The right tax strategies, applied year-round rather than scrambled together at filing time, can meaningfully reduce your tax burden while improving cash flow and long-term profitability. This isn't about aggressive loopholes or questionable deductions. It's about structuring your business correctly, timing revenue recognition strategically, and making smart investment decisions throughout the year that minimize taxable income legally.

TL;DR

- Electing S Corp status eliminates up to 15.3% self-employment tax on distributions

- Section 179 lets you deduct up to $1,250,000 in equipment costs immediately in 2025

- Most roofing contractors underclaim deductions for subcontractor costs, safety gear, and vehicle expenses

- The completed contract method legally defers income on projects spanning tax years

- QBI deduction cuts taxable income by 20% for qualifying profitable contractors

Why Roofing Contractors Need a Year-Round Tax Strategy

Roofing revenue is intensely seasonal. Most contractors generate 60-70% of annual revenue during Q2 and Q3 storm season, while Q1 often brings razor-thin cash flow. Consumer search data shows roof repair searches peak at +24% in September, reflecting this demand concentration.

This seasonal volatility makes end-of-year tax scrambling particularly costly. Without proactive planning, surprise tax bills land in January — your tightest cash month — draining operating capital you need for payroll, insurance renewals, and spring preparation.

The National Small Business Association's 2024 Taxation Survey makes the stakes clear:

- 90% of small business owners say federal taxes affect day-to-day operations

- 1 in 3 report a "significant" operational impact

- 20+ hours spent annually on taxes — even among those who hire professional help

Filing correctly is only part of the equation. Real tax savings come from structuring your business, timing revenue recognition, and making equipment investments strategically throughout the year — not in a December scramble.

Choose the Right Business Entity Structure

Many roofing contractors operate as sole proprietors or single-member LLCs, inadvertently paying 15.3% self-employment tax on every dollar of net profit. Choosing the right structure is one of the highest-leverage tax decisions a profitable roofer can make.

Sole Proprietor and Single-Member LLC

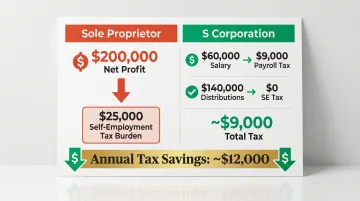

Pass-through taxation is straightforward but expensive for profitable roofers. All net profit flows to your personal return and faces the full 15.3% self-employment tax: 12.4% Social Security (on earnings up to $176,100 in 2025) plus 2.9% Medicare (no cap). For a contractor netting $200,000, that's over $25,000 in self-employment tax before income tax even starts.

S Corporation Election

The S Corp salary-plus-distribution strategy cuts that bill substantially. You pay yourself a "reasonable salary" subject to payroll taxes, then take remaining profit as distributions — which avoid the 15.3% self-employment tax entirely.

Example: A roofing contractor nets $200,000 annually.

- As sole proprietor: Pays ~$25,000 in self-employment tax

- As S Corp: Pays $60,000 reasonable salary (fully subject to payroll tax = ~$9,000) and takes $140,000 as distributions (zero self-employment tax). Tax savings: approximately $12,000 annually.

The IRS scrutinizes unreasonably low salaries. Case law including Watson v. United States shows the IRS will reclassify distributions as wages if salary doesn't reflect the owner's actual duties, time commitment, and comparable industry compensation.

C Corporation

C Corps face double taxation: a 21% federal corporate tax, then personal tax on dividends. That structure makes them uncommon for small roofing businesses. Larger operations may benefit from broader fringe benefit deductions and the ability to retain earnings at the flat 21% rate — but those advantages only outweigh the double-taxation drag at significant revenue levels.

Revisit your entity structure as revenue grows. What works at $500,000 may cost you tens of thousands at $2 million.

Maximize Equipment, Vehicle, and Job-Specific Deductions

Roofing is capital-intensive, giving you more deduction opportunities than most trades — if you know which apply and maintain records to support them.

Section 179 and Bonus Depreciation

Section 179 allows immediate expensing of qualifying equipment up to $2,500,000 in 2025 (phaseout begins at $4,000,000) rather than depreciating assets over 5-7 years. Qualifying purchases include trucks, trailers, nail guns, scaffolding, ladders, software, and tools.

