This guide separates what NJ actually mandates from what's strongly recommended, so you can stay compliant, protect your business from genuine financial risk, and understand exactly what you're paying for and why.

TL;DR

- NJ law requires general liability (minimum $300,000), workers' compensation (if you have employees), and commercial auto (for business vehicles)

- A $1,000 surety bond is also required by the NJ Board of Examiners — separate from insurance, and it must be repaid if a claim is paid out

- A BOP, tools and equipment coverage, and commercial umbrella are not legally required but are expected by most GCs and commercial clients before they'll award contracts

- General liability for NJ electricians runs around $684/year for a solo operator at standard limits, per Insureon benchmarks

- A Certificate of Insurance (COI) is routinely required before work begins — GCs and property managers will ask for it before day one on site

Insurance Required by New Jersey Law for Small Electrical Businesses

Operating without required coverage in New Jersey isn't just a paperwork problem. It can mean fines, license suspension, and personal exposure when a claim hits. Three policies are legally mandated depending on your business structure.

Workers' Compensation Insurance

New Jersey law requires workers' compensation coverage for any employer with one or more individuals performing services for financial consideration. For electrical contractors, the NJ Board's statutory packet extends this requirement to cover both employees and subcontractors employed by the permit holder.

A few important nuances:

- Sole proprietors are exempt as the principal owner — but the moment you bring on even one other person, coverage is required

- Subcontractor classification matters — if a subcontractor doesn't carry their own workers' comp, you may be on the hook

- Solo operators without employees should still consider voluntary coverage. Most health insurance plans explicitly exclude on-the-job injuries, leaving a real gap

The NJ Compensation Rating and Inspection Bureau (NJCRIB) assigns electrical contractors under class code 5190 (Electrical Wiring — Within Buildings & Drivers), with a 2026 rate of $3.843 per $100 of payroll and a minimum premium of $1,200. For a business running $200,000 in payroll, that's roughly $7,686 in annual workers' comp premium before experience modifications.

General Liability Insurance

The NJ Board of Examiners of Electrical Contractors requires a minimum of $300,000 combined single limit general liability coverage as a condition of licensure. That's the floor, not the standard most commercial jobs actually require.

Most commercial clients and general contractor subcontracts require $1 million per occurrence / $2 million aggregate, which is also what the Hartford and Insureon identify as the typical small business benchmark.

General liability covers:

- Third-party bodily injury (a homeowner trips over your cable run)

- Property damage caused during the job

- Completed operations coverage — claims that surface after the job is done, including a fire traced to a wiring connection made six months ago

Completed operations exposure is especially significant for electricians because wiring defects can go undetected for months — then surface as a fire or code violation long after your crew has moved on.

Commercial Auto Insurance

New Jersey requires commercial auto insurance for any business-owned vehicle used for work. Personal auto policies exclude regular business use, leaving you personally exposed after an accident.

Under NJ DOBI Bulletin 24-07 (effective July 1, 2024), commercial motor vehicle minimum limits are:

| Vehicle GVWR | Required Minimum Coverage |

|---|---|

| Under 10,001 lbs (vans, light trucks) | $300,000 combined single limit |

| 10,001 – 26,001 lbs | $300,000 combined single limit |

| 26,001 lbs or more | $1.5M combined single limit |

Most electrical contractors operate vans and light trucks that fall under the $300,000 CSL minimum — though many GC subcontracts and umbrella structures assume higher underlying limits.

If employees use their personal vehicles for business errands, hired and non-owned auto (HNOA) coverage fills the liability gap. It won't cover damage to the employee's personal vehicle, but it protects your business from liability claims when the accident happens on company time.

Recommended Insurance for NJ Electrical Contractors

These coverages aren't mandated by NJ law, but many are required by client contracts, GC subcontracts, or both. Treating them as optional is a mistake most contractors only make once.

Business Owner's Policy (BOP)

A BOP bundles general liability, commercial property insurance, and business interruption coverage into one package — typically at a lower combined cost than purchasing each separately. For electrical contractors operating from a fixed location (office, warehouse, or shop with equipment), it's the most practical starting point.

