This article breaks down how warranty administration works for contractors, which providers merit evaluation, how to assess them properly, and what a growing number of HVAC, roofing, plumbing, and electrical contractors are doing instead to keep more revenue in-house.

TL;DR

- Third-party warranty administrators handle claims, compliance, and customer service — removing callbacks from contractors' plates

- Top administrators offer transparent fees and A-rated insurer backing, though most programs target home builders rather than trade contractors

- Key selection criteria: claims turnaround time, AM Best A- or higher solvency rating, fee transparency, and customer relationship impact

- Contractor-owned reinsurance is a growing alternative that lets contractors capture underwriting profits instead of paying them out

What Is a Third-Party Warranty Administrator for Contractors?

A third-party warranty administrator is a company that sits between the contractor and the homeowner to process warranty claims, approve or deny coverage decisions, handle documentation, and manage compliance—so contractors don't have to operate a warranty department in-house.

Contractor warranties differ fundamentally from manufacturer warranties. Manufacturer warranties cover defects in equipment (furnaces, compressors, shingles). Contractor warranties cover labor and workmanship on installed systems—HVAC installations, roof replacements, plumbing repiping, electrical panel upgrades. The administrator determines what qualifies as a covered claim versus a standard service call.

Critical distinction: A warranty administrator manages the program and processes claims. A warranty obligor (also called the provider) is the financially responsible entity that pays claims. According to the NAIC Service Contracts Model Act, these can be the same company or separate entities. Many contractors confuse the two, and the distinction matters when evaluating risk and profitability.

The difference carries real consequences:

- If the administrator goes out of business but isn't the obligor, your warranty program may continue

- If the obligor fails and lacks proper insurance backing, you're exposed to unpaid claims

The NAIC Model Act requires warranty obligors to maintain one of three financial safeguards:

- Reimbursement insurance from an authorized insurer

- Funded reserves of at least 40% of gross consideration received (less claims paid) plus a 5% security deposit

- Net worth of at least $100 million

These requirements exist because warranty programs collect money upfront against future obligations—which is why vetting your obligor's financial backing is as important as evaluating the administrator's claims process.

Top Third-Party Warranty Administrators for Contractors

The following administrators were evaluated based on contractor-relevant criteria: coverage scope for trade work, claims handling infrastructure, fee transparency, and A-rated insurer backing—not just consumer brand recognition.

2-10 Home Buyers Warranty (2-10 HBW)

Founded in 1980 and now part of the Frontdoor brand, 2-10 HBW has provided warranties and service contracts for over 6 million new and pre-owned homes. The company is the largest administrator of builder warranties in the US, headquartered in Memphis, TN.

Who it's built for: 2-10 HBW is structured specifically for home builders, not standalone trade contractors. Its programs cover workmanship, distribution systems (electrical, plumbing, mechanical), and structural defects—sold as part of new home construction packages.

The NewHome Care program serves as the first point of contact for homeowner warranty questions, eliminating direct builder calls. Builders can select shared-risk deductibles ($10,000, $50,000, or $100,000 per occurrence) to lower their rates.

| Coverage Scope | Claims Process | Fee Structure for Contractors |

|---|---|---|

| Workmanship and distribution systems (electrical, plumbing, mechanical) for 1-2 years; structural coverage for 10 years; programs designed for home builders, not standalone HVAC, plumbing, or electrical contractors | 2-10 HBW receives and processes reported defects, arranges and pays for inspections, oversees dispute resolution, and manages homeowner communication; NewHome Care eliminates direct homeowner-builder contact | Pricing is not publicly listed; builders must request quotes; homes up to 3 years old can be enrolled (subject to inspection); shared-risk deductibles available to lower rates |

For trade contractors: No dedicated programs exist for standalone contractors performing service work, installations, or renovations outside of new home construction.

Residential Warranty Corporation (RWC)

Founded in 1981 and headquartered in Harrisburg, PA, RWC has administered warranties on over 4 million homes across 45 years. The company offers over 75 different warranty options serving builders, remodelers, and manufacturers.

The standout for remodelers: RWC is the only evaluated administrator with an explicit Remodelers Warranty designed for professional contractors doing renovation projects. The company's insurer has held an AM Best A- (Excellent) rating since 2001 and maintains over $130 million in surplus equity.

| Coverage Scope | Claims Process | Fee Structure for Contractors |

|---|---|---|

| Traditional 1-2-10 new home warranty; customized state warranties; Remodelers Warranty for professional contractors performing renovation work; builder liability limited to 2 years in most programs | Multi-step resolution process: written notice → mediation (free, informal) → conciliation (formal review) → arbitration (binding); warranties automatically transfer to subsequent buyers at no cost | Enrollment fees and per-home costs are not publicly disclosed; contractors must request a warranty quote directly |

Key advantage: The Remodelers Warranty explicitly targets trade contractors, making RWC the most relevant traditional administrator for renovation-focused HVAC, plumbing, electrical, and roofing contractors.

