The gap is costly. U.S. public homebuilders paid over $1 billion in warranty claims in 2024, with average warranty accruals running $2,739 per new home sold. For contractors without a clear warranty strategy, those numbers represent pure liability.

This guide breaks down what new construction warranties require, what they exclude, how claims and disputes work in practice, and how the smartest contractors are flipping warranty obligations from a cost center into a profit driver.

TL;DR

- New construction warranties follow a three-tier structure: 1 year for workmanship, 2 years for major systems, up to 10 years for structural defects.

- Both express (written) and implied (legally automatic) warranties apply in most states. Contract language alone won't eliminate all liability.

- Written notice, proper documentation, and following dispute procedures are non-negotiable when handling claims.

- Contractors can capture the underwriting profit that third-party warranty companies currently keep by establishing a contractor-owned reinsurance structure.

What Is Contractor Warranty Coverage for New Construction?

Contractor warranty coverage is a promise — written, implied, or both — that the work performed meets certain quality and performance standards for a defined period after completion or sale.

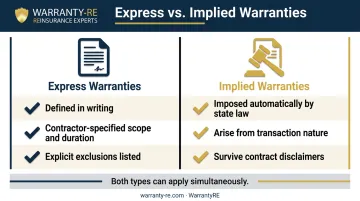

Two distinct types apply to new construction:

- Express warranties: explicitly stated in writing, with defined scope, duration, and exclusions. These are what most contractors think of when they hear "warranty."

- Implied warranties: imposed automatically by law, regardless of contract language. They arise from the nature of the transaction itself, not from anything the contractor agreed to in writing.

Implied warranties catch many contractors off guard. Most states impose some version of an implied warranty of habitability or workmanship on new home construction, which means a contractor can face legal liability even without a written warranty ever being offered.

State laws vary significantly. Contractors should verify the specific rules in their jurisdiction before assuming any written disclaimer provides full protection.

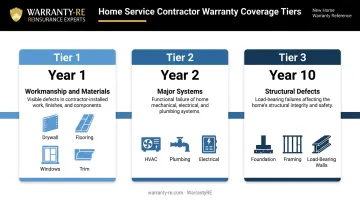

The Three Tiers of New Construction Warranty Coverage

According to the FTC, builder warranties generally follow a standard three-tier framework covering workmanship, major systems, and structural defects. Federal agency requirements and standard builder practice reflect this same structure.

Year 1 — Workmanship and Materials

The first year typically covers defects in workmanship and materials: drywall, flooring, trim, paint, siding, windows, and exterior caulking. "Defective workmanship" means work that fails to meet accepted trade standards or violates local building codes — not just work the buyer doesn't like.

Common exclusions at this tier:

- Cosmetic issues within normal tolerances (minor settling cracks, paint touch-ups)

- Damage caused by homeowner misuse or modifications

- Items covered under a separate manufacturer's warranty

Year 2 — Major Systems (HVAC, Plumbing, Electrical)

The second year extends coverage to a home's major mechanical systems. HVAC, plumbing, and electrical are included because failures in these systems typically result from installation errors — not product defects — which is why they warrant a longer coverage window.

This tier applies to installation-related failures only. Normal wear and tear, system abuse, and component failures already covered by equipment manufacturer warranties fall outside it.

Year 10 — Structural Defects

The most significant tier covers major structural defects — physical damage to load-bearing components (foundation, framing, load-bearing walls, roof structure, beams) that render the home unsafe, unsanitary, or uninhabitable.

That distinction drives claim outcomes. A crack in drywall is a cosmetic issue — denied. A crack in a load-bearing foundation wall is a structural defect — and the most expensive claim a contractor can face.

These tiers also interact with loan-type requirements that vary by program. VA guidance, for instance, requires new construction to be covered by either a one-year VA builder's warranty (VA Form 26-1859) or a 10-year insurance-backed protection plan acceptable to HUD. FHA, by contrast, eliminated its 10-year protection plan requirement via HUD Mortgagee Letter 2019-05, effective March 14, 2019, retaining only the one-year Warranty of Completion of Construction. Contractors working with VA-financed buyers need to account for this distinction.

