Introduction

Most HVAC contractors exploring reinsurance programs aren't asking what a warranty costs their customers—they're asking what it costs to stop paying a third-party warranty company and start keeping that profit themselves. The HVAC warranty market represents significant recurring revenue, with home warranty and service contract providers retaining gross profit margins exceeding 55%, according to Frontdoor's 2025 financial disclosures. Most contractors hand this profit to third parties without realizing they could capture it inside their own tax-advantaged reinsurance structure.

What follows is a direct breakdown of HVAC warranty reinsurance costs—formation, administration, and ongoing fees—so contractors can evaluate whether redirecting existing warranty premiums into their own reinsurance entity is worth it.

TL;DR

- Setup investment: Program formation carries one-time costs that vary by structure — speak with a reinsurance administrator to get numbers specific to your situation

- Volume drives efficiency: Contractors with higher installation volume spread fixed costs across more warranties and reach profitability faster

- Premiums fund the program: Reinsurance is funded by premiums already collected from customers; the real question is whether that underwriting profit stays with you or a third party

- Full-service administration: A full-service partner covering legal, compliance, claims, and bookkeeping costs more upfront but protects against costly failures down the line

How Much Does an HVAC Warranty Reinsurance Program Cost?

There's no single published price for an HVAC warranty reinsurance program. Costs vary widely based on program structure, installation volume, geographic scope, and the level of administrative support chosen. Unlike buying a product off the shelf, the cost model here involves redirecting warranty premiums that already exist in your business—premiums currently paid to third-party warranty companies.

When contractors misunderstand this cost structure, two problems emerge: they either overestimate the out-of-pocket investment and avoid a profitable program, or they underbudget for compliance and administration, exposing themselves to regulatory risk and claim disputes that cost far more than proper setup.

Typical Cost Tiers

Entry-Level / Lower-Volume Programs

Contractors with smaller installation volumes can establish basic reinsurance structures that include entity formation and minimal administrative support. At this tier, the contractor typically handles more operational responsibilities internally while the administrator manages essential compliance and regulatory filings.

What's typically excluded at this level:

- Dedicated claims adjudication staff

- Comprehensive financial reporting

- Ongoing tax compliance coordination

- Proactive program optimization

Contractors at this level may need to hire separate professionals for tax preparation and detailed financial analysis. This structure works best for contractors testing reinsurance viability before making a full administrative commitment.

Mid-Range / Standard Programs

The most common entry point for HVAC contractors doing moderate installation volume annually. General captive insurance benchmarks suggest viability begins around $1 million in annual premiums, though warranty-specific reinsurance programs may have lower thresholds. Full-service administration at this tier typically covers:

- Complete company formation and legal setup

- All state filings and licensing coordination

- Monthly claims administration and adjudication

- Compliance monitoring and regulatory management

- Monthly financial statements and performance reports

- Coordination of annual tax return preparation

- Staff training and ongoing support

Established contractors ready to stop paying third-party warranty providers and capture 100% of underwriting profits will find the mid-range tier the natural fit.

High-Volume / Full-Profit-Capture Programs

Higher-volume contractors maximizing underwriting profit returns typically invest in enhanced reserve structures and comprehensive administration. As volume increases, the percentage of premiums allocated to administration often decreases—meaning more of every premium dollar flows back as profit.

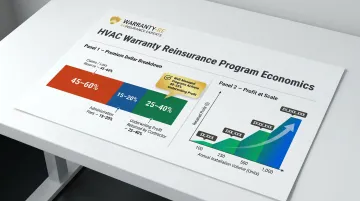

According to industry analysis of extended warranty economics, well-managed programs achieve loss ratios in the 45–60% range. That means 40–55% of collected premiums become underwriting profit when claims are managed effectively. At scale, that margin compounds into significant retained earnings—while still meeting all state regulatory requirements.

Contractors with established warranty programs and high installation volumes get the most from this tier, both in annual profit capture and long-term reserve growth.

Critical Clarification: Across all tiers, the reserve capital funding the program comes from warranty premiums collected from customers—not purely from the contractor's operating capital. The contractor's primary investment covers setup, administration, and maintaining proper financial reserves as required by state regulations.

Key Factors That Affect the Cost of an HVAC Warranty Reinsurance Program

Business-specific factors and structural choices both shape your program's pricing. Knowing which variables you control—and which are fixed by regulation or market conditions—is the starting point for budgeting accurately.

