](https://file-host.link/website/warranty-re-5tv26p/assets/blog-images/5bb3f4ce-8287-4900-9f17-283068793eac/1776809947383701_7ac5fb797d964b32aaeb67ad70346499/360.webp)

Introduction

Business owners—auto dealers and home service contractors alike—are paying third-party warranty companies to keep profits that should belong to them. NADA data reports that F&I profit per retailed unit averages $1,944 for new vehicles and $2,354 for used vehicles, yet the bulk of this margin flows to third-party administrators rather than staying with the dealer. Home service contractors face a similar reality: the global home warranty market reached approximately $9.12 billion in 2024, with contractors shouldering warranty costs while outside providers capture the underwriting profits.

Starting a warranty reinsurance company shifts this dynamic. By establishing your own captive reinsurance structure, you recapture the underwriting profit (the difference between premiums collected and claims paid) that third-party providers currently pocket. For most businesses, startup costs range from a few thousand dollars to $30,000 or more depending on structure and volume. This article breaks down what drives those numbers, which line items matter most, and how to tell whether the investment makes sense for your operation.

TL;DR

- Startup costs range from a few thousand dollars for basic formation to $25,000+ for complex structures

- Main cost drivers include formation fees, initial capital requirements, annual compliance, ceding fees, and premium taxes

- Structure complexity scales with volume — most contractors and dealers start leaner than they expect

- Setup costs are modest relative to the underwriting profits currently going to third-party providers — profits that could be yours

How Much Does It Cost to Start a Warranty Reinsurance Company?

There is no single fixed cost. Your total investment depends on the structure you choose (CFC, Admin Obligor, DOWC), the domicile of the company, your warranty sales volume, and whether you use a managed service or handle formation independently.

When costs are misunderstood, two things go wrong: owners either underbudget and face compliance gaps down the road, or overestimate and delay starting entirely. Both outcomes cost far more than the formation itself.

Here's what to expect at each level.

Entry-Level / Basic Setup

A basic formation typically involves a simple CFC (Controlled Foreign Corporation) structure or Admin Obligor program with low initial capital deposit.

What you can expect:

- Attorney and formation fees: approximately $4,000-$6,000

- Minimum capital deposit: $5,000 (IRS-recommended floor based on industry guidance)

- First-year filing and licensing fees: $1,000-$2,000

Total entry-level range: $10,000-$13,000

This tier covers company formation, basic compliance filings, and minimum capitalization. It does not include investment management, broad product offerings, or advanced tax optimization strategies.

Best for: Lower-volume dealers or contractors testing the reinsurance model for the first time, or those starting with a single product category (e.g., VSCs only or labor warranties for one trade).

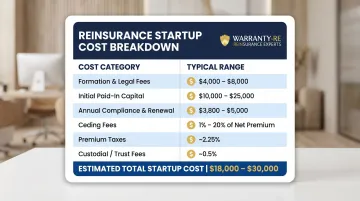

Mid-Range / Standard CFC or Admin Obligor Setup

A fully structured CFC or Admin Obligor reinsurance company includes formation fees, adequate capitalization, first-year ceding fees, premium taxes, and custodial/trust account fees.

Core cost components:

- Formation and legal fees: $4,000-$8,000

- Initial paid-in capital: $10,000-$25,000 (scaled to your initial warranty volume)

- Annual compliance and renewal fees: $3,800-$5,000

- Ceding fees: 1%-20% of net premium (varies by fronting carrier and volume)

- Premium taxes: approximately 2.25% of gross premiums (Georgia example)

- Custodial/trust account fees: approximately 0.5% (50 basis points)

Total mid-range all-in cost: $18,000-$30,000 for year one

Best for: Established dealers or contractors selling moderate warranty volume who want full underwriting profit participation and tax advantages under IRC Section 831(b).

Full-Service / DOWC or Advanced Structure

A DOWC (Dealer Owned Warranty Company) or hybrid domestic structure operates as a domestic insurance entity. It carries higher regulatory requirements, longer formation timelines, and greater capitalization needs. In exchange, it delivers maximum tax efficiency and profit control.

What this tier entails:

- Statutory capital requirement: $250,000-$1,000,000+ (depending on state domicile)

- Formation and legal fees: $10,000-$20,000

- Regulatory approval timeline: 3-6 months

- Seeding period before full tax benefits: 12-24 months

- No offshore compliance complexity (no FBAR reporting, no Subpart F)

Total advanced structure cost: $260,000-$1,050,000 upfront, with 1.5-2.5 years to full operational status

Best for: High-volume dealers or growing home service contractors who want maximum control, domestic domicile, and long-term tax efficiency and profit accumulation.