Warrantech (Amynta Group)

Warrantech is a subsidiary of The Amynta Group and was historically associated with AmTrust Financial Services. The company was acquired by H.I.G. Capital in 2007 at $0.75 per share, with AmTrust completing full acquisition in 2010.

Critical finding—Warrantech currently focuses exclusively on automotive, recreational, and powersports industries. Its programs serve vehicle service contracts through franchised and independent automobile dealers, leasing companies, and financial institutions.

Coverage spans automobiles, light trucks, powersports, watercraft, recreational vehicles, and mobility vans. No home service contractor programs were identified. For HVAC, plumbing, electrical, or roofing contractors, Warrantech is not a viable option.

Quality Builders Warranty (QBW)

Founded in 1985 and headquartered in Camp Hill, PA, QBW is backed by Liberty Mutual and markets itself as "the only 10-year home warranty program backed by a national insurance carrier of this size."

Builder tools: QBW provides QBW Direct (online tool for managing closings and inventory), Service Online Solution (SOS) for homeowner warranty requests, and QBW Messenger for integrated communication. Builder liability is limited to the first 2 years, except in Indiana and Virginia.

| Coverage Scope | Claims Process | Fee Structure for Contractors |

|---|---|---|

| Year 1: builder responsible for defects in workmanship and materials + major structural defects; Year 2: builder responsible for wiring, piping, ductwork defects + major structural defects; Years 3-10: QBW/Liberty Mutual covers major structural defects | Homeowner submits claims through builder's SOS platform; builder manages Year 1-2 claims; QBW/Liberty Mutual assumes Years 3-10; warranties automatically transfer to subsequent buyers | Specific enrollment fees not publicly disclosed; builders must request quotes; membership and partnership structured between QBW and the builder |

Bottom line: Programs are marketed exclusively to home builders for new construction. No standalone trade contractor enrollment was identified.

Fortegra Financial

Founded in 1978 (originally as Life of the South, rebranded to Fortegra in 2008), Fortegra is headquartered in Jacksonville, FL. The company was acquired by Tiptree Holdings in 2014 for $218 million, with DB Insurance announcing a follow-on acquisition in September 2025.

Fortegra reported $1.2 billion in premium growth revenue and holds an AM Best A- (Excellent) rating, affirmed April 2025.

The model: Fortegra offers white-label warranty solutions that let partners sell branded protection products under their own name. Its B2B approach includes tailored portfolios, embedded insurance, disciplined underwriting, and integrated support teams.

| Coverage Scope | Claims Process | Fee Structure for Contractors |

|---|---|---|

| Warranty solutions including protection plans, service contracts, home protection plans, and commercial coverage; partner categories include managing general agents, agents/brokers, financial institutions, auto dealers, medical devices/pharma, manufacturers, and administrators—no specific programs for HVAC, plumbing, electrical, or roofing trade contractors identified | Claims handling infrastructure integrated into white-label partner programs; specific contractor claims process not disclosed | Program costs and customization options not publicly disclosed; white-label partnerships require direct negotiation |

Worth noting: No trade contractor-specific programs appear on Fortegra's website. The company serves manufacturers, dealers, and administrators—not specialty trade contractors directly.

How We Chose the Best Third-Party Warranty Administrators for Contractors

The biggest mistake contractors make is choosing a warranty administrator based on brand name alone, without examining how claims decisions are made, who bears financial risk, and what happens to customer relationships when a claim is denied.

Our evaluation framework focused on:

- Coverage scope for trade work — Does the administrator cover HVAC, roofing, plumbing, and electrical labor warranties, or only new home construction?

- Claims turnaround benchmarks — How quickly are claims processed and resolved?

- Contractor fee transparency — Are costs disclosed publicly or hidden behind quote requests?

- Administrator vs. obligor structure — Is the administrator also the financially responsible obligor, or is risk outsourced to a third party?

- Ease of enrollment — Can a standalone contractor join, or is the program restricted to home builders?

- Financial solvency — Is the program backed by an A-rated insurance carrier?

Solvency deserves its own step in your due diligence. Verify that any administrator's program is backed by an insurer rated A- (Excellent) or higher by AM Best — an administrator that cannot pay claims exposes you to reputational and legal risk. According to ACCA's guidance for HVAC contractors, verifying "whether an A-rated insurance underwriter is backing the program" is the single most important due diligence step.

Among the administrators we evaluated, here's how each stacks up on that test:

- RWC's insurer holds AM Best A- (Excellent) since 2001

- QBW is backed by Liberty Mutual (a large, highly rated carrier)

- Fortegra holds AM Best A- (Excellent), affirmed April 2025

Most traditional warranty administrators focus on home builders and new construction — not standalone trade contractors. Only RWC's Remodelers Warranty explicitly targets professional contractors.

For HVAC, plumbing, electrical, and roofing contractors seeking dedicated labor warranty administration, specialist providers such as Trinity Warranty or contractor-owned reinsurance structures may be more appropriate than builder-focused administrators.

