TL;DR

- Warranty lengths range from 90-day limited to "lifetime" — no single legal definition exists for service warranty durations

- Terms like "transferable," "conditional," and "pro rata" determine what coverage customers actually receive

- The Magnuson-Moss Warranty Act governs product warranties but not contractor workmanship warranties — leaving contractors both flexibility and full responsibility

- A "lifetime" warranty can mean the product's life, the company's existence, or coverage for the original owner only — each creates a very different obligation

- Without a financial structure behind it, every warranty claim a contractor makes comes straight out of their own pocket

Introduction

Warranty language sits in the fine print of nearly every home service contract — and most contractors treat it as an afterthought, which creates real financial exposure.

For HVAC contractors, roofers, plumbers, and electricians, the terms buried in a warranty document determine real liability exposure, who pays when something fails, and whether a customer dispute becomes a legal problem.

A 1-year workmanship warranty and a 10-year workmanship warranty aren't just different durations — they carry different financial obligations and different legal risks, with entirely different business models behind them.

Consumer Federation data published in June 2025 found that participating agencies handled over 350,000 consumer complaints in 2024, with home improvement ranking second among all categories. Warranty disputes drove a significant share of those complaints.

This article breaks down what warranty lengths actually mean, what critical terms govern real-world coverage, and what happens when contractors issue promises they can't financially support.

What Warranty Lengths and Terms Actually Mean

The Two Types Every Contractor Creates

A warranty is a legally binding promise that work or materials will perform as described — and a commitment to remedy defects if they don't. Contractors create two types, whether they intend to or not.

Implied warranties arise automatically under state law and the Uniform Commercial Code. Under UCC 2-314, goods sold by a merchant carry an implied warranty of merchantability — that they're fit for ordinary use. Under UCC 2-315, a fitness warranty applies when a buyer relies on the seller's judgment for a specific purpose.

The exposure window is longer than most contractors realize. UCC 2-725 gives customers 4 years from when a cause of action accrues to pursue a breach of warranty claim. A contractor's 1-year written warranty doesn't eliminate that risk.

Express warranties are explicit promises — written or verbal — made by the contractor. These are the warranties contractors control, define, and document.

Where Federal Law Draws the Line

The Magnuson-Moss Warranty Act, passed in 1975, requires written warranties on consumer products to be designated as either "full" or "limited" and mandates that terms be disclosed before sale. Under Magnuson-Moss:

- A full warranty must provide free repair or replacement, impose no unreasonable conditions, and remain available to anyone who owns the product during the warranty period

- A limited warranty permits restrictions on duration, labor coverage, scope, or transferability

- Products costing more than $15 require pre-sale disclosure of written warranty terms

The contractor-specific catch: Magnuson-Moss generally does not cover warranties on services alone. Contractor workmanship warranties fall outside its scope unless both parts and labor are covered together. At the federal level, service warranties are largely unregulated — which gives contractors real flexibility to structure their terms, but also places full responsibility on them for whatever they promise.

That federal gap doesn't mean contractors are free from mandatory warranty obligations. Many states impose their own statutory construction warranties regardless of what a contractor's written document says. Minnesota is a clear example:

| Defect Type | Statutory Period |

|---|---|

| Defective workmanship | 1 year |

| Faulty mechanical system installation | 2 years |

| Major structural defects | 10 years |

These state minimums apply independently of any warranty a contractor provides in writing.

The Range of Warranty Coverage: From Short-Term to Lifetime

Warranty length is a design decision. The range runs from 90-day limited coverage to unconditional lifetime guarantees, and the financial obligations attached to each are vastly different.

Short-Term and Standard Warranties

The National Roofing Contractors Association reports that roofing contractors typically issue workmanship warranties of 1 or 2 years. The NAHB's model express limited warranty uses 1 year from occupancy as the benchmark for latent defects in workmanship and materials.

Standard 1- and 2-year limited warranties typically:

- Cover workmanship defects only

- Exclude normal wear and tear

- Require the original purchaser to report issues within the period

- Do not eliminate implied warranty exposure under state law

For home service contractors, this is the baseline. HVAC installation warranties, plumbing service warranties, and electrical workmanship warranties commonly fall in the 1–2 year range.