According to Insureon, electricians pay an average of $78/month ($936/year) for a BOP. The business interruption component replaces lost income if a covered event — fire, vandalism — forces a temporary shutdown.

BOP eligibility generally requires fewer than 100 employees and a lower-risk business classification. Most small NJ electrical operations qualify.

Contractor's Tools and Equipment Insurance

General liability does not cover your own tools. That's a coverage gap that catches contractors off guard.

Tools and equipment insurance (also called inland marine or equipment floater coverage) covers:

- Theft, damage, or loss of tools at job sites, in transit, or stored temporarily off-site

- Equipment like multimeters, voltage testers, conduit benders, ladders, and generators

- Items valued over $2,500 may need to be scheduled separately on the policy

It does not cover normal wear and tear, intentional misuse, or natural disasters like floods or earthquakes.

The cost is manageable: Insureon reports electricians pay around $41/month ($492/year) for tools valued at $10,000 or less.

Commercial Umbrella Insurance

Umbrella coverage activates when underlying policies — general liability, commercial auto, workers' comp — reach their limits. For electrical contractors, this matters most given completed operations exposure. A single commercial structure fire traced to a prior installation can easily exceed a $1 million GL limit.

Beyond risk management, umbrella coverage is increasingly a bid requirement. Larger GC subcontracts and commercial projects often list it as a condition of the contract, making it a growth enabler as much as a protection tool.

Turning Warranty Obligations Into a Revenue Stream

Umbrella insurance addresses what happens when a claim exceeds your policy limits. A related exposure — one most contractors don't have a structure for — is the labor warranty sitting on your books after every completed job.

Equipment manufacturers like Square D, Leviton, and Siemens cover their hardware. But the labor — every connection your electricians make — sits on your books. When a breaker trips, a neutral comes loose, or a fixture fails six months after inspection, that callback is yours.

WarrantyRE works with electrical contractors to build a reinsurance structure that captures a small warranty fee on every job, routes it into a contractor-owned account, and covers claims when they arise. Unused funds stay with the contractor — not a third-party warranty company. WarrantyRE handles all claims administration and program management so contractors stay focused on the work.

Instead of absorbing callback costs as overhead, a labor warranty reinsurance program lets you fund that exposure through the jobs themselves — and keep what you don't spend.

NJ Electrical Licensing and Your Insurance Obligations

The NJ Board of Examiners of Electrical Contractors ties licensure directly to insurance. Here's what you're required to carry and maintain:

General Liability: Minimum $300,000 combined limit, with proof submitted at renewal. Cancellation of required insurance isn't effective until the Board receives at least 10 days' written notice — meaning your agent needs to notify the Board directly if a policy lapses.

Surety Bond: NJ law requires a $1,000 bond in favor of the State of New Jersey, valid for 24-month terms and renewed each cycle. This is not insurance. A surety bond is a financial guarantee that you'll fulfill contractual and regulatory obligations — and unlike insurance, if the surety pays a claim on your behalf, you owe that money back.

Both requirements feed into license continuity. Let either lapse and you're exposed:

- A license not renewed within 30 days of expiration is suspended without a hearing

- An insurance lapse triggers the same result — no grace period, no warning

- Reinstatement requires time and paperwork your business may not be able to afford mid-job

Certificates of Insurance (COIs): GCs and commercial clients routinely require a COI before work starts, and often require being named as an additional insured. An insurance provider who can turn around COIs same-day keeps you in the running for jobs that competitors with slower providers lose before the conversation even starts.

