Introduction

Utah issued 26,775 building permits in 2025 according to U.S. Census Bureau data. The Wasatch Front's residential boom, Silicon Slopes tech corridor, and resort communities in Park City and Deer Valley are driving sustained demand for licensed electrical work.

Staying licensed in Utah takes more than a Master Electrician on staff. Utah's Division of Occupational and Professional Licensing (DOPL) requires proof of specific insurance coverages before issuing or renewing an electrical contractor license — and the state's seismic exposure, harsh winters, and high-value commercial projects create risks that go well beyond those minimums.

This guide covers what Utah electrical contractors (E200/E201) actually need:

- DOPL licensing and insurance requirements

- Required and recommended coverages

- Utah-specific risk factors

- Cost benchmarks

- What commercial contracts typically demand

TL;DR

- Utah E200/E201 electrical contractors must carry general liability insurance with a minimum of $1,000,000 per occurrence and $3,000,000 aggregate, with DOPL listed as certificate holder.

- Workers' compensation is required for any business with employees; a waiver certificate is required if operating without employees.

- License bonds carry a $50,000 minimum — separate from insurance and required for E200/E201 licensing.

- Most contractors also need commercial auto, tools and equipment, and umbrella coverage beyond the state minimums.

- Utah electrical contractor licenses expire November 30 of odd-numbered years — a lapsed policy can trigger immediate license suspension.

Utah DOPL Requirements: Electrical Contractor Licensing and Insurance

DOPL — the Utah Division of Occupational and Professional Licensing — governs electrical contractor licensing in Utah. Proof of insurance isn't a post-licensing formality; it's a prerequisite for receiving your license in the first place.

License Classifications and Qualifications

Utah issues two electrical contractor license types:

- E200 – General Electrical Contractor: Covers commercial, industrial, and residential electrical work

- E201 – Residential Electrical Contractor: Limited to residential projects

Both classifications require:

- A Master Electrician qualifier — either the owner or a qualifying employee

- Completion of a 30-hour pre-licensure course (25 hours general + 5 hours Utah Business & Law topics)

- Passing the Utah Contractor Business and Law Exam, administered by Prov

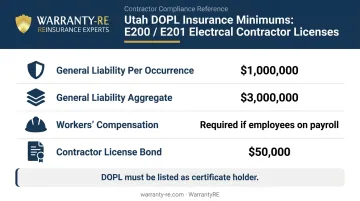

DOPL Insurance Minimums

DOPL's current requirements for E200/E201 contractors:

| Coverage | Minimum Required |

|---|---|

| General Liability (per occurrence) | $1,000,000 |

| General Liability (aggregate) | $3,000,000 |

| Workers' Compensation | Required if employees are on payroll |

| Contractor License Bond | $50,000 |

The general liability certificate must list DOPL as certificate holder at: DOPL, 160 E 300 S, Salt Lake City, Utah, 84111.

If your business has no employees and you don't want workers' comp coverage for yourself, you must submit a Workers' Compensation Coverage Waiver Certificate from the Utah Labor Commission.

License Renewal

Keeping your insurance current doesn't end at licensure — it's an ongoing obligation tied directly to renewal. Utah electrical contractor licenses expire November 30 of odd-numbered years. Renewal requires:

- 6 hours of continuing education (including 3 live hours)

- $128 renewal fee

- A current certificate of insurance meeting DOPL minimums

Any lapse in coverage, however short, can trigger license suspension. You cannot legally operate on any job site until coverage is restored and proof is re-submitted to DOPL.

Required Insurance Coverages for Utah Electrical Contractors

General Liability Insurance

General liability is the foundational required policy. It covers third-party bodily injury and property damage arising from your operations and completed work. For electrical contractors, that means coverage for scenarios like:

- Electrical fires caused by faulty wiring during or after installation

- Shock or burn injuries to building occupants

- Physical property damage during rough-in or panel work

The state minimum is $1,000,000 per occurrence / $3,000,000 aggregate, but most commercial project owners and GCs require limits well above that threshold.

Pay close attention to the completed operations component. Every project you sign off on represents a potential future claim — completed operations coverage extends protection after the job is finished. If a wiring fault causes a fire 14 months after project completion, this coverage responds. For electricians doing panel upgrades, service changes, or complex commercial installations, that tail exposure is real.

Workers' Compensation Insurance

Any Utah electrical contracting business with employees is legally required to carry workers' comp. It covers:

- Medical bills for on-the-job injuries

- Lost wages during recovery

- Disability costs for permanent impairments

Electrical work carries some of the highest injury severity of any trade. Arc flash injuries, falls from ladders and scaffolding, and electrocution are not theoretical risks — they're documented hazards that can result in catastrophic, career-ending injuries.