Volume of Annual HVAC Installations

The number of systems installed per year is the single biggest driver of cost efficiency. Higher volume spreads formation and administration fees across more warranty contracts, significantly reducing the per-unit cost.

For example, if program administration costs $40,000 annually and a contractor installs 200 systems with warranties, the cost per warranty is $200. At 400 installations, that drops to $100 per warranty—a 50% reduction in unit cost with the same administrative investment.

AHRI data shows approximately 3 million heating and cooling systems are replaced annually across the U.S., with contractors ranging from small owner-operators handling fewer than 50 installations per year to large operations exceeding 500 annually. Your position on that spectrum determines whether program economics work in your favor from year one or require a ramp-up period.

Program Structure and Reinsurance Model

The administrator-obligor reinsurance structure—where the contractor's company serves as the obligor, backed by an A-rated insurer—affects both cost and the contractor's ability to fully capture underwriting profits.

In this model, the contractor owns 100% of the reinsurance entity and retains all underwriting profits. The A-rated insurance carrier provides ultimate financial backing if claims exceed reserves, protecting against catastrophic loss while allowing full profit retention.

This structure requires proper legal formation, trust account management, and regulatory compliance—costs that simpler self-funded models might avoid, but at the expense of adequate risk protection.

Alternative structures, such as profit-sharing arrangements with third-party warranty companies, typically return only a percentage of underwriting profits (often 30-50%) while the provider retains the rest. The administrator-obligor model costs more to establish but returns 100% of profits to the contractor.

Coverage Terms and Warranty Scope

Warranty length and scope directly affect reserve requirements and program costs. A 1-year labor-only warranty requires significantly lower reserves than a 5-year parts-and-labor warranty or a 10-year full-system replacement guarantee.

According to Trinity Warranty's pricing data, consumer-facing HVAC extended warranties range from $115-$220 for a 2-year air conditioner labor warranty to $850-$1,600 for a 10-year complete system labor warranty. The premium collected determines reserve funding, which in turn sets the financial structure and reserve requirements for your reinsurance entity.

Broader scope and longer terms mean higher exposure—which translates directly into higher reserve requirements and more complex claims management overhead.

State Regulatory Requirements and Geographic Scope

Warranty programs operating across multiple states face different regulatory and licensing requirements, which can add to formation and compliance costs. Single-state programs are typically simpler and less costly to establish.

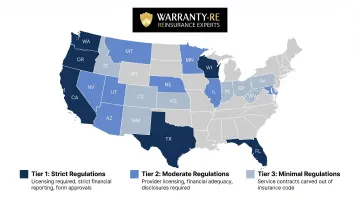

NCOIL research categorizes state regulation into three tiers:

- Significant regulation (CA, WA, OR, TX, FL, WI): Requires licensing for administrators, sellers, and obligors; strict financial reporting; prior approval of contract forms

- Moderate regulation (NV, UT, AZ, MT, NE, MN, IL): Requires licensing for service contract providers; financial adequacy demonstration; specific disclosures

- Minimal regulation (ID, WY, CO, NM, KS, IN, OH, WV, PA, MD): Service contracts carved out of insurance code with no additional regulatory requirements

Operating in California, Florida, and Texas simultaneously means navigating three distinct "significant regulation" jurisdictions—each with separate licensing, form approvals, and financial reporting requirements. That's substantially more complex and costly than running a program in a single "minimal regulation" state.

Full Cost Breakdown: One-Time Setup vs. Ongoing Expenses

The total cost of ownership for a reinsurance program extends beyond setup. Contractors should evaluate both the initial investment and the annual operating cost structure before comparing it to what they currently pay third-party warranty providers.

Program Formation and Entity Setup (One-Time)

One-time costs of establishing the reinsurance entity include legal entity formation, state filings, licensing, initial compliance documentation, and program design. General captive insurance formation costs typically range from $50,000 to over $100,000, though warranty-specific programs administered through specialized firms may differ.

Formation costs typically include:

- Legal entity formation and corporate structure ($10,000+)

- Feasibility study and program design ($15,000-$25,000 for complex programs)

- Application and licensing fees ($5,000-$15,000 depending on jurisdiction)

- Initial compliance documentation and regulatory filings

A full-service partner like WarrantyRE manages all legal forms, filings, and company setup on the contractor's behalf, reducing internal time investment and minimizing error risk that could lead to costly regulatory issues.

