A growing number of roofing contractors are switching to reinsurance programs that allow them to own their warranty structure, capture underwriting profits, and control claims. This shift represents a fundamental change in business strategy—turning warranty obligations into recurring revenue streams while maintaining customer loyalty and protection. The home warranty market alone generated $8.87 billion in revenue in 2025, yet most contractors still operate as intermediaries rather than beneficiaries of this massive opportunity.

This article breaks down what roofing warranty reinsurance is, who the top providers are, and what to look for when choosing the right partner to transform your warranty program from a cost center into a profit generator.

TL;DR

- Roofing warranty reinsurance lets contractors own and fund their own warranty program, replacing third-party providers and capturing profits that were going to third-party providers

- Top providers back programs with A-rated insurers, handle full administration, and charge transparent fees

- Evaluate providers on program structure, insurer financial ratings, and claims control authority

- Providers in this space include WarrantyRE, EFG Companies, AmTrust Financial Services, and select specialty administrators

- Long-term profitability and customer retention matter more than upfront setup costs when choosing a provider

What Is Roofing Warranty Reinsurance?

Roofing warranty reinsurance is a structured financial arrangement where roofing contractors establish and own their own warranty company instead of paying a third-party provider. In traditional models, when you sell a customer-facing warranty backed by a third-party company, all underwriting profits flow to that company. In a reinsurance structure, warranty premiums flow into a company you own or control—allowing you to capture 100% of the profits.

Three distinct types of warranty coverage exist in roofing:

- Manufacturer warranties cover product defects from brands like GAF, Owens Corning, or CertainTeed

- Contractor workmanship warranties cover installation-related issues the contractor offers directly

- Reinsurance-backed warranty programs let the contractor become the risk-bearing entity, supported by A-rated carriers

Of the three, the reinsurance model fundamentally changes how workmanship warranties work financially. Rather than purchasing coverage from a third party, contractors collect warranty fees from customers, invest those premiums in low-risk investments, and pay claims only when they arise. Any premiums not used for claims remain as profit.

The right reinsurance provider handles the legal, administrative, and compliance complexity, so contractors capture those profits without needing to become insurance experts.

Best Roofing Warranty Reinsurance Providers

Selection criteria include financial backing through A-rated carrier support, program structure integrity, administrative capability, compliance track record, contractor support quality, and the provider's tenure in the home services or roofing reinsurance space. The following providers represent the leading options for roofing contractors seeking to own their warranty programs.

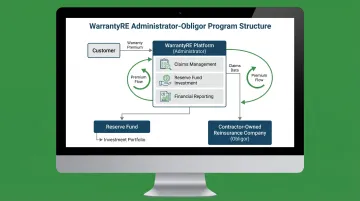

WarrantyRE

WarrantyRE is a Southeast Virginia-based reinsurance firm founded in 1994 by Tim Byrd. Originally built to serve auto dealers, the company has expanded to serve roofing, HVAC, plumbing, and electrical contractors nationwide. Over 30 years in business and experience helping 400+ auto dealers provides a deep operational foundation for its home services programs.

The company specializes in administrator-obligor (admin-obligor) reinsurance structures backed by A-rated insurers. In this model, contractors own their own reinsurance company—capturing 100% of underwriting profits, gaining claims control, and building a recurring revenue stream from each install. WarrantyRE provides full-service administration including training, claims adjudication, compliance, performance reporting, bookkeeping, and tax filings with transparent pricing.

Key operational benefits include:

- Complete claims management from first call to final resolution

- No adjusters to manage or claims paperwork for contractors

- Warranty fees built into job pricing (typically on $15,000+ roof replacements)

- Investment income on premium reserves (conservative government bonds initially, aggressive options once reserves exceed 125%)

- Tax-advantaged structure under IRS Code 831(b)

| Category | Details |

|---|---|

| Program Structure | Administrator-Obligor; contractor owns their reinsurance company, supported by A-rated insurers |

| Key Services | Full-service administration, onboarding, claims adjudication, compliance, tax filings, staff training, monthly financial reporting, reserve fund management |

| Best For | Roofing, HVAC, plumbing, and electrical contractors nationwide seeking to replace third-party warranty providers and maximize program profitability |

EFG Companies

EFG Companies was founded in 1977 by Oklahoma businessman Bob Moore, drawing on his experience as a car dealer. Headquartered in Irving, Texas, the company serves more than one million contract holders across auto dealers, agents, lenders, OEMs, and home warranty service providers.