Extended Coverage Warranties

Five- to 10-year warranties are common in roofing, HVAC, and foundation work. Roofing contractors may offer 5- or 10-year labor warranties. HVAC manufacturers provide useful context: Trane's registered limited warranty typically covers parts for 10 years, while Lennox's Signature series covers components and compressors for 10 years.

These are manufacturer parts warranties. Contractor labor warranties run parallel and are a separate obligation entirely.

Extended warranties are often structured with tiered coverage:

- Full parts and labor in years 1–2

- Parts-only coverage in years 3–5

- Proportional or reduced coverage beyond that

Each interpretation creates a different obligation, often much shorter than what the customer assumes. The FTC's advertising guidelines require that contractors using "lifetime" claims disclose which lifetime they mean. Vague advertising language that implies permanent, unconditional coverage can constitute a deceptive claim under FTC guidelines. Contractors advertising lifetime warranties must define the term in writing before the sale.

Critical Warranty Terms That Determine Real-World Coverage

Two warranties with identical durations can offer completely different protection depending on their terms. These four categories are where most disputes originate.

Transferability

A transferable warranty remains valid when a home changes ownership. A non-transferable warranty ends when the original purchaser sells. For roofing, HVAC, and other work with multi-year coverage periods, this distinction can matter more than the warranty length itself — many coverage periods outlast the original owner's time in the home.

Transfer requirements vary widely. Trane's registered limited warranty, for example, requires transfer within 90 days of home sale and charges a $99 fee. The NAHB model express limited warranty bars assignment without the contractor's prior written consent entirely.

Disputes commonly arise when:

- Second owners assume a warranty transferred automatically

- Transfer paperwork or fees were missed at closing

- Reduced or prorated coverage applies to transferred warranties

State transferability terms explicitly in writing — fees, deadlines, and notification requirements all included. Vague language here is what turns routine ownership changes into disputes.

Conditionality and Exclusions

Conditional warranties require ongoing customer compliance to remain valid. Common conditions include annual maintenance inspections, registration card submission, or use of approved service providers. Failure to comply can void coverage entirely.

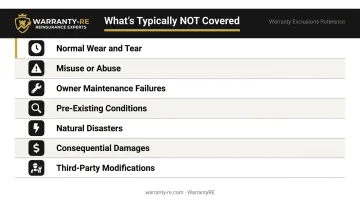

Standard exclusions found in home service warranties include:

- Normal wear and tear

- Damage from misuse or abuse

- Owner maintenance failures

- Pre-existing conditions

- Natural disasters or acts of God

- Consequential or incidental damages

- Third-party actions or modifications

The NAHB model express limited warranty includes all of these exclusion categories and requires written notice plus a defined service process before a claim is honored. When exclusion language is ambiguous, contractors lose disputes and end up paying claims they never intended to cover.

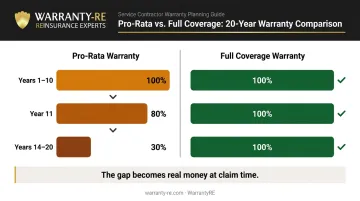

Pro Rata vs. Full Coverage

A pro-rata warranty decreases in value over time. A full coverage warranty provides the same remedy throughout the period.

The Western States Roofing Contractors Association provides a concrete example: a 20-year warranty may provide 100% coverage for the first 10 years, then drop to 80% of materials in year 11, and 30% in years 14–20. That gap becomes real money when a homeowner files a claim in year 15 and expects full replacement value.

| Coverage Period | Pro-Rata Example | Full Coverage |

|---|---|---|

| Years 1–10 | 100% materials | 100% materials |

| Year 11 | 80% materials | 100% materials |

| Years 14–20 | 30% materials | 100% materials |

Contractors structuring extended warranties should calculate their expected claim exposure under each model — the cost of a full-coverage 10-year program is considerably higher than a pro-rata equivalent.

