Warranty reinsurance offers a different path. Instead of reselling a third party's warranty product, contractors can either back their own warranty programs or partner with specialized reinsurance providers — and choosing the right partner directly impacts profitability, customer retention, and claims outcomes. The choice matters: it's the difference between earning a sales margin and capturing the entire underwriting profit.

TL;DR

- HVAC warranty reinsurance provides insurance-grade risk protection while the contractor retains premium revenue and control

- Contractors who own their warranty company through an admin obligor model capture underwriting profits — third-party resellers keep those profits instead

- Strong providers bring A-rated reinsurance backing, full administration support, compliance management, and clear financial reporting

- Evaluate providers on program structure, financial stability, and hands-on HVAC contractor experience

- WarrantyRE offers contractors a complete admin obligor setup — including claims administration, compliance, and full profit capture — built on 30+ years of reinsurance experience

What Is HVAC Warranty Reinsurance?

HVAC warranty reinsurance is the mechanism by which a contractor's warranty or service agreement obligations are financially backed by an insurer or reinsurer, transferring or sharing the risk of warranty claims. Instead of the contractor bearing 100% of the liability when a furnace fails or an AC unit malfunctions during the warranty period, a reinsurance structure provides financial protection backed by an insurance company.

Two Primary Models:

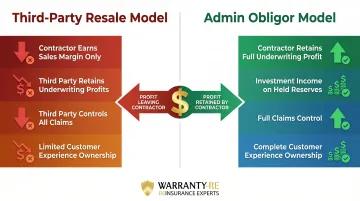

Third-Party Warranty Programs — The contractor resells plans from a provider like JB Warranties. The third party acts as the obligor, retains underwriting profits, and controls claims. The contractor earns a margin on each resale.

Admin Obligor Reinsurance — The contractor owns the warranty company, collects premiums, and controls claims. An A-rated reinsurer provides financial backing if the contractor's company can't cover obligations — and the contractor keeps the underwriting profit.

Why More Contractors Are Moving to Admin Obligor:

The ACCA/FCG study shows warranty margins of 24-30% even in the third-party resale model — warranty programs generate real margin, even before owning the underwriting layer. Contractors who move to admin obligor retain:

- The full underwriting profit (premiums minus claims)

- Investment income earned on held reserves

- Control over claims adjudication and customer experience

Market Context:

The North America extended warranty market is projected to reach $85.6 billion by 2030, growing at a 9.5% CAGR, according to Grand View Research.

HVAC-specific figures aren't publicly isolated, but the ACCA study confirms that 10-year agreements account for 48% of contractor warranty sales and 5-year agreements for 20%. Contractors who own the underwriting layer — rather than reselling third-party plans — capture that profit directly.

Best HVAC Warranty Reinsurance Providers

These providers were selected based on program structure, financial backing, administrative support, compliance capabilities, and relevance to HVAC and home service contractors. Providers vary significantly in model type — from contractor-owned reinsurance structures to third-party ESA programs — so the right fit depends on how much ownership and profit participation you want from your warranty program.

WarrantyRE

Founded in 1994 in Southeast Virginia by Tim Byrd, WarrantyRE has spent over 30 years helping home service contractors — including HVAC companies — establish and manage their own administrator obligor reinsurance companies. The company has served 400+ clients across the United States, helping them replace third-party warranty providers and capture underwriting profits that would otherwise flow to external companies.

With the admin obligor model, the HVAC contractor's own reinsurance company is backed by A-rated insurers, giving the contractor full ownership of premiums, claims control, and underwriting profits. Warranty fees built into every furnace, AC, heat pump, or mini split installation become a profit center — not a third-party expense.

WarrantyRE provides full-service administration including:

- Claims adjudication — WarrantyRE services every claim from first call to final resolution, eliminating the need for contractors to manage adjusters or claims paperwork

- Compliance management — Coordinates licensing, IRS Code 831(b) compliance, and regulatory filings

- Financial bookkeeping — Prepares monthly financial statements and annual reports for tax preparers

- Staff training — Onboarding and ongoing education for contractor teams

- Tax planning — Significant tax deductions on reinsurance contributions

No hidden fees, a guaranteed setup process, and a shared-success partnership model round out the offer.

| Program Model | Admin Obligor Reinsurance (contractor owns their warranty company) |

|---|---|

| Key Services | Claims adjudication, compliance, bookkeeping, staff training, tax returns and renewals |

| Best For | HVAC contractors wanting to capture 100% of warranty profits and build recurring revenue |

Trinity Warranty

Founded in 1991 and now a subsidiary of Kingsway Financial (acquired 2012), Trinity Warranty provides Extended Service Agreements (ESAs) for HVAC/R and plumbing contractors. The company operates as a service contract administrator backed by four different A-rated insurance underwriters, offering fully insured warranty programs that extend manufacturer warranties on HVAC/R/plumbing equipment.

