are reinsurance program reserves typically invested?

UPR (A account) funds are invested conservatively per insurer and regulatory guidelines — typically government bonds. Surplus (B account) funds have greater flexibility and, once reserves exceed 125% of unearned premiums, can be invested in equities or other higher-yield vehicles at the direction of company ownership.

How long does it take to set up a contractor-owned reinsurance company?

Timelines vary based on structure complexity and domicile selection. Working with a full-service administrator like WarrantyRE, who manages entity formation, legal filings, trust setup, and compliance, reduces the setup burden on the contractor or dealer and accelerates the path to first contract enrollment.