What New Construction Warranties Typically Exclude

A well-drafted express warranty should clearly define what is not covered. The FTC identifies the most common exclusions:

- Household appliances — covered separately under manufacturer warranties

- Minor cosmetic cracking — small cracks in tile, brick, drywall, or concrete within normal tolerances

- Homeowner-caused damage — modifications, neglect, failure to maintain

- Third-party work — repairs or changes made after the builder's work was completed

- Acts of nature — damage from site conditions or weather events outside the contractor's control

- Temporary expenses — relocation costs and out-of-pocket expenses resulting from defect repairs

The Implied Warranty Problem With Disclaimers

Many contractors assume their written exclusions eliminate implied warranty exposure — they often don't.

New York's General Business Law §777-A is a clear example. The statute creates a housing merchant implied warranty that survives title transfer, covering construction defects for 1 year, plumbing, electrical, and HVAC installation defects for 2 years, and material defects for 6 years.

Under GBL §777-A, contract provisions that exclude or modify this implied warranty are void — unless the contractor follows the specific limited-warranty substitution procedure under GBL §777-B, which requires offering the buyer a qualifying limited warranty in writing before signing.

Virginia follows a similar approach. A waiver of the implied warranty under Virginia Code §55.1-357 requires conspicuous capital-letter language at least two points larger than the surrounding text.

Written exclusion clauses don't automatically eliminate implied warranty exposure. Before finalizing warranty language, contractors should confirm with legal counsel exactly which disclaimers are enforceable in their state — and which are void regardless of what the contract says.

Implied Warranties vs. Express Warranties: What Every Contractor Needs to Know

Implied warranties arise automatically under state law whenever a contractor builds or sells a new home. "Let the buyer beware" has no application to new residential construction in most jurisdictions — buyers have warranty protections whether or not a written warranty was ever offered.

The practical risk this creates is significant. A homeowner can pursue a warranty claim even if the written contract contains no warranty at all, if the applicable statute of limitations hasn't expired. Limitation periods vary by state and defect type:

| State | Applicable Period |

|---|---|

| California | 10 years for latent deficiencies (CCP §337.15) |

| Texas | 10 years construction repose (Prop. Code §16.009) |

| New York | 6 years for contract actions (CPLR §213) |

| Florida | 4-year period, 7-year outside limit (current 2025 statute) |

Contractors can sometimes replace an implied warranty with a written limited warranty — but only if it meets minimum statutory standards. Keep these points in mind:

- A written warranty cannot legally shorten coverage below what state law mandates

- States like New York and Virginia impose specific procedural requirements for the substitution to be valid

- Contractors working across multiple states must verify each jurisdiction's rules individually

Assuming one state's rules apply everywhere is the most expensive warranty mistake contractors make.

How Contractors Handle Warranty Claims and Disputes

The Standard Claims Process

Most new construction warranty programs follow a consistent process:

- Homeowner submits written notice — within the required timeframe, identifying the defect and its location

- Contractor receives the right to inspect and cure — a reasonable opportunity to evaluate and repair before any legal action can proceed

- Repairs are made according to warranty terms, with documentation kept throughout

Written notice requirements are strictly enforced in most jurisdictions. State-specific rules include:

- Texas: Written notice required at least 60 days before filing a construction defect action

- Florida: 60 days' notice (120 days for associations covering more than 20 parcels)

- California: Notice must be sent via certified mail or personal delivery

Homeowners who skip these steps can have claims dismissed. Contractors who fail to document their receipt of notice, inspection, and completed repairs are left with a far weaker legal position.

Keep records of everything. Every written notice received, every inspection performed, every repair completed. These records are the difference between a manageable dispute and expensive litigation.

Dispute Resolution: Mediation and Arbitration

Most builder warranty programs use one of two mechanisms to resolve disputes short of court:

- Mediation — non-binding, facilitated negotiation between the parties

- Arbitration — binding decision by a neutral third party

Many builder warranties require arbitration over litigation. For VA- or FHA-financed homes, the FTC notes that homeowners making claims against a third-party warranty company may choose between arbitration and court.