Trinity Warranty specializes in customizable ESA programs covering parts only, labor only, or parts and labor. Contractors pick coverage levels and labor reimbursement rates tailored to their market. The company handles large commercial equipment (over 25 tons and boilers over 2M BTUs) and offers $0 deductibles for equipment owners.

Key features include:

- Multi-carrier backing — Programs backed by four A-rated carriers provide financial stability

- National accounts support — Service dispatch and facility management for contractors serving commercial clients

- Broad eligibility — New residential equipment eligible up to 2 years after installation; commercial equipment up to 1 year

- Indoor air quality solutions — Extends coverage beyond core HVAC systems

| Program Model | ESA Administrator with Multi-Carrier Backing |

|---|---|

| Key Services | Extended service agreements, preventive maintenance programs, online administration platform, national dispatch |

| Best For | HVAC contractors serving residential and commercial markets needing broad equipment coverage |

Fortegra Financial

Fortegra Financial, part of Tiptree Inc. (NASDAQ: TIPT), operates as a specialty insurer with 45+ years in the warranty business and holds an A- (Excellent) rating from AM Best (under review with positive implications as of April 2026).

Fortegra operates primarily as the underwriting carrier behind service contract programs rather than a direct contractor-facing administrator. Their structure includes:

- White-labeled warranty programs — Profit-sharing arrangements for program partners

- In-house capabilities — Underwriting, compliance, and claims management fully integrated

- HVAC-specific coverage — Home protection plans specifically include HVAC, plumbing, and electrical systems

- Customizable plans — Tailored to meet partner pricing and margin goals

HVAC contractors typically access Fortegra-backed programs through a program administrator rather than contracting directly with the carrier. The company's financial strength and regulatory standing make it a reliable backing insurer for warranty programs.

| Program Model | Insurance Carrier / CLIP Provider (accessed through program administrators) |

|---|---|

| Key Services | Underwriting, compliance management, claims processing, profit-sharing structures |

| Best For | Program administrators or larger contractors needing carrier-level financial backing |

AmTrust Financial / Warrantech

AmTrust Financial is one of the world's largest underwriters of warranty insurance, with $8.8B in gross written premium, $27.1B in total assets, and 55 million active contracts across 55 countries.

The company holds an A- (Excellent) rating from AM Best with a stable outlook and financial size category XV ($2B+ capital/surplus). Warrantech operates as AmTrust's warranty administration subsidiary.

AmTrust offers multiple program structures including:

- First Dollar (full risk transfer)

- Excess of Loss (coverage above a retention threshold)

- Failure-to-Perform (CLIP) (steps in if obligor defaults)

- Participation Programs including reinsurance, captive insurance, Dealer Owned Warranty Company (DOWC), and profit-sharing

The company's Home & Utilities segment includes whole-home warranties, appliance protection, and mechanical breakdown coverage. AmTrust partners with manufacturers and service providers to build customized programs, though HVAC contractors seeking direct DOWC or reinsurance structures would typically work through AmTrust's participation programs rather than as individual retail clients.

| Program Model | Multi-Structure Carrier (First Dollar, Excess, CLIP, DOWC, Profit Share) |

|---|---|

| Key Services | Underwriting, program design, claims administration, customized warranty products |

| Best For | Large contractors or dealer groups seeking flexible program structures with carrier-level financial strength |

JB Warranties

Founded in 1996, JB Warranties is an employee-owned extended labor warranty provider holding 52% market share of the HVAC extended labor warranty market (ACCA/FCG study, 2026). The company has been named to the Inc. 5000 list five times, most recently in August 2024.

JB Warranties operates as a traditional third-party warranty provider — contractors purchase extended service agreements and resell them to homeowners. Plans include labor only, labor plus, parts and labor plus, or customized parts-only plans covering all brands. Agreements are transferable to new homeowners at no charge.

Key features include:

- 52% market share of HVAC extended labor warranties reflects widespread contractor adoption across the US

- Online platform — Streamlined purchasing, claims filing, and access to marketing materials with contractor branding

- Integration capability — Works with service management platforms for workflow efficiency

- Flexible terms — 10-year (48% of sales) and 5-year (20% of sales) agreements dominate

Important distinction: JB Warranties is not a reinsurance program. Contractors earn a margin on resale but do not participate in underwriting profits. This model offers simplicity and immediate implementation but limits long-term profitability compared to contractor-owned reinsurance structures.

| Program Model | Third-Party Warranty Provider (contractor resale model) |

|---|---|

| Key Services | Extended labor warranties, online platform, claims processing, marketing support |

| Best For | HVAC contractors seeking immediate warranty program with minimal setup and no ownership requirements |

How We Chose the Best HVAC Warranty Reinsurance Providers

Selecting a warranty reinsurance provider is not just about cost — a common mistake contractors make is choosing the lowest premium without evaluating the financial strength of the backing insurer, ownership of claims data, or the profitability structure of the program model.