Ongoing Administration Fees (Recurring)

Ongoing costs cover claims adjudication, compliance monitoring, financial reporting, tax preparation, and staff training. Fees are structured as per-warranty charges, flat monthly or annual fees, or a percentage of premiums collected — models vary by administrator.

General captive management fees range from 15-35% of annual written premiums or flat annual fees of $36,000-$100,000+. Additional line items typically include:

- Actuarial opinions: $5,000-$15,000 annually

- Audit and tax preparation: $10,000-$20,000 annually

WarrantyRE bundles these services with transparent pricing and no hidden add-on fees, so contractors know their total program cost before signing.

Reserve Funding (Recurring—Self-Sustaining)

Reserve accounts hold the portion of each warranty premium set aside to pay future claims. This isn't an expense in the traditional sense — it's the contractor's own money, held in their reinsurance company and available for claims or investment returns.

According to service contract industry analysis, the typical cost structure allocates roughly 80% to premium reserves with 20% covering administration fees. On an $800 warranty, that's $640 to reserves and $160 to administration.

California regulations generally require financial security of approximately 40% of gross contractual consideration as a reserve for obligations not backed by admitted insurance. Proper A-rated insurer backing through a contractual liability insurance policy (CLIP) can reduce or eliminate statutory reserve requirements, improving cash flow.

The key differentiator: any portion of the premium reserve not used to pay claims becomes underwriting profit retained by the contractor's reinsurance company. With third-party providers, that profit disappears entirely.

Renewal, Reporting, and Tax Compliance (Periodic)

Annual renewal costs, required regulatory filings, and tax return preparation for the reinsurance entity are recurring expenses. These typically include:

- Annual regulatory filings and license renewals

- Financial statement audits

- Tax return preparation (Form 1120-PC for insurance companies)

- Compliance monitoring and updates

In a managed program, these costs are bundled rather than billed separately. WarrantyRE handles all filings, tax returns, and renewals directly — no surprise invoices, no compliance gaps to manage internally.

Reinsurance Program vs. Third-Party Warranty Provider: What Each Actually Costs

Most HVAC contractors currently pay a third-party warranty provider and never see those dollars again. Reinsurance changes that equation fundamentally.

Cost Comparison Framework

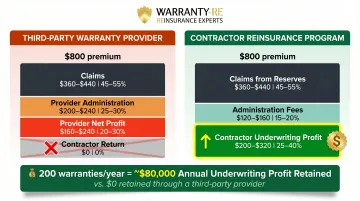

Third-Party Warranty Provider:

- Premium paid out: 100% ($800 per warranty example)

- Claims paid by provider: ~45-55% (industry average)

- Gross profit retained by provider: 45-55%

- Net profit to provider after administration: 20-30%

- Return to contractor: $0

Reinsurance Program:

- Premium collected: 100% ($800 per warranty example)

- Administration fees paid: ~15-20% ($120-$160)

- Claims paid from reserves: ~45-55% ($360-$440)

- Underwriting profit captured by contractor: 25-40% ($200-$320)

- Reserve investment income: Additional returns

Frontdoor's 2025 financial data reveals the economics of the largest home warranty provider: claims cost ratio of 44.7%, gross profit margin of 55.3%, and net income margin of 12.2%. These profit margins represent money that contractors using third-party providers pay away permanently.

In a reinsurance structure, the contractor retains 100% of underwriting profit rather than ceding it to a third party. On 200 warranties annually at $800 each with a 50% loss ratio, underwriting profit approaches $80,000 annually—profit that builds in the contractor's own tax-advantaged entity.

Long-Term Value Shift

While a reinsurance program has setup costs that a third-party arrangement does not, the ongoing cost per warranty sold is substantially lower when underwriting profit is factored in. The contractor's reserve account also compounds over time — profitable years don't just return a margin, they build a balance sheet asset.

The tax structure accelerates this advantage. Under IRC Section 831(b), small property and casualty insurance companies with less than $2.9 million in annual net premiums may elect to be taxed only on investment income, creating a benefit that third-party warranty arrangements never offer.

Expected savings from properly structured programs often reach 20-30% over three years, with ROI typically becoming clear within 3 to 5 years.

