Introduction

If you're an electrical contractor offering labor warranties, you're likely leaving significant money on the table. The residential and commercial electrical market represents a $195 billion industry in the United States, yet most contractors hand underwriting profits to third-party providers — profits that could stay in their own business.

Customers now expect coverage on panel upgrades, service calls, and installations. That expectation means contractors absorb the claims risk and customer relationship management, while external warranty companies capture the premium reserves and investment income that make these programs profitable.

Electrical warranty reinsurance changes this equation entirely. Instead of paying third-party providers to manage your warranties, you establish and own your own reinsurance company, backed by A-rated insurers, and retain 100% of underwriting profits in a tax-advantaged structure.

This guide breaks down what electrical warranty reinsurance is, which providers offer these programs, and what criteria matter most when choosing a partner that helps you own your warranty program instead of renting someone else's.

TL;DR

- Electrical warranty reinsurance lets you own your warranty company and capture underwriting profits instead of paying third parties

- The admin obligor model is most common—backed by A-rated insurers while you retain the financial upside

- Providers vary in how they handle compliance, claims adjudication, and contractor-specific program setup

- Look beyond premium splits—onboarding support, compliance management, and claims handling matter just as much

- WarrantyRE has served 400+ contractors since 1994 across electrical, HVAC, plumbing, and roofing trades

What Is Electrical Warranty Reinsurance?

Electrical warranty reinsurance is a financial structure where an electrical contractor establishes their own warranty company—typically as an administrator obligor entity—backed by A-rated reinsurers. Rather than paying third-party warranty companies to manage labor warranties, the contractor's company receives premiums, manages claims reserves through their administrator, and keeps the underwriting profit instead of passing it to an outside provider.

The Core Difference:

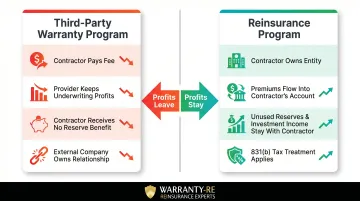

- Third-party warranty programs: Contractor pays a fee to an external provider. The provider keeps underwriting profits from premium reserves (money collected but not paid out in claims). Contractor receives no benefit from unused reserves.

- Reinsurance programs: Contractor owns the warranty entity. Premiums flow into the contractor's reinsurance account. After claims are paid, remaining reserves and investment income belong to the contractor's company, typically under IRS Section 831(b) tax treatment.

In practical terms, owning the warranty structure means the contractor stops funding someone else's profit margin. The home warranty service market hit approximately $9.12 billion in 2024 and is projected to reach $12.5 billion by 2029 — most of that underwriting profit flows to program owners, not the contractors selling the work.

Best Electrical Warranty Reinsurance Providers

Selection is based on experience in home service and electrical contractor programs, quality of administrative support, compliance track record, financial backing, and ability to scale with a contractor's business.

WarrantyRE

Background: WarrantyRE was founded in 1994 by Tim Byrd in Southeast Virginia and has operated for over 30 years. The firm has served 400+ clients, starting with automotive dealers before expanding into electrical, HVAC, plumbing, and roofing contractor markets nationwide.

Key Differentiators: WarrantyRE operates on an admin obligor model backed by A-rated insurers, handling all legal filings, tax returns, compliance, claims adjudication, and bookkeeping on behalf of the contractor. The contractor becomes the warranty company on paper, while WarrantyRE handles the operations. The firm's "we only succeed if you do" model aligns administrator compensation with contractor profitability, with no hidden fees.

| Feature | Details |

|---|---|

| Program Structure | Admin Obligor — contractor owns the reinsurance entity, backed by A-rated insurer |

| Support Provided | Full service: onboarding, training, claims adjudication, compliance, financial reporting, tax coordination |

| Market Served | Electrical, HVAC, plumbing, roofing, general contractors, auto dealers — nationwide |

Project Warranty

Background: Project Warranty operates in the contractor warranty reinsurance space, focusing exclusively on home service contractors including HVAC, plumbing, roofing, solar, foundation repair, and concrete leveling businesses. Project Warranty doesn't explicitly list electrical contractors on their industry pages, but their program targets "residential and commercial contractors" broadly and uses the same captive reinsurance structure applicable across trades.