Evaluation Framework:

Each selection criterion ties directly to a business outcome:

Program Model and Profit Ownership Structure

- Admin obligor structures allow contractors to retain underwriting profits

- Third-party resale models limit contractors to sales margins

Financial Backing and Insurer Credit Rating

- A-rated backing protects against insolvency risk

- The California DOI recommends checking financial strength ratings before purchasing service contracts

Administrative Support Quality

- Claims adjudication, compliance management, and bookkeeping reduce contractor overhead

- Full-service administration eliminates the need for internal warranty management staff

Transparency and Reporting

- Monthly financial statements and performance analysis enable profit monitoring

- Transparent fee structures prevent hidden costs

Track Record with HVAC or Home Service Contractors

- Providers with HVAC-specific experience understand seasonal claim patterns and equipment failure modes

- Industry specialization ensures compliance with HVAC-specific regulations

Why Admin Obligor Matters:

Contractors who want to build their own reinsurance company rather than resell a third party's program should specifically evaluate providers like WarrantyRE that offer the admin obligor model. This structure lets HVAC businesses invest premiums for additional ROI and retain the underwriting profits that third-party providers otherwise keep.

The Service Contract Industry Council (SCIC) confirms that service contracts should be backed by financially strong insurers, noting: "Many contracts are backed by A+ rated insurers to ensure financial solvency for long-term obligations."

Conclusion

HVAC contractors who are serious about scaling their warranty revenue should evaluate whether they want to continue sending profits to a third party or partner with a reinsurance provider that helps them own and operate their own warranty company.

The difference between these two models is substantial: the ACCA study shows third-party warranty programs deliver 24-30% margins, but admin obligor structures allow contractors to capture the full underwriting profit, meaning the difference between premiums collected and claims paid goes directly to the contractor.

Assess each provider not just on program structure but on long-term scalability and claims adjudication quality. A reinsurance partner that mishandles claims will damage customer relationships regardless of how profitable the program looks on paper. The strongest programs pair financial backing with contractor ownership — so warranty revenue stays in your business, not a third party's.

For HVAC contractors ready to capture those profits, WarrantyRE offers a proven path to owning your own warranty company — with full administrative support, A-rated insurance backing, and over 30 years of experience. Contact the WarrantyRE team at (804) 824-9533 to learn how to get started.

Frequently Asked Questions

How much does insurance cost for an HVAC contractor?

Standard business insurance — general liability, workers' comp, and commercial auto — typically costs $55–$127/month per coverage type depending on revenue and employee count, according to Simply Business data from 2024. Warranty reinsurance program costs are separate and vary based on warranty volume and program structure, not employee headcount.

What kind of insurance does an HVAC company need?

HVAC companies need general liability (third-party injury/property damage), workers' compensation (employee injuries), commercial auto (business vehicles), and often a contractor's license bond. Warranty reinsurance is a separate financial product that covers the risk of honoring warranty claims on HVAC systems sold or serviced — not a liability insurance policy.

Who are the top reinsurance companies?

Globally recognized carriers include Munich Re, Swiss Re, and Berkshire Hathaway Reinsurance, all holding A+ or A++ ratings from AM Best. For HVAC contractors, the more relevant question is which specialty program administrators — like WarrantyRE — have experience structuring programs for home service contractors. Global reinsurers don't work directly with individual HVAC businesses.

What is the difference between HVAC warranty reinsurance and a third-party warranty provider?

With a third-party provider, the contractor resells the warranty while the provider retains premiums, controls claims, and earns the profit. With an admin obligor reinsurance program, the contractor owns their own warranty company — keeping premiums, controlling claims, and earning the underwriting profit — with a reinsurer providing financial backing.

How do HVAC contractors profit from a reinsurance program?

Contractors profit two ways:

- Underwriting profit: The difference between premiums collected and claims paid stays with the contractor's reinsurance company, not a third party.

- Investment income: Premiums held in reserve can be invested for additional return, with all gains belonging to the contractor.

What is an administrator obligor reinsurance program?

In an admin obligor arrangement, the HVAC contractor's own company is the obligor — the entity legally responsible for fulfilling warranty obligations — with an A-rated reinsurance company providing financial backing. This structure allows the contractor to control claims, retain profits, and build long-term business value compared to simply reselling a third-party warranty product.