Both strategies can be used together or separately. Bonus depreciation is now permanently set at 100% following the One Big Beautiful Bill Act signed in July 2025, reversing the TCJA phase-down that would have reduced it to zero by 2027. You can write off the full cost of qualifying equipment in the year you place it in service — with no sunset date going forward.

Strategy: If you're buying a $70,000 work truck in 2025, Section 179 or 100% bonus depreciation lets you deduct the entire amount this year instead of spreading it over five years. For a contractor in the 32% bracket, that's $22,400 in immediate tax savings.

Vehicle Deductions

The IRS offers two methods:

- Standard mileage rate: 70 cents per mile for 2025 business use

- Actual expense method: Track real costs (fuel, insurance, repairs, depreciation)

For heavy-use work trucks common in roofing, actual expense typically yields larger deductions. Vehicles over 6,000 lbs GVWR qualify for enhanced Section 179 treatment beyond standard passenger limits (SUVs are capped at $31,300).

Audit Risk: Maintain detailed mileage logs. Poor documentation is the top reason contractors lose deductions under audit.

Job-Specific and Overhead Deductions

Commonly missed deductions include:

- Subcontractor labor (with proper 1099 filing)

- Roofing materials and supplies consumed on jobs

- Safety equipment (harnesses, helmets, boots)

- Marketing and advertising

- Professional fees (accounting, legal)

- Software subscriptions (estimating, CRM, project management)

- Home office expenses if you perform administrative work from home

Deductions must be ordinary, necessary, and documented. Keep receipts, invoices, and contemporaneous records for every expense.

Advanced Tax Reduction Strategies: Accounting Methods, QBI, and Retirement

Accounting Method Elections

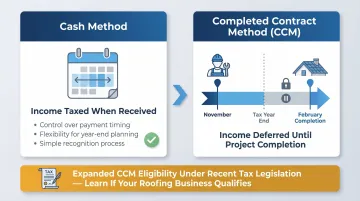

Roofing contractors under the $31 million average annual gross receipts threshold can elect the cash method of accounting, meaning income is taxed only when received (not when billed). This is valuable for managing retainage and year-end revenue timing.

A separate election — the completed contract method (CCM) — lets eligible small contractors recognize income and expenses only when projects finish. Recent legislative changes expanded CCM eligibility from home construction to all residential construction and extended qualifying contract duration from 2 to 3 years. If you start a large project in November that completes in February, CCM defers all that income to the following tax year.

The Qualified Business Income (QBI) Deduction

Section 199A allows eligible pass-through owners to deduct up to 20% of qualified business income, reducing taxable income without any cash outlay. For 2025, the deduction begins phasing out at $197,300 (single) or $394,600 (married filing jointly).

Above these thresholds, the deduction is limited by W-2 wages paid or the value of qualified property. This creates a balancing act worth understanding:

- Higher W-2 wages paid to yourself or employees increases your QBI deduction capacity at upper income levels

- Excessive owner salary, however, reduces QBI itself — which shrinks the 20% deduction

- The takeaway: compensation strategy and QBI optimization must be planned together, not in isolation

Retirement Account Contributions

The three most relevant retirement vehicles for roofing contractors:

- SEP IRA: Contribute up to 25% of net self-employment earnings, maximum $70,000 in 2025. Simple to set up and maintain.

- Solo 401(k): Higher contribution limits by combining employee deferrals ($23,500) and employer contributions (up to $70,000 total; $81,250 for ages 60-63). Best for self-employed contractors with no W-2 employees.

- SIMPLE IRA: Employee deferrals up to $16,500 ($21,750 ages 60-63), plus employer match. Better for contractors with small staff.

Each dollar contributed is a dollar off your taxable income. A contractor in the 32% bracket who puts $50,000 into a SEP IRA saves $16,000 in federal tax — while building long-term wealth at the same time.

Turn Your Warranty Program into a Tax Advantage

Most roofing contractors handle warranty obligations in two ways: absorb claim costs out-of-pocket (unpredictable liability) or pay third-party warranty administrators (money leaves permanently). Neither approach provides tax planning benefits.

