Introduction

Oklahoma sits in one of the most storm-battered regions in the country. The state ranked #3 for major hail events in 2025 with 369 documented events, according to the Insurance Information Institute's hail data — and that's on top of tornado seasons, high-wind events, and ice storms that roll through year after year.

When storm damage hits a roof, a homeowners insurance claim is often the only realistic alternative to paying tens of thousands of dollars out of pocket. Most Oklahoma homeowners don't understand how the claims process works until they're already in the middle of one — and early mistakes can result in a reduced payout or an outright denial.

This guide walks through exactly what your policy covers, how to file correctly, and what to avoid.

TL;DR

- Oklahoma homeowners insurance covers sudden storm damage — hail, wind, tornadoes — but not gradual wear, aging, or neglect

- Most policies give you up to 12 months to file, but your specific policy controls — check it before assuming

- RCV (Replacement Cost Value) pays today's replacement price; ACV (Actual Cash Value) deducts depreciation, leaving a larger out-of-pocket gap

- Never let an adjuster inspect your roof without your roofing contractor present; subtle damage gets missed regularly

- The first payout offer is rarely final — request supplements, challenge low estimates, or escalate to the Oklahoma Insurance Department

Why Roof Insurance Claims Are a Reality for Oklahoma Homeowners

Oklahoma's severe weather risk is consistent and predictable. The state sits squarely in the central Plains severe-weather corridor, where warm Gulf air collides with cold fronts, producing hailstorms, tornadoes, and damaging wind events with consistent frequency.

According to the Oklahoma Insurance Department, hail can cause substantial damage to roofs and most standard homeowners insurance policies cover it. The three most common storm types that trigger roof claims in Oklahoma are:

- Hailstorms — Hail bruises asphalt shingles invisibly from the ground, accelerating granule loss and weakening the mat until leaks eventually appear

- High winds and tornadoes — Sub-tornado wind events can still lift shingles, break seals, and drive water beneath roofing layers

- Ice storms — Ice accumulation and freeze-thaw cycles damage flashing, crack sealant, and can force water under shingles at vulnerable transition points

The financial stakes are real. Roof replacement costs are driven by material type, labor, local code requirements, and the size of the structure — and in Oklahoma's current construction environment, total project costs can reach $10,000–$20,000 or more for an average home. Knowing how to navigate the claims process from the start directly affects how much of that cost your insurer covers.

What Oklahoma Homeowners Insurance Actually Covers for Your Roof

Covered Perils and Policy Types

Standard HO-3 and HO-5 homeowners policies cover roof damage caused by sudden, accidental events. In Oklahoma, the covered perils most relevant to roofing are: hail, wind, tornadoes, fallen trees, and fire.

Damage must affect the roof's structural function, not just its appearance. Many Oklahoma policies now include cosmetic damage exclusions — meaning dents, dings, or surface scuffs that don't impair the roof's ability to keep water out may not be covered. Check your declarations page and any roof-surfacing endorsements carefully.

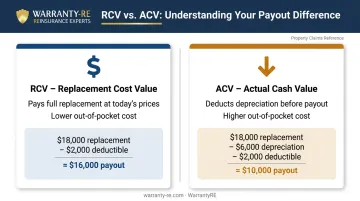

RCV vs. ACV: The Payout Difference

Your policy type determines how much money you actually receive:

| RCV (Replacement Cost Value) | ACV (Actual Cash Value) | |

|---|---|---|

| What it pays | Full replacement cost at today's prices, minus deductible | Replacement cost minus depreciation, minus deductible |

| Example (hypothetical) | $18,000 replacement → you pay $2,000 deductible → insurer pays $16,000 | $18,000 replacement → $6,000 depreciation − $2,000 deductible → insurer pays $10,000 |

| Out-of-pocket impact | Lower | Significantly higher |

ACV policies leave homeowners responsible for a much larger gap. If you're unsure which type you have, check the declarations page or call your agent before a storm hits.

Wind and Hail Deductibles

Many Oklahoma policies carry a separate wind and hail deductible calculated as a percentage of your home's insured value — not a flat dollar amount. According to the Oklahoma Insurance Department's homeowners checklist, this deductible is typically 1% of the dwelling amount but can range from 2% to 5%.