What Electrical Contractor Insurance Costs in New Jersey

Costs vary by business size, type of work (residential vs. commercial vs. high-voltage industrial), payroll, claims history, and coverage structure. Here are sourced benchmarks:

| Coverage | Approximate Annual Cost | Source |

|---|---|---|

| General Liability ($1M/$2M limits) | $684/year ($57/month) | Insureon |

| Workers' Comp (code 5190) | $3.843 per $100 payroll, min. $1,200 | NJCRIB 2026 |

| Commercial Auto (per vehicle) | $1,680/year ($140/month) | Insureon |

| Tools & Equipment (up to $10K) | $492/year ($41/month) | Insureon |

| BOP (GL + property bundled) | $936/year ($78/month) | Insureon |

Combined cost example — 2-3 person NJ electrical business:

A typical operation with two field electricians, one work vehicle, and a small shop might carry:

- BOP: ~$936

- Workers' comp on $150K payroll: ~$5,765

- Commercial auto for one truck: ~$1,680

- Tools coverage: ~$492

That puts total annual insurance spend in the $8,873–$10,000+ range, before adding umbrella coverage, a second vehicle, or higher payroll.

Solo operators with no employees, one vehicle, and basic tools typically run closer to $2,500–$3,500 annually for GL (or BOP), commercial auto, and tools coverage.

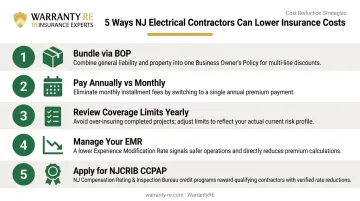

Smart Ways to Lower Your Electrical Contractor Insurance Costs in NJ

Five strategies can meaningfully reduce what NJ electrical contractors pay for coverage — without cutting protection they actually need:

Policy structure and payment terms are the fastest levers to pull:

- Bundle via a BOP. Combining general liability and commercial property under a Business Owner's Policy saves up to 10% versus separate policies, per NEXT Insurance — and streamlines renewals and COI requests.

- Pay annually instead of monthly. Installment plans carry financing fees; annual payment eliminates them and often unlocks an additional discount.

- Review coverage limits every year. Revenue, payroll, and equipment change — your policy structure should follow. Catching mismatches early prevents gaps and overpayments alike.

Workers' comp costs respond to two specific moves worth pursuing:

- Manage your EMR. NJ workers' comp premiums are calculated using an Experience Modification Rate — your actual losses compared to expected losses for your classification. An EMR below 1.0 lowers your premium; above 1.0 raises it. Consistent claims management is the most direct path to a better rate.

- Apply for the NJCRIB CCPAP. The NJ Construction Classification Premium Adjustment Program offers a premium credit for construction businesses where at least one classification averages at least $24.00 per hour. Qualifying electrical contractors apply directly through NJCRIB.

Frequently Asked Questions

How much does insurance for a small electrical business in New Jersey cost?

Costs vary by size and coverage type. A solo operator might pay $2,500–$3,500 annually covering general liability (or a Business Owner's Policy), commercial auto, and tools. A 2-3 person operation with employees and vehicles typically runs $8,000–$10,000+ annually once workers' comp, commercial auto, and full coverage are included.

Do electricians need to be licensed in NJ?

Yes. New Jersey requires electrical contractors to be licensed through the Board of Examiners of Electrical Contractors. Licensure requires proof of general liability insurance (minimum $300,000) and a $1,000 surety bond renewed every 24 months.

What type of insurance should an electrical contractor have?

The core stack for most NJ electrical contractors includes:

- General liability — required for licensing and nearly every job

- Workers' comp — required if you have employees

- Commercial auto — required for business vehicles

- Tools/equipment coverage and a BOP — strongly recommended

- Commercial umbrella — expected on larger commercial contracts

Is a surety bond the same as insurance for NJ electricians?

No. A surety bond is a financial guarantee that you'll meet contractual and regulatory obligations. Unlike insurance — where the insurer absorbs the loss — any claim paid against your surety bond must be repaid by you to the surety.

Do I need workers' compensation if I'm self-employed in NJ with no employees?

Technically, sole proprietors without employees are exempt from NJ's workers' comp mandate. But most health insurance plans exclude on-the-job injuries, which means a ladder fall or electrical burn isn't covered. Voluntary workers' comp coverage fills that gap.