Key Differentiators: Project Warranty helps contractors form a separate C-Corporation that operates as a reinsurance company owned and operated by the contractor. The program references IRS Section 831(b), allowing small insurance companies to underwrite up to $2.85 million in net written premium annually before underwriting profit becomes subject to federal income tax. Project Warranty provides business plan development, federal income tax and insurance regulatory compliance monitoring, and ongoing financial consulting. The firm emphasizes contractor control: "Everything involved in this program is yours; the business entity, the bank account and how the money is used."

| Feature | Details |

|---|---|

| Program Structure | Captive / 831(b) micro-captive — contractor owns separate C-Corp reinsurance entity |

| Support Provided | Entity setup, business planning, compliance monitoring, tax documentation, financial reporting and consulting |

| Market Served | HVAC, plumbing, roofing, solar, foundation repair, concrete leveling — implied nationwide |

iA American Warranty Group

Background: iA American Warranty Group (formerly IAS and SouthwestRe) has operated for over 35 years, primarily serving automotive dealers but explicitly stating they manage reinsurance accounts for "doctors, lawyers, contractors, and many others." Their insurance partner is Dealers Assurance Company (DAC), which holds an AM Best "A" (Excellent) rating—the only provider among the three to publicly name its carrier partner and rating.

Key Differentiators: iA American offers multiple profit participation structures including CFC (Controlled Foreign Corporation), NCFC (Non-Controlled Foreign Corporation), DOWC (Dealer-Owned Warranty Company), and Domestic Captive models. Their team handles company formation, corporate management, financial statement and tax return preparation, regulatory reporting, policy administration, and claims adjudication.

Their primary client base is automotive dealers. Electrical contractors should confirm home-service-specific program design directly before committing, though the explicit contractor mention and transparent AM Best "A" rated carrier backing make iA American worth a direct conversation.

| Feature | Details |

|---|---|

| Program Structure | Multiple models: CFC, NCFC, DOWC, Domestic Captive — contractor chooses based on tax and control preferences |

| Support Provided | Company formation, corporate management, financial statements, tax returns, regulatory reporting, policy admin, claims adjudication |

| Market Served | Primarily automotive dealers; contractors mentioned as secondary market — nationwide |

What to Look for in an Electrical Warranty Reinsurance Partner

Program Ownership Structure

The admin obligor model matters because contractors should own the reinsurance entity and retain underwriting profit—not just participate in a revenue-sharing arrangement. Verify that the backing insurer carries at minimum an A rating from AM Best.

According to AM Best's rating guide, an "A" (Excellent) Financial Strength Rating indicates "an excellent ability to meet ongoing insurance obligations." This ensures customer warranty claims will be honored even if the program administrator encounters financial difficulties.

Only iA American publicly names its carrier partner (Dealers Assurance Company, AM Best "A" rated). WarrantyRE references "A-rated" backing without naming the carrier. Project Warranty does not disclose its underwriting partner. For a structure where you're committing significant capital and long-term obligations, ask any prospective provider to name their carrier in writing before you commit.

Scope of Administrative Support

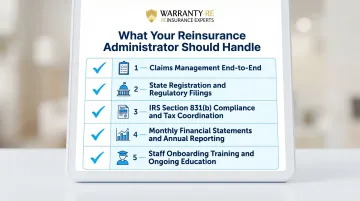

For most small and mid-size electrical contractors, the scope of administrative support determines whether a reinsurance program actually runs itself or becomes a second job. The right partner should handle:

- Manages claims end-to-end, from first customer call through final resolution

- Handles state-by-state service contract registration and regulatory filings

- Coordinates IRS Section 831(b) compliance and annual tax returns with your CPA

- Delivers monthly financial statements, annual reports, and performance tracking

- Trains your staff at onboarding and provides ongoing education as needed

A provider that handles only claims leaves you managing compliance, tax filings, and reporting internally — which defeats the purpose of having a program partner.

Track Record and Compliance History

Reinsurance programs operate within a regulated environment. Ask prospective providers:

- How long have you administered programs in the home service space?

- Do you have verifiable clients in the electrical contracting industry?

- What is your compliance history with state regulators and the IRS?

The IRS has placed micro-captive arrangements on its "Dirty Dozen" list of tax schemes, and 2025 final regulations established loss ratio thresholds: captives with loss ratios below 60% may be flagged as "transactions of interest," and those below 30% may be designated "listed transactions." Your provider must demonstrate genuine risk transfer, adequate risk distribution, and bona fide insurance operations to withstand IRS scrutiny.

Surviving IRS scrutiny over decades requires institutional knowledge that only comes with time. WarrantyRE has operated since 1994; iA American cites 35+ years of experience. Project Warranty does not publicly disclose its founding year. When compliance is this consequential, a provider's track record is not background noise — it's due diligence.

Alignment of Incentives

The ideal provider earns only when you earn — fee structures should reflect this directly. The structural difference matters:

- Third-party warranty model: The contractor earns a markup on sales; the provider and insurer keep underwriting profit and investment income

- Captive reinsurance model: The contractor retains all underwriting profit and investment income from unused premiums

WarrantyRE's messaging emphasizes this structural difference: "Capture 100% of the profits that your 3rd party warranty and insurance companies are keeping." However, no provider publicly discloses specific profit margin percentages or fee structures. Red flags include excessive setup fees, hidden charges, or opaque reporting. Require a detailed fee schedule in writing before you sign anything.