When Third-Party Arrangements May Still Make Sense

Very low-volume contractors or those just starting warranty programs may not yet have the volume to justify full reinsurance program costs. Contractors installing fewer than 50 systems annually with warranties should carefully evaluate whether current volume supports the administrative infrastructure required for compliance.

However, many contractors underestimate their volume or fail to recognize that offering better warranties could increase sales and customer satisfaction—and higher close rates, recurring revenue, and tax savings can make reinsurance viable well before a contractor expects it to be.

How to Plan Your HVAC Warranty Reinsurance Program Budget

The right budget is not the cheapest setup—it's the one that matches your installation volume, growth trajectory, and internal administrative capacity.

Factors to Assess Before Committing

Evaluate these variables carefully before establishing your program:

- Annual installation volume: Count every system you install annually — new units and replacements both qualify for warranty coverage.

- Warranty premium per install: What customers currently pay for extended labor coverage, based on system cost and coverage duration.

- Third-party warranty spend: Total your annual payments to outside warranty companies. That's money leaving your business that a reinsurance program would redirect back to you.

- Internal staff capacity: Contractors without dedicated admin staff benefit most from full-service claims management; those with admin support may handle more themselves.

- States of operation: Single-state programs face simpler compliance requirements; multi-state operations require more complex regulatory coordination.

Common Budgeting Mistakes to Avoid

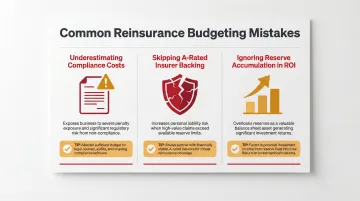

- Underestimating compliance costs: Self-administered programs require ongoing regulatory monitoring, annual filings, and tax return preparation. Underbudgeting for professional administration often leads to penalties or regulatory exposure.

- Skipping A-rated insurer backing: Programs without a contractual liability insurance policy (CLIP) from an A-rated carrier leave contractors personally liable if claims exceed reserves. Low-cost setup fees don't offset that risk.

- Ignoring reserve accumulation in ROI modeling: Reserves build inside your own company, earn investment returns, and become accessible once they exceed required levels. Factoring this in makes the ROI picture look very different from a simple cost comparison.

How to Get an Accurate Program Cost Estimate

These mistakes share a common thread: they stem from working off generic estimates rather than contractor-specific modeling. A business analysis from a reinsurance program specialist gives you actual cost projections based on your volume, warranty pricing, and operational structure.

WarrantyRE has helped over 400 businesses establish reinsurance programs since 1994. A consultation delivers contractor-specific cost modeling and ROI projections — not industry averages.

Contact WarrantyRE at (804) 824-9533 or request a free analysis at their website to get customized projections for your HVAC contracting business.

Frequently Asked Questions

What is an HVAC warranty reinsurance program?

An HVAC warranty reinsurance program is a structure in which an HVAC contractor establishes their own warranty company, backed by an A-rated insurer, to collect warranty premiums, pay claims, and keep the underwriting profit—instead of paying those premiums to a third-party warranty provider.

How much does an HVAC warranty cost?

Consumer-facing HVAC warranty pricing typically ranges from $115–$220 for 2-year labor coverage to $500–$1,600 for 10-year complete system coverage, depending on equipment type and local labor rates. These are the fees contractors collect from customers—not the business-side cost of setting up the reinsurance structure that captures those premiums.

How is a reinsurance program different from self-insuring warranty claims?

A proper reinsurance program is backed by an A-rated insurance carrier, protecting the contractor if claims exceed reserves. Self-insuring means the contractor absorbs all risk with no external backing—creating real financial and compliance risk that could threaten the business if claims spike unexpectedly.

How much is HVAC liability insurance?

HVAC liability insurance (general liability/errors and omissions) is a separate product from warranty reinsurance. General liability insurance for HVAC contractors averages $78 per month or $941 annually. Reinsurance covers warranty claim risk; liability insurance covers third-party injury or property damage.

How long does it take to set up an HVAC warranty reinsurance program?

Timeline varies by state and program complexity. With a full-service partner managing entity formation, filings, and onboarding, most programs are operational within 30–90 days. Contact WarrantyRE at (804) 824-9533 for a timeline estimate based on your state and business structure.