EFG operates as a near 50-year consumer protection product company with SSAE-18 certification. For home services, EFG offers a Preferred Service Provider Program for HVAC and plumbing contractors — emphasizing guaranteed work, marketing support, and commission revenue.

This is not a contractor-owned reinsurance structure. EFG connects contractors to warranty work as a service provider network administrator, with a 21-day payment guarantee and a focus on referral income rather than underwriting profit retention.

| Category | Details |

|---|---|

| Program Structure | Service provider network model with commission revenue; not a contractor-owned reinsurance structure |

| Key Services | Contractor referrals, marketing support, 21-day payment guarantee, home warranty product administration (HVAC, plumbing, electrical, appliances) |

| Best For | Contractors seeking referral work and commission income rather than ownership of warranty underwriting profits |

AmTrust Financial Services

AmTrust Financial Services is one of the largest warranty underwriters globally — $8.8 billion in gross written premium, $27.1 billion in total assets, and 55 million active contracts as of 2024. The company holds an A- (Excellent) Financial Strength Rating from AM Best (Financial Size Category XV), affirmed in October 2025.

AmTrust's Warranty & Specialty Risk division serves 60+ partners across 55 countries, including third-party administrators, retailers, manufacturers, and financial institutions. Coverage spans automotive VSCs, consumer electronics, powersports/marine, heavy equipment, and home products.

AmTrust can serve as the A-rated backing carrier for contractor-owned warranty programs. That said, the company does not offer a dedicated roofing contractor reinsurance program with full-service administration — contractors typically access AmTrust's capacity through an established TPA or admin-obligor administrator.

| Category | Details |

|---|---|

| Program Structure | A-rated backing carrier for third-party administrators; CLIP (Contractual Liability Insurance Policy) provider; fronting arrangements for various warranty programs |

| Key Services | Insurance backing, CLIP coverage, warranty product underwriting, claims support for administrators |

| Best For | Large-scale operations requiring A-rated carrier backing, or contractors working through established TPAs needing financial stability from a highly rated insurer |

Other Providers

Residential Warranty Services (RWS) was founded in 1988 and is currently powered by Porch. The company offers one-year home warranties marketed through real estate agents across all 50 states. RWS functions as a traditional third-party home warranty provider — it does not offer contractor-owned reinsurance programs or admin-obligor structures.

Centerpoint Financial returned no authoritative results for a warranty reinsurance administrator in the home services or automotive space. Multiple unrelated entities exist under similar names (CenterPoint Energy, Centerpoint Financial Management), but none operate warranty reinsurance programs for contractors.

How We Chose the Best Roofing Warranty Reinsurance Providers

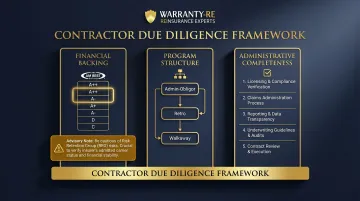

The roofing warranty reinsurance space lacks public rankings or consumer review platforms, so selection criteria focus on program structure integrity, carrier financial ratings, administrative depth, and contractor outcomes. Common mistakes contractors make include choosing providers based solely on ease of entry, ignoring fee structures, or not verifying the A-rating of the backing carrier.

Three core factors separate legitimate reinsurance programs from marketing arrangements:

Financial Backing

Is the program supported by an A-rated carrier through AM Best? According to AM Best's rating scale, only ratings from A- through A++ represent "Excellent" to "Superior" ability to meet ongoing insurance obligations. Ratings of B+ fall into the "Good" category but approach vulnerable territory. Contractors should verify the specific AM Best rating and confirm the backing carrier's name—not just accept generic claims of "A-rated support."