On a home insured for $300,000, that means your out-of-pocket deductible could run from $3,000 to $15,000 — well above what most homeowners expect from a standard flat deductible. Confirm your deductible type and amount before filing.

What's Not Covered

Knowing your deductible is only half the picture. Insurers also scrutinize claims for signs of neglect, and several common scenarios fall outside standard coverage:

- Normal wear and aging shingles

- Manufacturer defects

- Damage from lack of maintenance

- Pre-existing conditions that existed before the storm

- Cosmetic-only damage under policies with surfacing exclusions

Recoverable Depreciation Under RCV Policies

If you have RCV coverage, your insurer typically pays in two stages. The first check covers the ACV amount — the depreciated value. The withheld portion is released only after you complete repairs and submit documentation proving the work is done. Don't skip this step; that second payment won't come automatically.

How to File a Roof Insurance Claim in Oklahoma: Step by Step

The process spans several weeks, and each step affects both approval odds and payout amount. Your policy controls the exact notice and filing deadlines — some require initial notification within 30–60 days, even if the full filing window extends to 12 months. Act promptly.

Step 1: Document Everything Before Touching Anything

Before any cleanup or repairs, capture thorough photo and video evidence. The Oklahoma Insurance Department advises that immediate documentation is the most critical first step after storm damage.

What to photograph:

- Wide shots of the full property and roofline

- Close-ups of damaged, displaced, or missing shingles

- Dented vents, gutters, and flashing

- Granule accumulation in gutters (a key hail damage indicator)

- Any interior water staining or ceiling damage

Temporary repairs — tarps, plywood — are often reimbursable if you keep receipts. Permanent repairs should wait until after the adjuster's inspection.

Step 2: Get a Professional Roof Inspection First

Before calling your insurer, get a roofing contractor on the roof. This establishes a documented baseline of all damage — including hail bruising, lifted nails, and underlayment issues that aren't visible from the ground. That documentation gives you a strong starting point going into the claim and reduces the risk of the adjuster missing damage that affects your payout.

Step 3: Review Your Policy and File the Claim

Before filing, confirm:

- RCV or ACV coverage

- Deductible type and amount (flat vs. percentage-based)

- Any cosmetic damage exclusions

- Filing and notice deadlines

Most insurers accept claims by phone, online portal, or mobile app. Provide the exact storm date, a description of the damage, your policy number, and contact information.

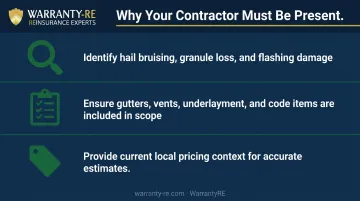

Step 4: Be Present During the Adjuster Inspection

The adjuster assesses damage and determines the insurer's payout — they work for the insurance company, not you. Having your roofing contractor present during this inspection is one of the most effective steps you can take.

A contractor can:

- Point out hail bruising, granule loss, and flashing damage the adjuster may overlook

- Ensure gutters, vents, underlayment, and code-required components are included in the scope

- Provide current local pricing context if the adjuster's estimate uses outdated figures

Step 5: Review the Estimate and Request Supplements If Needed

After the inspection, you'll receive a Statement of Loss listing repair line items, depreciation, and the initial payment amount. Compare it line by line against your contractor's assessment.

Common discrepancies include:

- Outdated material pricing

- Missing code-upgrade items (drip edge, ice and water barrier where required by Oklahoma building code)

- Unlisted components like flashing, vents, or underlayment

Your contractor can submit a supplement to the insurer requesting additional funds for overlooked or undervalued items. Supplementing is a routine part of the claims process, not an adversarial move.

Step 6: Choose Your Contractor and Complete the Work

You have the legal right to choose your own roofing contractor. The insurer cannot require you to use a specific company or their preferred vendor list.

Warranty coverage is worth evaluating before you sign. Manufacturer material warranties from GAF, Owens Corning, and similar brands cover shingles, but they don't cover labor or installation workmanship. That gap falls entirely on the contractor. Ask any contractor you're considering what their workmanship warranty covers, how long it lasts, and what backs it financially — a written, structured warranty offers more protection than an informal verbal commitment.