Those risks directly affect your premiums. Utah workers' comp premiums for electricians are calculated based on payroll using NCCI classification codes. The applicable code for within-building electrical wiring is NCCI Code 5190 (Electrical Wiring – Within Buildings & Drivers). Precise Utah-specific rates per $100 of payroll aren't publicly published, but NCCI's 2025 filing proposed a 4.5% decrease to Utah voluntary-market loss costs effective February 2026.

Contractor License Bond

A contractor license bond is not insurance. It's a financial guarantee that you will perform work in compliance with your license and state regulations. If you fail to meet those obligations, the bond protects the public — not you.

For E200/E201 electrical contractor classifications, DOPL requires a minimum $50,000 bond. This is purchased through an insurance carrier or bonding company and maintained separately from your general liability policy. Both must be current for license renewal.

Recommended Additional Coverages Beyond State Requirements

Commercial Auto Insurance

Work trucks and cargo vans used for business must be covered under a commercial auto policy — personal auto policies typically exclude business use and will deny claims if a vehicle was being used for work at the time of an accident.

Commercial auto covers:

- At-fault accident liability

- Physical damage to your vehicle

- Medical expenses for injured parties

Utah's current minimum auto liability requirements (for policies issued or renewed on or after January 1, 2025) are $30,000 bodily injury per person / $65,000 per accident / $25,000 property damage. These minimums are rarely adequate for a loaded service van. If an employee uses their personal vehicle on a job, hired and non-owned auto coverage fills the gap your commercial auto policy would otherwise leave.

Tools and Equipment Insurance (Inland Marine)

A standard commercial property policy only covers assets at a fixed location. It won't cover tools stolen from your truck, specialty testing equipment lost on a remote job site, or staged materials damaged overnight at a construction site.

An inland marine / tools and equipment policy covers these assets wherever they are:

- Hand tools and power tools

- Specialty meters, testers, and diagnostic equipment

- Staged materials at the job site

Utah's mountain construction sites — particularly in resort communities like Deer Valley and Park City — present limited site security and difficult access. The theft and damage risk for unsecured equipment in remote locations is substantially higher than on a locked urban job site.

Umbrella / Excess Liability

An umbrella policy sits above your general liability, commercial auto, and employers liability policies and extends total limits across all three. It's the most cost-effective way to reach the higher limits commercial contracts demand.

Data centers, university builds, government projects, and resort construction on the Wasatch Front routinely require $2,000,000 to $5,000,000 or more in total liability limits. A $1,000,000 GL policy alone won't get you in the door.

Beyond Compliance — Contractor-Owned Warranty Programs

With insurance compliance handled, it's worth looking at another line item in your job pricing: the warranty fees you're already collecting — and where they go.

Most electrical contractors offer labor warranties on panel installations, wiring, and fixture connections — but every callback comes out of pocket, and any unused warranty reserves flow to a third-party provider.

WarrantyRE's model lets electrical contractors establish their own administrator-obligor reinsurance company to replace that arrangement. A warranty fee is built into every job price, flows into a structure the contractor legally owns, and unused funds stay with the contractor rather than going to an outside company.

This is a financial strategy layered on top of the required insurance coverages described above — not a substitute for them. WarrantyRE handles all claims administration, legal filings, and compliance management. Contractors interested in how the structure works can reach WarrantyRE directly at (804) 824-9533.

Utah-Specific Risks That Shape Your Coverage Needs

Seismic Exposure from the Wasatch Fault

According to the USGS Fact Sheet 2016-3019, there is a 43% probability that the Wasatch Front region will experience at least one M6.75 or greater earthquake in the next 50 years. The Utah Geological Survey's data supports the same figure.

For electrical contractors, this matters in two practical ways:

- Earthquake-resistant installation standards may affect how you scope and price jobs

- Equipment and materials staged on job sites could be damaged in a seismic event — verify whether your inland marine and builders risk policies exclude earthquake damage

Winter Working Conditions

Utah winters create real exposure for electrical contractors on outdoor and exterior jobs. Freezing temperatures, ice, and wind push workers' comp risk well beyond what the standard NCCI classification code assumes.

The practical consequences compound quickly:

- Arc flash risk increases when you're working a live panel on an icy scaffold

- A serious winter injury spikes your experience modification rate (EMR) for three years

- A higher EMR directly increases workers' comp premiums on every future renewal

Mountain and Resort Construction

Electrical work in Park City, Deer Valley, and similar resort communities carries a distinct set of exposures:

- High-value properties with substantial completed operations exposure

- Remote access and limited site security amplify tools and equipment loss

- Weather delays can leave staged materials unsecured for extended periods

- Verify how your builders risk and installation floater coverage applies to materials not yet permanently installed

How Much Does Electrical Contractor Insurance Cost in Utah?