Why Some Contractors Are Moving Beyond Third-Party Administration

The core limitation of third-party administration is simple: the administrator keeps the underwriting profit—the difference between premiums collected and claims paid. Contractors fund this revenue stream but never see it, even when their claim rates are low because of quality workmanship.

Warranty Week reports that Frontdoor Inc. achieved an 18% profit margin in Q3 2024. While this reflects the consumer warranty segment rather than contractor labor warranties specifically, the structural economics are the same: a meaningful share of every premium dollar stays with the administrator, not the contractor doing the work.

Rather than paying a third party to administer warranty obligations, contractors can establish their own administrator-obligor reinsurance company—backed by A-rated insurers—that processes claims internally and retains the underwriting profit.

Contractors typically choose between two ownership structures:

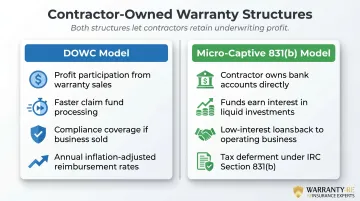

Dealer Owned Warranty Company (DOWC) Model

Programs like NAHG/ServiceGuard enable HVAC contractors and distributors to own their warranty company and participate in back-end profits from warranty sales. Key features include:

- Profit participation from warranty sales revenue

- Faster claim fund processing

- Compliance coverage if the business is sold

- Reimbursement rates reviewed annually for inflation

Micro-Captive Insurance (831(b)) Model

Programs such as Project Warranty set up a micro-captive insurance entity entirely owned by the contractor. Under this structure:

- Contractor owns the bank accounts directly (no escrow)

- Funds earn interest in high-liquidity investments

- Low-interest loans from the captive back to the operating business are available

- Tax deferment advantages apply under IRC Section 831(b)

The shift is structural, not cosmetic. With a reinsurance model, contractors turn installs into recurring revenue, cut the cost of service callbacks, retain full control over the customer claims experience, and capture profits that previously went to a third party.

For contractors ready to make that shift, WarrantyRE has helped HVAC, roofing, plumbing, and electrical businesses establish their own administrator-obligor reinsurance companies since 1994. Full-service administration covers claims adjudication, compliance, training, financial management, and legal filings—while the contractor keeps 100% of underwriting profits in a tax-advantaged structure backed by A-rated insurers.

Conclusion

The best third-party warranty administrator for your contracting business is one that:

- Processes claims fairly and consistently

- Protects your customer relationships

- Carries AM Best A- or higher financial ratings

- Is transparent about what contractors pay versus what they keep

Those standards matter — and they're a reasonable bar to set. Yet as claim volume grows and program maturity increases, the economics of keeping underwriting profit in-house become harder to ignore. Unused warranty reserves paid out to a third-party administrator represent real margin leaving your business every year.

If you're a contractor curious about whether a reinsurance-based warranty program makes sense for your business, contact us to explore how our reinsurance model could replace or supplement your current third-party arrangement.

Frequently Asked Questions

What is the best third-party extended warranty administrator for contractors?

There is no single "best" option—the right administrator depends on your trade, claim volume, and whether you prioritize cost, claims speed, or customer control. Evaluating financial solvency (AM Best A- or higher), obligor backing, and fee transparency are the most important steps. RWC is the only traditional administrator with a Remodelers Warranty targeting trade contractors.

What does a third-party warranty administrator do for a contractor?

A warranty administrator manages the operational side of a contractor's warranty program: receiving and adjudicating claims, handling customer communications, maintaining compliance documentation, and coordinating repairs or reimbursements. This removes the day-to-day burden so contractors can focus on billable work.

How much does it cost a contractor to use a third-party warranty administrator?

Costs vary by program structure—some administrators charge per-job enrollment fees, others take a percentage of the warranty premium, and some charge flat annual program fees. None of the five administrators publish pricing — all require a direct quote. Hidden fees are common, so request a detailed breakdown before committing.

What is the difference between a warranty administrator and a warranty obligor?

A warranty administrator manages the process: claims, paperwork, customer contact. The warranty obligor is the entity legally and financially responsible for paying claims. These can be the same company or separate entities. Contractors should confirm which entity is backing their program and verify the obligor's financial strength through AM Best ratings or NAIC filings.

Do contractors need a third-party warranty administrator, or can they run their own program?

Contractors with sufficient volume can structure their own administrator-obligor reinsurance company, controlling claims decisions and retaining underwriting profit instead of paying it to a third party. WarrantyRE specializes in helping contractors build these structures, as do NAHG/ServiceGuard and Project Warranty.

What should contractors look for when evaluating a warranty administrator?

Key vetting criteria include:

- Financial backing by an AM Best A-rated insurer

- Transparent fee structure with no hidden costs

- Clear claims adjudication timelines and criteria

- Licensing in all states where you operate

- Obligor compliance with NAIC Service Contracts Model Act requirements