That choice carries real financial weight. AAA's Home Construction Industry fee schedule shows that disputes between $300,000 and $1,000,000 carry a builder filing fee of $3,250 — and that's just the administrative fee, before arbitrator compensation. Contractors who manage claims thoroughly upfront spend a fraction of what disputed cases cost to resolve.

How Contractors Can Turn Warranty Obligations Into a Profit Center

Most contractors treat warranty coverage as a cost to be minimized. That framing leaves real money on the table.

The Problem With Third-Party Warranty Providers

When contractors pass warranty obligations to a third-party warranty company, they pay a premium to transfer the risk. That premium (collected to fund potential claims) doesn't disappear. It becomes the third-party provider's underwriting profit. The contractor retains the customer relationship and reputational exposure; the warranty company keeps the money.

If third-party warranty providers weren't profitable, they wouldn't exist. The premiums collected consistently exceed claims paid. Contractors are funding someone else's profit margin on every job.

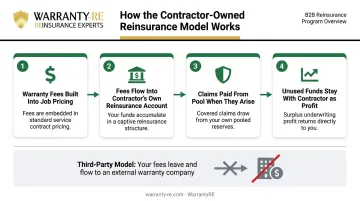

Contractor-Owned Reinsurance: The Alternative

WarrantyRE, which has been helping contractors and dealers establish their own reinsurance companies since 1994, offers a different structure. Rather than paying a third party to hold warranty risk, contractors form their own reinsurance company (backed by A-rated insurers) and keep the underwriting profit themselves.

Here's how the mechanics work:

- Warranty fees are built into job pricing — customers are already paying for coverage

- Fees flow into the contractor's own reinsurance account, held at a U.S. Trust Company

- Claims are paid from the pool when they arise

- Unused funds remain with the contractor as underwriting profit

WarrantyRE handles setup, claims adjudication, compliance, legal filings, performance reporting, and staff training. Contractors capture the profit without taking on the administrative work.

What Changes (and What Doesn't)

From the homeowner's perspective, nothing changes. They receive the same warranty coverage, backed by the same A-rated insurance carrier support. The difference is entirely structural : the underwriting profit flows to the contractor rather than a third party.

Key financial benefits of the contractor-owned model:

- Captures 100% of underwriting profit that previously went to a third-party provider

- Creates tax-advantaged structures through reinsurance contributions, reducing annual tax burden

- Accumulated reserves can be invested in government bonds or, once they exceed 125% of unearned premiums, more aggressively at the owner's direction

- Funds warranty work from the customer-funded pool rather than the contractor's operating cash

HVAC, roofing, plumbing, and electrical contractors are all currently using this structure. On a $12,000 HVAC system replacement, for example, a 2-year labor warranty fee built into the job price flows directly into the contractor's reinsurance account. Claims come out of that pool. Whatever isn't claimed stays with the contractor.

For contractors running significant installation volume, that's a meaningful income stream — built entirely from work they were already doing.

Frequently Asked Questions

Does new construction come with a warranty?

Yes. Most new construction carries both a written builder's warranty and implied warranty protections imposed by state law. Coverage typically spans workmanship (1 year), major systems (2 years), and structural defects (up to 10 years), though the exact terms depend on the builder's program and applicable state statutes.

What does the 2-year warranty on new construction cover?

The 2-year tier generally covers the home's major mechanical systems — HVAC, plumbing, and electrical — for defects resulting from improper installation. It does not cover normal wear and tear or component failures already addressed by equipment manufacturer warranties.

Does the VA require a 10-year warranty on new construction?

VA guidance requires new construction to be covered by either a one-year VA builder's warranty (VA Form 26-1859) or a 10-year insurance-backed protection plan acceptable to HUD. FHA dropped its 10-year plan requirement in 2019, now requiring only a one-year Warranty of Completion of Construction.

Is a home warranty worth it for new construction?

For new construction, the builder's warranty is the primary protection and is legally required in many states. A separate home warranty (service contract) is an optional purchase designed to extend coverage after builder warranties expire, not to duplicate them.

What is the difference between a builder's warranty and a home warranty?

A builder's warranty is tied to the construction of the home and covers workmanship, systems, and structural defects. A home warranty (service contract) is separately purchased, covers appliances and mechanical systems, and is designed to pick up where builder coverage leaves off.