Breaking Down the Costs: What You're Actually Paying For

The total cost to start a reinsurance company goes beyond the one-time formation fee. There are startup (one-time) and ongoing (recurring) cost categories that you must budget for separately.

Formation and Legal Fees (One-Time)

Formation fees cover the full legal setup of your reinsurance entity. This typically includes:

- Attorney fees to create the company structure

- Reinsurance license (commonly in an offshore domicile like Turks and Caicos for a CFC)

- Corporate documents and stock certificates

- Tax ID number, IRS 953(d) filings, and 831(b) election

Typical range: $4,000-$20,000

Domestic DOWC structures may involve different regulatory and filing costs depending on state requirements. Offshore CFC structures tend to fall at the lower end of this range due to streamlined licensing in jurisdictions like Turks and Caicos.

Initial Paid-In Capital (One-Time)

The IRS requires reinsurance companies to have initial paid-in capital to be considered viable insurance entities (per IRS TAM 200323026). While no specific minimum amount is mandated, industry guidance suggests at least $5,000, with adequate capitalization relative to your starting risk strongly advised.

Key principle: This capital sits in a trust account and is not "spent." It seeds the company's reserves and backs your risk-bearing capacity.

Annual Compliance and Renewal Fees (Recurring)

These cover attorney and CPA firm fees for annual renewals, books and records maintenance, tax preparation, and annual filings.

Typical range: $3,800-$5,000 per year

WarrantyRE handles all legal forms, filings, tax returns, and renewals as part of their administration package — no surprise fees, no tracking deadlines yourself.

Ceding Fees (Recurring)

Ceding fees are charged by the admitted (fronting) carrier that transfers the risk and premium reserves to your reinsurance company. Providers typically quote these as a percentage of the actual premium reserve.

Typical range: 1%-20% of net premium

Some providers bundle this into an administration fee while others charge separately. High ceding fees can erode underwriting profits over time, so comparing provider fee structures is critical.

Premium Taxes and Custodial/Investment Fees (Recurring)

Premium taxes: Based on actual amounts paid by the insurance company in the state of filing. For example, Georgia's state premium tax rate is 2.25%.

Custodial/trust account fees: Charged by the money manager overseeing the brokerage account holding your reserves. A NAIC white paper on reinsurance collateral estimates trust and LOC fees at 40-60 basis points, with typical custodial fees around 0.5% (50 basis points).

Warning: Some investment managers also charge hidden proprietary fund fees. Always ask for full fee disclosure before committing.

Key Factors That Affect Your Total Startup Cost

Three variables drive the difference in total startup cost: structure type, domicile, and the scale of your operation at launch.

Structure Type

Each structure type carries a different cost profile:

- Retro/bonus programs: Minimal upfront cost but lower profit participation (you share profits with the carrier)

- CFC structures: Involve formation and ceding costs but offer IRC 831(b) tax advantages—premiums up to approximately $2.8 million (2024 cap) are taxed at 0% on underwriting income

- DOWCs: Higher regulatory startup costs ($250K-$1M capital) but maximum domestic tax efficiency, with claims paid and statutory reserves deductible as business expenses

Domicile Choice

Where the company is domiciled affects licensing costs, ongoing compliance fees, and IRS treatment.

Offshore domiciles like Turks and Caicos are common for CFC structures. The Turks and Caicos Islands Financial Services Commission regulates insurance business under the Insurance Ordinance 1998, with licensing fees and formation costs that typically run lower than domestic DOWC requirements.

Domestic DOWC structures face state-level regulatory requirements. Vermont and Tennessee are commonly chosen for streamlined captive regulations.

Caution: Avoid providers using non-compliant domiciles as workarounds. IRS Notice 2016-66 identifies certain 831(b) micro-captive transactions as "transactions of interest" requiring Form 8886 disclosure, with penalties up to $50,000 per failure for individuals and $200,000 for entities.

Volume and Risk Level at Launch

Capital and reserve requirements scale directly with the volume of warranties you're writing. A contractor selling 10 service contracts per month carries a very different risk exposure than one selling 100—and your structure should reflect that.

Undercapitalizing to cut startup costs is one of the most common mistakes. The IRS evaluates whether capitalization is adequate relative to the risks actually assumed. Specific red flags include:

- Reserves set below projected claims exposure

- Premium levels disproportionate to the risk written

- No actuarial support for the pricing structure

- Capital that doesn't grow as contract volume scales

If the arrangement doesn't hold up to that scrutiny, the IRS can challenge whether it qualifies as insurance at all.