Once work is complete, submit proof of completion to your insurer to trigger the release of any withheld depreciation under an RCV policy.

Key Factors That Affect Your Roof Claim Outcome

Roof Age and Condition

Older roofs depreciate faster under actual cash value (ACV) calculations. A 15-year-old roof will receive significantly less than a 5-year-old roof with identical storm damage. Condition at the time of loss — including evidence of prior maintenance or neglect — shapes the adjuster's final valuation.

Documentation Quality

The completeness of your documentation — contractor inspection report, photographs, damage itemization — is one of the few things you fully control. Weak documentation makes it easier for an adjuster to minimize or miss damage.

Filing Timing

Filing promptly after a storm keeps the link between your damage and a specific storm clear. Delayed claims give insurers grounds to question causation, and visible unaddressed damage can create problems under policy maintenance obligations.

Beyond the claim basics, two Oklahoma-specific factors can significantly affect your final settlement amount.

Oklahoma Building Code Upgrades

If a roof replacement triggers a code-required upgrade — such as drip edge installation or updated ventilation requirements — those additions may only be covered if your policy includes ordinance or law coverage. Ask your insurer directly whether this applies to your policy before the replacement begins.

Oklahoma Insurance Department Resources

The OID regulates insurer conduct and requires prompt claim acknowledgment. Under Oklahoma administrative rules, insurers must acknowledge a claim within 30 business days after receiving notice.

If your claim is disputed or underpaid:

- File a complaint with OID Consumer Assistance at oid.ok.gov

- Call the OID consumer hotline: 1-800-522-0071

- Request the EAGLE Mediation Program as an alternative to litigation

Common Mistakes Oklahoma Homeowners Make That Hurt Their Claims

Don't delay filing or documentation. Delayed filing weakens the connection between damage and a specific storm, and many policies require notice within 30–60 days. Visible unrepaired damage can also raise questions about whether you took reasonable steps to prevent further deterioration — which complicates your claim.

Always have your contractor present during the adjuster's inspection. Adjusters covering many claims may miss subtle hail bruising, underlayment damage, or code-required components — simply because they lack the roofing-specific expertise your contractor brings. The result is an underfunded estimate you're left to cover out of pocket.

Watch what you say to the adjuster. Stick to factual, event-specific descriptions. Avoid speculating about damage causes, volunteering information about delayed maintenance, or downplaying what you observed. Your documentation and contractor's report should carry the detailed argument.

Don't treat the first estimate as final. The initial payout offer is a starting point. You can request supplements, submit a contractor's counter-assessment, or formally appeal a denial. Review any denial letter carefully, gather additional evidence, and submit a written response. If that fails, escalate to the Oklahoma Insurance Department or consult an attorney.

Frequently Asked Questions

What should I not say to an insurance adjuster about my roof?

Avoid speculating about damage causes, mentioning delayed maintenance, or downplaying what you observed. Stick to factual descriptions of what happened during the storm and let your contractor's inspection report and photos carry the detailed evidence.

How can I get my roof replaced through insurance?

A full replacement is covered when storm damage from a qualifying event — hail, wind, tornado — is extensive enough that repair isn't sufficient. A professional inspection establishes that scope, which the adjuster then confirms.

Will homeowners insurance pay for roof repair?

Yes, storm-related repairs are covered subject to your deductible and policy terms. However, cosmetic-only damage may be excluded under some Oklahoma policies. Whether the payout covers repair or full replacement depends on the extent of damage documented.

How long do I have to file a roof insurance claim in Oklahoma?

Most Oklahoma policies allow up to 12 months from the storm date, but many require initial notice within 30–60 days. Your specific policy controls these deadlines — check it and notify your insurer promptly to protect your rights.

What is the difference between RCV and ACV roof coverage?

RCV pays to replace your roof at today's prices minus your deductible. ACV deducts depreciation based on the roof's age and condition before calculating the payout. ACV policies result in a significantly lower initial payment and higher out-of-pocket costs.

Will filing a roof insurance claim raise my rates in Oklahoma?

Wind and hail claims are treated as weather-related events, not policyholder-fault claims. Most insurers do not surcharge for them individually, but this varies — confirm with your agent before filing if rate impact is a concern.