How We Chose the Best Electrical Warranty Reinsurance Providers

Evaluation Process

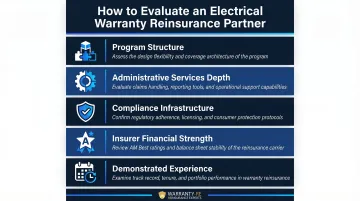

We assessed each provider across five criteria:

- Program structure: Admin obligor vs. captive vs. revenue share

- Depth of administrative services: Claims, compliance, tax, training, financial reporting

- Compliance infrastructure: IRS Section 831(b) expertise, state-by-state service contract compliance

- Insurer financial strength: AM Best rating of backing carrier

- Demonstrated experience: Years serving electrical and home service contractors

One common mistake: choosing a program based on premium split alone. A higher profit share means nothing if your staff is managing claims, filing compliance forms, and coordinating tax returns on the back end. These selection factors account for that full picture.

Selection Factors

- Backing insurer AM Best rating: Only programs backed by A-rated or higher carriers were included — ensuring claims are honored regardless of administrator viability.

- Years of experience in home service programs: WarrantyRE (founded 1994, 30+ years) and iA American (35+ years) have institutional depth. Project Warranty does not disclose a founding year but shows contractor-specific program design.

- Breadth of services: Full-service administration covering claims, compliance, tax, and training is essential. All three providers offer comprehensive support, though scope varies by program.

- Fee and retention transparency: No provider publicly discloses detailed pricing or retention metrics. WarrantyRE emphasizes "no hidden fees"; iA American states "nothing is hidden"; Project Warranty does not address fees on its website. Request this information directly during consultation with any provider.

Conclusion

Choosing an electrical warranty reinsurance partner isn't just a financial decision—it's an operational one. The right partner reduces admin burden, keeps your business compliant, and positions your warranty program as a recurring revenue stream rather than a liability.

Avoid choosing a provider based solely on program fees or premium splits. Prioritize:

- Full-service support that eliminates claims and compliance workload

- Financial strength with named, A-rated backing insurers

- Proven track records in electrical or home service contractor programs

- Transparent pricing with no hidden fees or surprise charges

WarrantyRE, Project Warranty, and iA American represent three viable options, each with distinct structural models, client focus areas, and transparency levels. Before committing, request detailed fee schedules, verify carrier backing, and confirm the program is designed specifically for home service contractors.

If you're an electrical contractor ready to stop paying third-party warranty providers and start owning your own program, WarrantyRE has been helping contractors do exactly that since 1994. Reach out to the team at (804) 824-9533 to explore whether a captive program fits your business.

Frequently Asked Questions

Who is the best extended warranty provider?

"Best" depends on whether you're a homeowner buying consumer coverage or a contractor setting up a business program. For electrical contractors looking to own their warranty program and capture underwriting profits, reinsurance program administrators like WarrantyRE, Project Warranty, or iA American are the relevant category—not consumer-facing warranty companies like home warranty providers sold to homeowners.

What is electrical warranty reinsurance?

Electrical warranty reinsurance allows electrical contractors to establish and own their own warranty company, backed by an A-rated insurer. The contractor retains warranty premiums and underwriting profits rather than paying them to a third-party provider—capturing those margins as tax-advantaged income under IRS Section 831(b) instead.

How does the admin obligor model work for electrical contractors?

The contractor's reinsurance entity acts as the obligor on warranties sold to customers, backed by a licensed A-rated insurer. A program administrator (like WarrantyRE) handles compliance, claims adjudication, and financials, while the contractor captures the underwriting profit and builds customer loyalty through branded warranty coverage.

What does it cost to set up an electrical warranty reinsurance program?

General captive formation costs run approximately $20,000–$100,000+ in year one, with ongoing management fees of $45,000–$65,000+ annually, per industry sources. Warranty-specific administrators don't always publish exact figures, so contact providers directly for a detailed fee schedule. Programs typically become self-funding once sufficient warranty volume is in place.

How is a reinsurance program different from buying a third-party warranty?

With a third-party warranty, the contractor pays a fee and the provider keeps the underwriting profit. With a reinsurance program, the contractor owns the entity, collects premiums, and retains the margin after claims are paid—with potential tax advantages under IRS Section 831(b) that third-party arrangements don't offer.

Can a small electrical contractor qualify for a reinsurance program?

Qualification is based primarily on projected warranty sales volume, not company size. WarrantyRE explicitly states that "the largest misconception is you must be very large in volume or that it costs a lot of money to get started. Neither are true!" Direct consultation with a provider like WarrantyRE at (804) 824-9533 will help assess eligibility based on your specific business profile.