Contractor-owned reinsurance offers a third option. Roofing businesses can establish their own administrator obligor reinsurance company, where warranty premiums customers pay flow into an entity the contractor owns — not a third-party provider.

Here's how it works: On a $15,000 roof replacement with a 5- or 10-year labor warranty, a warranty fee is built into the contract price. Instead of that fee disappearing to an external warranty company, it flows into your reinsurance account, a tax-advantaged structure you control completely. When claims arise, they're paid from this pool. Unused funds remain yours.

This structure operates under IRS Section 831(b) provisions, which allow qualifying small insurance companies with less than $2.85 million in annual premiums (2025 limit) to be taxed only on investment income, with underwriting profits exempt from federal income tax. Key conditions that make this structure work:

- Premiums must stay under the $2.85M annual threshold

- The company must qualify as a small insurance company under IRS rules

- Underwriting profits accumulate tax-exempt, building retained earnings you own

- Contributions provide tax advantages beyond any standard deduction

Important: This strategy requires proper legal structuring, ongoing compliance, and professional administration. WarrantyRE has helped contractors in roofing, HVAC, plumbing, and other trades set up and manage these programs since 1994. The company handles all legal forms, tax filings, claims administration, and compliance management, allowing contractors to focus on operations while capturing underwriting profits third-party providers would otherwise keep.

For profitable roofing businesses ready to stop subsidizing third-party warranty providers, this structure converts an overlooked cost center into a controlled, tax-advantaged asset.

Conclusion

The roofing contractors who pay the least in taxes aren't doing anything exotic — they're combining the right entity structure, aggressive depreciation, strategic revenue timing, and long-term vehicles like retirement accounts and reinsurance programs. Each layer builds on the last. Together, they produce compounding savings that grow with the business.

Tax planning isn't a once-a-year filing exercise. It's a year-round discipline that preserves cash flow, funds growth, and protects profitability in an industry where margins are tight and cash flow swings with the season.

Work with a tax professional who understands the construction industry — someone who can implement these strategies correctly, not just file a return. If reinsurance-based profit and tax structures are on your radar, WarrantyRE works directly with roofing contractors to build and manage those programs. Reach them at (804) 824-9533.

Frequently Asked Questions

What is the most overlooked tax deduction for roofing contractors?

Vehicle and mileage deductions, subcontractor costs (with proper 1099 filing), and job-specific safety equipment are most commonly missed. Without systematic recordkeeping — detailed mileage logs, receipts for safety gear, and organized subcontractor documentation — these legitimate deductions simply go unclaimed year after year.

What are the 5 pillars of tax planning?

The five core pillars of tax planning are:

- Income shifting — moving income to lower-tax entities or family members

- Deduction timing — accelerating or deferring deductions strategically

- Tax deferral — delaying income recognition through retirement contributions or accounting methods

- Entity structure optimization — choosing the most tax-efficient business form

- Tax credit utilization — claiming available credits like R&D or energy incentives

How to avoid the 32% tax bracket as a roofing contractor?

Four strategies work together to keep income out of the 32% bracket: maximize SEP IRA or Solo 401(k) contributions, claim Section 179 and vehicle deductions, elect S Corp status to cut self-employment taxes, and apply the 20% QBI deduction. Combined, these reduce taxable income while growing retirement savings tax-deferred.

What is the $2,500 expense rule for contractors?

The IRS de minimis safe harbor election allows businesses without applicable financial statements to expense items costing $2,500 or less per item or invoice rather than capitalizing and depreciating them. This simplifies deductions for tools, small equipment, and supplies.

How profitable is a roofing business?

Industry data from the National Roofing Contractors Association shows average net profit margins of just 2.8%. Strong performers reach 8-12%, and best-in-class contractors achieve 12-15%+. Profitability varies significantly by geography, job mix (insurance restoration vs. retail), and operational efficiency — making tax strategy critical to survival.

Can a roofing contractor write off roof repairs on taxes?

Yes — roofing contractors deduct the cost of materials, labor, and subcontractors used on client jobs as ordinary business expenses under Section 162. This is distinct from homeowners deducting roof repairs on personal residences, which IRS Publication 530 confirms are not deductible unless the property is a rental or qualifies for home office treatment.