What Most People Miss When Budgeting for Reinsurance

Most budgeting mistakes don't happen on the formation side — they happen in the gaps. Three blind spots trip up the majority of dealers and contractors entering reinsurance for the first time:

- Formation fees are just the entry ticket. The real financial picture includes ongoing compliance, ceding fees compounding over years, and investment management costs. The gap between "cost to start" and "cost to operate" is where budgets break down.

- Delaying has a real dollar cost. NADA data shows F&I profit per retailed unit at $1,944 for new vehicles and $2,354 for used. Selling 20 service contracts per month at an average premium reserve of $800, with a 50% loss ratio, means roughly $8,000 per month ($96,000 annually) in underwriting profit left on the table. Every month of delay compounds that loss.

- Cheap providers often hide fees elsewhere. Some advertise zero ceding fees but embed those costs in administration fees. Others use non-compliant domiciles that create downstream IRS and legal exposure that dwarfs any upfront savings. Before committing, ask for full itemized fee disclosure (including any proprietary investment fund fees).

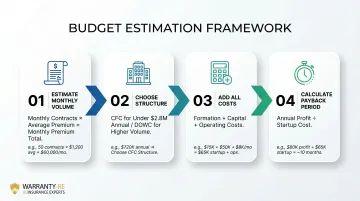

How to Estimate the Right Budget for Your Business

Follow this simple framework for self-assessment:

- Estimate monthly warranty volume and average premium reserve per contract

- Example: 20 contracts/month × $800 average premium = $16,000 monthly premium

- Determine which reinsurance structure fits your volume and tax situation

- Under $2.8M annual premiums: CFC with 831(b) election

- Higher volume or preference for domestic structure: DOWC

- Add up formation + capital + first-year operating costs

- Use the cost breakdown categories above

- Include ceding fees, premium taxes, and custodial fees

- Compare total cost to projected annual underwriting profit to determine payback period

- Example: $16,000/month × 50% loss ratio = $8,000/month profit × 12 = $96,000 annually

- If startup cost is $20,000, payback period is approximately 2.5 months

What pushes cost up:

- Higher volume justifies more complex (and more expensive) structures

- Domestic DOWC requires significantly higher capital ($250K-$1M)

- Multiple product categories increase administrative complexity

What pushes cost down:

- Lower volume means starting with a simpler CFC or Admin Obligor program

- Offshore domiciles reduce regulatory overhead

- Managed-service providers eliminate in-house compliance staffing costs

Running this framework gives you a clearer picture—but the right structure depends on details specific to your business volume, tax situation, and growth goals. WarrantyRE works with dealers and home service contractors to run that analysis, select the right structure, and handle all formation, legal filings, tax returns, and renewals from start to finish. Call (804) 824-9533 or visit warranty-re.com to start your owner analysis.

Frequently Asked Questions

What is the capital requirement for reinsurance companies?

The IRS requires reinsurance companies to have initial paid-in capital to be treated as viable insurance entities, though no specific dollar minimum is mandated by law. Industry guidance recommends capitalizing at a level commensurate with starting risk—a minimum of $5,000 is commonly cited as a floor, with higher-volume operations requiring proportionally more.

Is reinsurance a profitable business?

Yes, warranty reinsurance can be highly profitable. Owners capture the underwriting profit — premium reserves not used to pay claims — that would otherwise go to a third-party provider. Profitability scales with warranty volume, loss ratio management, and investment returns, with IRC 831(b) tax advantages adding further upside for qualifying small insurers.

Can small dealerships or contractors afford to start a warranty reinsurance company?

A large operation is not required. Entry-level CFC or Admin Obligor setups carry modest formation costs (approximately $10,000–$13,000), and a managed service provider handles ongoing administration without requiring dedicated dealer staff. Many smaller contractors and dealers benefit from reinsurance at volumes that most assume wouldn't qualify.

How long does it take to set up a warranty reinsurance company?

A basic CFC or Admin Obligor structure can be formed in weeks with the right team. A domestic DOWC typically requires 3–6 months for regulatory approval, plus a 12–24 month seeding period before full tax benefits activate. Working with a full-service provider like WarrantyRE can shorten that timeline considerably.

What is the difference between a CFC and a DOWC reinsurance structure?

A CFC (Controlled Foreign Corporation) is an offshore entity — the most common structure — that allows tax-deferred premium income via a 953(d) election. A DOWC (Dealer Owned Warranty Company) is a domestic insurer that can offer greater long-term tax efficiency as the book matures, but requires $250K–$1M in startup capital and carries more regulatory complexity.