Introduction

HVAC contractors, roofers, plumbers, and electricians routinely include labor warranties in their proposals — often without a clear financial model behind it. Who's actually profiting from those warranty premiums? If you're handing risk to a third-party administrator, absorbing callback costs out of pocket, or burying warranty fees in your pricing, the answer probably isn't you.

As warranty programs become table stakes for winning bids, contractors are asking whether there's a smarter structure — one that lets them protect their work and retain the financial upside. The home services market is projected to reach $802 billion by 2030, with HVAC, roofing, plumbing, and electrical work representing some of the largest segments. Every one of those jobs includes a warranty — and every one represents a profit opportunity contractors are often leaving on the table.

That profit opportunity comes down to structure. The choice between captive insurance and contractor reinsurance directly affects margins, claims control, and long-term financial stability — and most contractors don't realize they have options beyond buying third-party coverage. Both models put more control in your hands. Which one fits your business is what matters.

TL;DR

- Captive insurance means forming a licensed insurance subsidiary you own — with high capital requirements, complex setup, and heavy regulatory oversight

- The admin obligor reinsurance model lets you own a reinsurance entity backed by A-rated insurers, with warranty premiums funding your company instead of a third party

- Captive structures fit large, multi-state operations with diversified liability risks and substantial capital reserves

- For most HVAC, roofing, plumbing, and electrical contractors, the admin obligor model offers lower barriers, expert support, and direct profit recapture

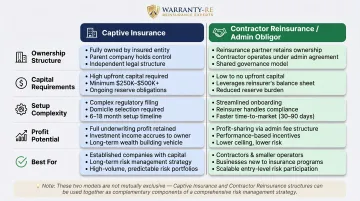

Captive Insurance vs. Reinsurance for Contractors: Quick Comparison

| Dimension | Captive Insurance | Contractor Reinsurance (Admin Obligor) |

|---|---|---|

| Ownership Structure | You form and own a fully licensed insurance company that underwrites risk directly | You own a reinsurance entity; risk is shared with an A-rated fronting insurer who provides the licensed insurance paper |

| Capital Requirements | $250,000+ initial capitalization (varies by domicile); substantial startup reserves required | Lower entry barrier; capitalized through warranty premiums built into customer job pricing |

| Setup Complexity | High: actuarial studies, domicile selection, state filings, ongoing regulatory oversight | Simplified: administrator handles company formation, legal filings, compliance, and training |

| Profit Potential | Full control over underwriting profits and investment income; can underwrite multiple risk lines | Capture 100% of warranty underwriting profits; investment income on reserves; focused on service warranties |

| Best For | Large contractors or franchise groups with $500K+ annual premium volume and in-house risk management teams | HVAC, roofing, plumbing, and electrical contractors replacing third-party warranty providers; want recurring revenue from installs without operational complexity |

Note: These structures are not mutually exclusive: captives often purchase reinsurance to manage large or volatile losses. For most home service contractors, the reinsurance model offers a faster, lower-capital path to capturing warranty profits.

What Is Captive Insurance?

Captive insurance is a business-owned, licensed insurance company formed specifically to underwrite the parent company's own risks. Instead of paying premiums to a commercial carrier, the business creates a wholly owned subsidiary that functions as both the insurer and the insured.

The National Association of Insurance Commissioners (NAIC) defines a captive as "a wholly owned subsidiary created to provide insurance to its non-insurance parent company." That structure gives the business direct control over policy design, underwriting decisions, and claims management.

Types of Captives

Two main types matter for contractors:

- Single-parent (pure) captives — owned by one company exclusively

- Group captives — shared among multiple businesses, often in the same industry

Micro-captives (those with annual written premiums under $2.8 million) can elect to be taxed only on investment income under IRC Section 831(b). However, final IRS regulations issued in January 2025 now classify certain micro-captive arrangements as "listed transactions" or "transactions of interest," requiring strict disclosure and triggering heightened IRS scrutiny.

Practical Barriers for Most Contractors

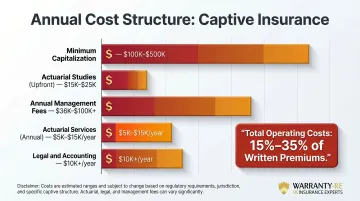

Those tax benefits come with a steep price of entry. Forming a captive typically requires:

- Minimum capitalization ranging from $100,000 to $500,000, depending on domicile

- Selection of a domicile jurisdiction (Vermont, Delaware, Utah, offshore)

- Actuarial studies and feasibility analysis: $15,000–$25,000 upfront

- Ongoing regulatory filings and compliance oversight

- Annual management fees of $36,000–$100,000+, plus actuarial services ($5,000–$15,000) and legal/accounting ($10,000+)

- Total annual operating costs estimated at 15%–35% of written premiums

Vermont, the largest US captive domicile, hosts 639 active captives — primarily Fortune 500 companies and large enterprises with dedicated risk management teams. For most small-to-mid-size contractors, those overhead costs consume any underwriting profit before it reaches the owner's pocket — which is why reinsurance structures built specifically for contractors offer a more accessible path.

What Is Reinsurance for Home Service Contractors?

Reinsurance is a risk-sharing structure where a contractor's own reinsurance entity partners with a licensed fronting insurer. The contractor isn't buying retail insurance — they're participating in the insurance market as an insurer themselves, capturing the underwriting profits traditionally kept by third-party warranty providers.

The Admin Obligor Model

In the admin obligor model:

- The contractor forms a reinsurance company

- Customer warranty premiums flow into that entity

- Claims are paid from the contractor's reinsurance reserves

- Underwriting profits accumulate for the contractor, not a third party

The fronting insurer (A-rated) provides the licensed insurance paper, giving the program legal and regulatory compliance along with consumer protection. If the contractor's reinsurance company cannot meet obligations, the fronting insurer ultimately bears claim liability.