Costs vary significantly by business size, scope of work, and coverage structure. The main premium drivers:

- Payroll — workers' comp is payroll-based; larger crews mean higher premiums

- Claims history and EMR — a strong safety record directly reduces your workers' comp costs

- Scope of work — commercial electrical work carries higher GL premiums than residential

- Coverage limits — contract requirements pushing you to $2M–$5M total will increase umbrella costs

- Geographic location — Wasatch Front vs. southern Utah markets may see different carrier appetite (a carrier's willingness to insure certain risks in a given area)

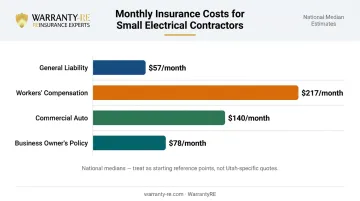

Using national benchmarks from Insureon's electrician insurance data (updated October 2025) as reference points:

| Coverage | Median Monthly Cost |

|---|---|

| General Liability | $57/month |

| Workers' Compensation | $217/month |

| Commercial Auto | $140/month |

| Business Owner's Policy (BOP) | $78/month |

These are national medians for small electrical businesses and should be treated as starting reference points, not Utah-specific quotes. A solo operator with no employees carrying GL only will pay considerably less than a crew of eight running full commercial work.

Understanding where your costs land is the first step. Managing them is the next. Three practical ways to keep premiums in check:

- Maintain a documented winter safety program — ice, snow, and cold weather protocols can support a lower EMR (Experience Modification Rate) over time

- Verify employee classifications under the correct NCCI codes; these codes determine your workers' comp rate, and misclassification leads to audit adjustments and unexpected bills at renewal

- Bundle GL, commercial auto, and umbrella with a single carrier for potential multi-policy discounts

Contract Insurance Requirements for Commercial Projects

DOPL minimums get you a license. They don't get you on a commercial job site.

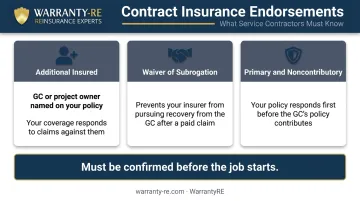

Utah's commercial GCs, project owners, data center developers, and public agencies routinely require subcontractors to carry coverage beyond state minimums. The three most common contract-specific requirements:

- Additional Insured — the GC or project owner is named on your policy, so if your work causes a claim against them, your policy covers it

- Waiver of Subrogation — prevents your insurer from pursuing recovery from the GC after paying a claim on your behalf

- Primary and Noncontributory — your policy responds first, before the GC's policy contributes anything

These endorsements must be confirmed and in place before the job starts, not the week of your first scheduled work. Missing a GC's certificate of insurance requirements can pull you from an active project — or keep you off the bid list entirely.

On larger Wasatch Front projects — data centers, university construction, government contracts, resort builds — total required limits of $2,000,000 to $5,000,000 are common. An umbrella policy is the standard mechanism for reaching those thresholds.

Before submitting your certificate, confirm your umbrella sits cleanly over your GL, commercial auto, and employers liability policies. That alignment is what satisfies primary and noncontributory wording.

Frequently Asked Questions

What type of insurance should an electrical contractor in Utah have?

At minimum, a Utah E200/E201 contractor needs general liability ($1M/$3M) and workers' compensation if they have employees. Most also carry commercial auto, tools and equipment coverage, and an umbrella policy to meet commercial contract requirements and protect business assets.

How much does electrical contractor insurance cost in Utah?

Costs depend on business size, payroll, scope of work, and claims history. National benchmarks suggest GL around $57/month and workers' comp around $217/month for small electrical businesses — but full commercial programs with multiple coverages will run well above those figures. Get quotes from a broker familiar with Utah electrical contractors.

Is there a difference between an electrician and an electrical contractor?

An electrician is an individual trade professional licensed at the apprentice, journeyman, or master level through DOPL. An electrical contractor is a business entity holding an E200 or E201 license that employs electricians and takes on contracts. That distinction comes with separate insurance and bonding obligations.

What is the minimum general liability insurance for a Utah electrical contractor license?

DOPL currently requires $1,000,000 per occurrence and $3,000,000 aggregate for E200/E201 electrical contractor licenses, with DOPL listed as certificate holder on the policy.

What happens if my insurance lapses as a Utah electrical contractor?

DOPL can suspend your contractor license for any coverage lapse. You cannot legally operate on any job site until coverage is restored and a current certificate of insurance is re-submitted to DOPL.

Do I need a bond in addition to insurance for my Utah electrical contractor license?

Yes. A $50,000 contractor license bond is required separately from your general liability insurance for E200/E201 classifications. The bond is a financial guarantee of compliant work — not a substitute for liability coverage.