Introduction

Roofing is one of the most hazardous trades in construction. Workers operate at dangerous heights, handle heavy materials, and navigate steep slopes in unpredictable conditions. In 2023, roofing contractors accounted for 26% of all fatal falls in construction—110 out of 423 fall deaths.

A single uninsured incident can destroy a roofing business overnight: a worker falls from a ladder and sustains life-changing injuries, debris damages a client's vehicle, or a stolen tool trailer halts operations for weeks.

Insurance isn't just about managing those risks — it's a basic business requirement. Most homeowners and general contractors require proof of coverage before signing contracts, and several states mandate workers' compensation and contractor licensing bonds. Operating without it exposes you to civil penalties, personal liability for employee injuries, and losing jobs to competitors who carry proper coverage.

This guide breaks down the essential insurance policies roofing contractors need, what each covers, typical costs, and how to choose the right provider for your business.

TL;DR

- Roofing contractors need general liability, workers' comp, commercial auto, and tools/equipment insurance as baseline coverage

- Workers' comp is legally required in most states; general liability is required in practice by clients

- General liability insurance averages $267/month for roofers; bundling policies can cut premiums by 10–20%

- Top providers include ERGO NEXT, The Hartford, Thimble, Chubb, and Travelers—each with distinct strengths for roofing-specific risks

- Established roofing contractors can also set up their own reinsurance programs—turning warranty risk into a profit center instead of a recurring expense

What Business Insurance Do Roofing Contractors Need?

"Roofing insurance" isn't one policy—it's a package of coverages tailored to the unique risks of the trade. Falling debris, property damage, vehicle incidents, and faulty workmanship claims all require separate coverage types. Your exact needs vary by business size, employee count, and whether you focus on residential re-roofing or commercial flat roofs.

Required Coverages

General Liability Insurance

General liability is the cornerstone policy for roofers. It covers third-party bodily injury and property damage claims—such as when falling debris damages a client's vehicle or a neighbor slips on loose materials. Most small businesses choose GL limits of $1 million per occurrence and $2 million aggregate, though commercial jobs often require higher limits.

This coverage is required by virtually all client contracts and most state contractor licensing boards. When evaluating GL policies, understand the difference between occurrence-based and claims-made forms:

- Occurrence-based: Triggered by incidents during the policy period, regardless of when the claim is filed

- Claims-made: Triggered only when the claim is made during the active policy period; requires tail coverage for claims filed after cancellation

Occurrence-based policies are typically better for roofing contractors due to the potential for long-tail property damage and bodily injury claims that may not surface until months or years after project completion.

Workers' Compensation Insurance

Workers' comp is legally mandated in most states for any business with employees. It covers medical expenses, lost wages, and rehabilitation for workers injured on the job. Falls from ladders are the most common roofing claim—in 2024, falls accounted for 389 fatalities in construction, with roofing contributing a disproportionate share.

Texas is the notable exception where workers' comp is elective for most private employers, though non-subscribers must file DWC-5 forms and meet reporting requirements. Solo contractors should carry coverage given the physical demands of roofing and personal liability exposure when operating uninsured.

Commercial Auto Insurance

Personal auto policies almost always exclude business use. Any truck, van, or trailer used to haul shingles, ladders, or crew to job sites needs commercial auto coverage. Commercial auto provides higher limits, covers multiple drivers, and protects vehicles used to transport equipment and tow business trailers.

Optional but Recommended Coverages

Tools and Equipment Insurance / Inland Marine

Tools and equipment coverage pays to repair or replace nail guns, scaffolding, and ladders if damaged, lost, or stolen on or off the job site. Construction companies lose an estimated $300 million to $1 billion per year to equipment theft.

For smaller contractors, a basic tools-and-equipment policy may suffice. Larger operations benefit from inland marine "floaters" that cover owned, leased, or borrowed equipment at job sites, in transit, and in storage—offering broader protection than location-tied property endorsements.