How Customer-Funded Premiums Change the Economics

Every service warranty sold — whether for an HVAC install, a new roof, or other labor work — generates premium dollars. In a traditional third-party model, those premiums enrich the warranty administrator. In a reinsurance structure, they fund the contractor's own entity.

Example: You close a $12,000 HVAC system replacement with a 2-year labor warranty. The warranty fee is built into the job price. That fee goes directly into your reinsurance account. When warranty calls come in, they're covered from this pool. Unused funds remain with you as profit.

According to ACCA industry data, a single HVAC lead can cost $400, making customer retention a direct financial priority. When warranties keep customers loyal, the reinsurance structure ensures those warranty fees stay in your business — not a third party's pocket.

Operational Benefits for Home Service Contractors

- Retain 100% of underwriting profits instead of sending them to a third-party administrator

- Build balance sheet equity as every install generates premium income

- Adjudicate claims fairly and reduce unnecessary callbacks on your terms

- Hold reserves in a tax-advantaged insurance entity for structured tax planning

WarrantyRE's Admin Obligor Reinsurance Program

WarrantyRE handles the full setup and ongoing administration for contractors entering this structure. The company handles company formation, legal filings, staff training, claims adjudication, compliance, and financial reporting — so contractors can access these benefits without needing insurance expertise in-house.

Captive Insurance vs. Reinsurance: Which Is the Better Fit for Home Service Contractors?

Key Decision Factors

Consider:

- Business revenue and scale — are you writing $500K+ in annual premiums?

- Type of risk — warranty/service risk vs. broader liability exposure

- Available startup capital — can you fund $250K+ in initial reserves?

- Tolerance for administrative complexity — do you have in-house risk management staff?

When a Captive Structure Makes Sense

Captives work best for:

- Larger contractors or franchise groups with revenue across multiple states

- Businesses that want to underwrite multiple lines of coverage (GL, workers' comp, equipment, warranties)

- Contractors who already have risk management infrastructure and want maximum customization

When the Admin Obligor Reinsurance Model Is the Clear Fit

Reinsurance is ideal for:

- Contractors replacing a third-party warranty provider

- Businesses whose primary risk exposure ties to service warranties on installed equipment

- Contractors seeking professionally managed programs without forming a full insurance company

- Those wanting to generate recurring revenue from their existing customer base

When Captives and Reinsurance Work Together

Captives and reinsurance aren't always competing alternatives. Many captive structures purchase reinsurance behind them to manage large or volatile losses. But for a roofing, HVAC, plumbing, or electrical contractor entering this space, starting with an admin obligor reinsurance program delivers immediate profit recapture and claims control without the upfront capital a captive requires.

Situational Summary

- Reinsurance: Best fit if you want to replace third-party warranties and build recurring revenue from installs — without heavy capital or administrative overhead.

- Captive: Better suited if you're large enough to justify forming a full insurance entity and want to underwrite multiple coverage types beyond warranty claims.

How a Home Service Contractor Reinsurance Program Works in Practice

Step 1 — Formation

A contractor works with a reinsurance program administrator to legally form their own reinsurance entity. This includes business structure setup, state filings, tax return preparation, and onboarding of administrative staff. The contractor does not need insurance licensing.

Step 2 — Premium Flow

Warranty premiums collected from customers at the point of installation or service agreement are directed into the contractor's reinsurance company rather than to a third-party warranty administrator. Every sale builds the contractor's own balance sheet.

Step 3 — Claims Management

The administrator adjudicates claims while the contractor's reinsurance entity funds covered payouts. This reduces frivolous callbacks and ensures claims data informs future pricing and coverage decisions.

Step 4 — Profit Accumulation and Investment

Underwriting profits (premiums minus claims and admin costs) accumulate within the contractor's reinsurance company. They can be invested for additional ROI, used for tax planning, or distributed, creating a financial asset that grows alongside the service business.

WarrantyRE handles every element of this process: company setup, ongoing compliance, claims administration, and performance reporting. HVAC, roofing, plumbing, and electrical contractors capture the profits their warranty programs generate without adding operational complexity.

Ready to explore whether reinsurance is right for your business? Reach out to WarrantyRE at (804) 824-9533 or visit warranty-re.com to learn how to get started.

Frequently Asked Questions

What is the difference between captive insurance and reinsurance?

Captive insurance is a business-owned licensed insurance company that directly underwrites risk. Reinsurance transfers risk from a primary (fronting) insurer to another entity — often the contractor's own reinsurance company. The two structures frequently work together rather than against each other, since captives regularly purchase reinsurance to manage large losses.

Do captives buy reinsurance?

Yes. Captives frequently purchase reinsurance from third-party reinsurers to manage large or catastrophic losses that exceed their own balance sheet capacity, stabilize financial results, and comply with regulatory capital requirements. The two structures are often complementary rather than competing.

What are the main types of reinsurance?

The two primary types are facultative reinsurance (negotiated risk by risk) and treaty reinsurance (automatic coverage for a defined class of business), with proportional and excess-of-loss as common treaty sub-types. Home service contractor programs typically use treaty-style arrangements.

What are the two major types of captive insurance companies?

Single-parent captives are owned exclusively by one company; group or association captives involve multiple unrelated businesses pooling resources in a shared structure. Micro-captives (under the 831(b) election) are a smaller variation but have faced significant IRS scrutiny in recent years.

What is a captive contractor?

"Captive contractor" is not an insurance term — it typically refers to a contractor exclusively tied to one client or employer rather than operating independently. In the insurance context, home service contractors interested in risk ownership are more likely to explore the admin obligor reinsurance model or a captive insurance structure.