What Goes Wrong When Warranty Terms Are Unclear or Unsupported

The most common failure pattern: a contractor issues broad warranty language without any financial mechanism to fulfill it. When claims arrive — and they do — the contractor either absorbs unexpected costs out of operating capital or defaults on the promise.

For HVAC, roofing, plumbing, and electrical contractors, every warranty callback represents technician time, fuel, parts, and margin leaving the business. Without a funded structure, each claim is a direct hit to profitability.

When the Company Closes

What happens to a warranty when the contractor goes out of business? Manufacturer warranties may survive — Trane or Lennox will still honor their parts coverage through the manufacturer. But contractor-issued workmanship warranties typically become unenforceable when the contractor closes, unless the warranty is backed by an insurance policy or a reinsurance structure.

The NAIC's Service Contracts Model Act provides that if a service contract provider fails to pay or provide service within 60 days after proof of loss, the contract holder may make a claim directly against the reimbursement insurer. This protection only exists when the warranty is backed by a licensed insurance entity.

WarrantyRE's reinsurance structures are backed by A-rated insurers, so if the contractor's reinsurance company cannot meet its financial obligations, the ultimate liability for claim payments rests with the direct writing insurance company. Customer warranties stay protected even if the contractor dissolves.

Legal and Regulatory Exposure

The FTC's June 2022 actions against Harley-Davidson and Westinghouse illustrate how warranty advertising enforcement works in practice. The FTC alleged both companies used illegal warranty terms implying coverage would be voided if customers used independent dealers — and alleged Harley-Davidson failed to disclose all warranty terms in a single document.

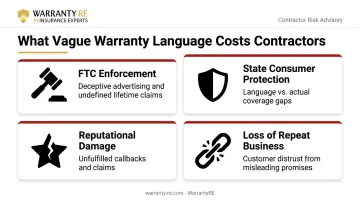

For contractors, the risk areas are:

- FTC enforcement for deceptive warranty advertising, including undefined "lifetime" claims

- State consumer protection claims where warranty language doesn't match actual coverage delivered

- Reputational damage from callbacks or claims the business can't fulfill

- Loss of repeat business when customers feel misled by warranty promises

Vague warranty language creates legal exposure and erodes the customer trust that drives repeat business.

Frequently Asked Questions

What happens to a lifetime warranty when a company goes out of business?

Manufacturer warranties may survive through the manufacturer directly. Contractor-issued workmanship warranties typically become unenforceable when the contractor closes — unless backed by a third-party insurer or reinsurance structure with A-rated support. Customers should confirm whether their warranty is insurance-backed before the contractor closes.

What is the difference between a full warranty and a limited warranty?

Under Magnuson-Moss, a "full" warranty must provide free repair or replacement without conditions and be available to anyone owning the product during the period. A "limited" warranty permits restrictions on duration, labor coverage, or transferability. Most home service workmanship warranties are limited.

What does a lifetime warranty actually cover?

"Lifetime" is not legally defined for service warranties and can mean the product's life, the structure's life, the original owner's life, or the company's existence. Before signing, ask the contractor to define "lifetime" in writing — and contractors should document it explicitly to avoid FTC advertising issues.

Can a home service warranty be transferred to a new homeowner?

Transferability depends entirely on the written terms. Some warranties transfer at no cost, others require fees and advance notification, and many are non-transferable. Trane's registered warranty, for example, requires transfer within 90 days with a $99 fee. Verify transfer terms in writing before any purchase or home sale.

What is the difference between a warranty and a service contract?

A warranty is included in the product or service purchase price — it's part of the original transaction. A service contract is a separately purchased agreement providing additional protection beyond the warranty. Both can apply simultaneously, but they are distinct legal agreements with separate obligations and enforcement mechanisms.

How much does a 100,000-mile extended auto warranty cost?

Costs vary significantly by vehicle age, mileage, coverage level, and provider — and Consumer Reports notes that extended warranty owners often pay more in premiums than they receive in repair benefits. Higher-mileage vehicles carry higher risk, which drives higher premiums. Get quotes from multiple providers and compare coverage terms, not just price.