Here's how the remaining optional coverages compare:

| Coverage | What It Covers | Best For |

|---|---|---|

| Professional Liability (E&O) | Faulty workmanship, errors, negligence claims | Contractors offering design or consulting services |

| Business Owner's Policy (BOP) | GL + property + business interruption in one policy | Smaller roofing operations seeking cost efficiency |

| Commercial Umbrella | Excess liability above standard GL limits | Large commercial projects or high-value residential work |

Best Business Insurance Companies for Roofing Contractors

The following providers were evaluated on coverage options tailored to roofing trades, financial strength ratings, complaint records, ease of obtaining certificates of insurance, and overall value. Use the profiles below to match your business size and work type to the right carrier.

NEXT Insurance

Background: Digital-first insurer backed by Munich Re, NEXT Insurance earned an A+ (Superior) Financial Strength Rating from AM Best in September 2025. The company offers policies designed specifically for contractors including roofing businesses, with instant online quotes, policy purchase, and 24/7 certificate of insurance downloads—highly valued by contractors who need proof of coverage before starting jobs.

NEXT Insurance bundles general liability with contractor errors and omissions (E&O) coverage, protecting roofers if a client claims faulty workmanship caused property damage. The company consistently earns top marks for workers' compensation pricing among roofing contractors. Roofing contractors report general liability starting around $82–$83 per month depending on business profile and location.

| Best For | Roofing contractors who want digital-first convenience and bundled GL + E&O coverage |

|---|---|

| Financial Strength | A+ (AM Best), backed by Munich Re |

| Key Feature | Instant COI download 24/7; competitive workers' comp rates for roofers |

The Hartford

Background: One of the oldest U.S. commercial insurers with deep expertise in contractor coverage. The Hartford offers business owner's policies, workers' comp, professional liability, and commercial auto. Hartford Fire Insurance Company holds an A+ Financial Strength Rating from AM Best. The company is known for professional guidance and the ability to add additional insureds online quickly.

Specialty in contractor coverage means underwriters understand roofing-specific risks. The Hartford reports average small business costs of $810/year for GL and $744/year for professional liability, though roofing-specific rates will vary by location and claims history.

| Best For | Established roofing businesses seeking comprehensive contractor-specific coverage with strong customer support |

|---|---|

| Financial Strength | A+ (AM Best); low complaint ratio relative to market size |

| Key Feature | Competitive professional liability rates; flexible BOP with add-on options |

Thimble

Background: Insurtech provider offering pay-as-you-go coverage by job, month, or year—underwritten by A-rated carriers including Markel Insurance. Thimble's digital platform enables instant certificates and flexible payment options suited to seasonal roofing operations.

Pay-as-you-go coverage is ideal for seasonal roofing contractors or those working project-to-project. Thimble offers competitive general liability and BOP rates; pricing varies by project scope and season, so request a quote for current rates.

| Best For | Small or seasonal roofing contractors seeking affordable coverage with flexible payment options |

|---|---|

| Financial Strength | Backed by Markel Insurance and other A-rated AM Best carriers |

| Key Feature | Pay-per-job or monthly coverage options; accessible pricing for smaller operations |

Chubb

Background: Global commercial insurer offering policies for businesses earning under $2 million in annual revenue. Chubb's business owner's policy includes robust property and liability enhancements, with low complaint ratios and exceptional financial strength.

Best option for roofing contractors working on high-value residential projects or commercial properties where clients require higher coverage limits. Chubb's reputation makes it a preferred carrier for general contractors and property owners who specify minimum insurer requirements.

| Best For | Mid-to-large roofing businesses or those working on high-value commercial projects requiring robust liability limits |

|---|---|

| Financial Strength | A++ (AM Best); among the lowest complaint ratios for commercial insurers |

| Key Feature | Comprehensive BOP enhancements; high-limit policies for commercial roofing work |

Travelers

Background: Major commercial insurer with over 700 underwriters, claims, and risk control professionals dedicated to construction. Travelers offers multiple policy options including general liability, workers' comp, commercial auto, and inland marine for roofing businesses of all sizes.

In-house construction risk management experts advise on safety improvements that can reduce premiums over time. A strong fit for roofing contractors looking to scale from residential into commercial work.

| Best For | Growing roofing contractors expanding into commercial work who want risk management support |

|---|---|

| Financial Strength | A++ (AM Best); dedicated construction industry underwriting team |

| Key Feature | In-house construction risk management experts; scalable coverage for residential and commercial work |

How Much Does Roofing Business Insurance Cost?

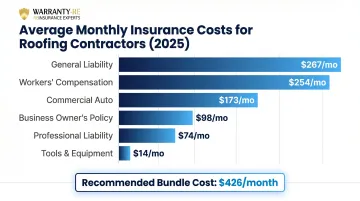

Roofing business insurance costs more than most other contractor trades due to fall risks and weather exposure. Based on 2025 market data from Insureon, median monthly costs for roofing contractors are:

- General Liability: $267/month ($3,200/year) — typical limits $1M per occurrence / $2M aggregate

- Workers' Compensation: $254/month ($3,054/year)

- Business Owner's Policy (BOP): $98/month ($1,173/year)

- Professional Liability (E&O): $74/month ($886/year)

- Commercial Auto: $173/month ($2,075/year)

- Contractor's Tools & Equipment: $14/month ($169/year)

A recommended comprehensive bundle (BOP + workers' comp + professional liability) will run approximately $426/month or $5,113/year, though actual costs vary significantly by business profile.

Cost Factors That Affect Your Premiums

Several variables drive your final premium — some within your control, some not:

- Payroll and headcount: Workers' comp is priced per $100 of payroll using class codes. Roofing class code 5551 carries one of the highest base rates in the trades.

- State: Florida charges $6.75 per $100 payroll for roofers; Michigan runs $6.20; South Carolina $6.00. Storm frequency and state regulations push rates up in high-risk markets.

- Scope of work: Commercial flat roofs, steep-slope jobs, and anything above three stories carry higher risk. Multi-story work can trigger height exclusions in standard GL policies that require separate endorsements.

- Claims history: Your Experience Modification Rate (EMR) reflects past losses — an EMR above 1.0 raises premiums; below 1.0 reduces them.

- Coverage limits: Commercial contracts often require $2M+ liability limits versus $1M for residential, which increases premiums proportionally.

Tips to Lower Your Roofing Insurance Costs

- Bundle policies with one provider to access multi-policy discounts—often 10–15% savings

- Pay annually rather than monthly to avoid installment fees

- Invest in documented safety training and OSHA compliance programs; insurers offer discounts for clean claims records

- Raise deductibles on equipment coverage (but keep general liability deductibles lower given the cost of roofing-related lawsuits)

How to Choose the Best Business Insurance for Your Roofing Company

Choosing the right business insurance starts with understanding your actual risk exposure — and roofing carries some of the highest in the trades. Before comparing quotes, take stock of what your company actually needs.

Start with your state's minimum requirements. Most states require roofing contractors to carry General Liability and Workers' Compensation before they can pull a permit or get licensed. Know your minimums before adding anything else.

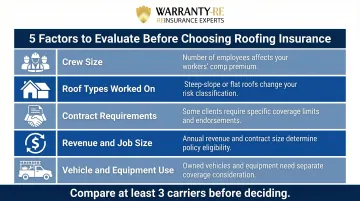

From there, build your coverage around these key factors:

- Crew size: More employees means higher Workers' Comp premiums and greater liability exposure on job sites

- Roof types you work on: Steep-slope residential, commercial flat roofing, and metal roofing each carry different risk profiles

- Contract requirements: General contractors and property managers often require $1M–$2M in General Liability coverage before they'll hire a sub

- Revenue and job size: Larger projects may require umbrella or excess liability coverage to close the contract

- Vehicle and equipment use: If your crew drives company trucks or hauls equipment, you need commercial auto and inland marine coverage

Once you know what you need, compare at least three carriers. Look beyond the premium — check coverage limits, exclusions, and how each carrier handles claims. A policy that saves $100 a month but excludes wind damage or subcontractor liability can cost you tens of thousands on a single job.

Also consider your long-term risk management strategy. Business insurance protects against third-party claims and workplace accidents. But labor warranty risk — the cost of fixing your own workmanship after the job closes — is a separate exposure that standard insurance policies don't cover. Roofing contractors who offer labor warranties without a structured program absorb those costs entirely out of pocket.

This is where reinsurance programs like those offered by WarrantyRE come in. Rather than paying a third-party warranty provider every time you sell a labor warranty, you can establish your own warranty company and capture those underwriting profits for yourself — while staying protected against unexpected claims.