The California Department of Insurance specifically warns that Risk Retention Groups (RRGs) used to back some service contracts "are not licensed by the CDI and are not subject to the same strict financial and claim-handling regulations" as licensed insurance companies.

Massachusetts law adds another layer of risk: service contracts are not protected by state Guaranty Association funds. If both the provider and insurer fail, contractors have no state safety net.

Program Structure

Does the contractor actually own and control the reinsurance entity, or is it a managed third-party arrangement in disguise? True admin-obligor structures grant full ownership to the contractor, with all underwriting profits retained in a C Corporation the contractor controls. In contrast, "retro programs" offer profit-sharing without downside risk but don't provide full ownership, while "walkaway programs" simply pay commissions on third-party sales.

These distinctions carry real financial consequences. Under NAIC Model #685, service contracts are regulated by state Departments of Insurance for solvency standards and obligor disclosures—even though they are not classified as insurance contracts. The admin-obligor structure positions the contractor as the legal obligor on service contracts, backed by Contractual Liability Insurance Policies (CLIPs) from fronting carriers.

Ownership structure also determines who absorbs administrative burden—which brings us to the third factor.

Administrative Completeness

Does the provider handle compliance, tax filings, claims adjudication, and staff training, or does the contractor absorb that burden? Full-service administration means contractors receive:

- Monthly financial statements and performance reports

- Annual tax preparation coordination (including 831(b) compliance)

- All regulatory filings and state registrations

- Complete claims processing with no third-party adjusters needed

- Ongoing staff training and program updates

Partial administration creates hidden costs. If contractors must hire outside CPAs for tax compliance, engage separate claims adjusters, or manage regulatory filings independently, the program's profitability can erode by 20–30% or more. According to the NAIC framework, proper disclosure of the obligor, maintenance of solvency standards, and regulatory registration are mandatory—so gaps in administrative support translate directly into compliance exposure.

Conclusion

Structured correctly, roofing warranty reinsurance turns every warranty-backed install into a source of recurring profit, builds customer loyalty, and reduces dependence on third-party warranty companies that retain the financial upside.

The difference between traditional warranty models and reinsurance ownership is significant. In the traditional model, contractors act as sales agents for third-party providers, earning modest commissions while the provider keeps underwriting profits and controls claims decisions.

In the reinsurance model, contractors own the warranty company outright, invest premium reserves for additional ROI, and retain 100% of funds not used for claims — with administration handled by an experienced partner.

Evaluate providers based on long-term profitability potential and full-service administrative support — not just program entry fees or brand recognition. Three checks matter most:

- Verify carrier ratings directly through AM Best rather than accepting marketing claims

- Request transparent fee disclosure covering setup costs and ongoing administration

- Confirm the program structure grants true ownership, not a profit-sharing arrangement

Roofing contractors ready to explore owning their own warranty company can connect with WarrantyRE — a 30-year reinsurance partner serving contractors nationwide — to learn how an admin-obligor program can replace existing third-party warranty providers and start capturing profits currently given away. Call (804) 824-9533 to schedule an owner analysis consultation tailored to your specific business.

Frequently Asked Questions

What are the top reinsurance companies for roofing warranty programs?

The leading providers for roofing contractor warranty reinsurance include WarrantyRE, EFG Companies, and AmTrust Financial Services. The right fit depends on your program structure needs, volume, and whether you want full admin-obligor ownership versus a managed or service-provider-network model.

Who has the best roof warranty for contractors to offer customers?

Manufacturer warranties from GAF, Owens Corning, and CertainTeed cover material defects only. Contractor-backed reinsured warranties go further — giving you control over coverage terms and keeping the underwriting income in your own company instead of paying it to a third party.

What is the difference between a third-party warranty provider and a reinsurance program?

A third-party warranty provider pays claims but also keeps all premium income and underwriting profit. A reinsurance program allows the contractor to own the premium-funded entity, control claims, and receive the profits that would otherwise go to the third party—creating a recurring revenue stream from warranty sales.

How does an administrator-obligor reinsurance program work for roofing contractors?

In an admin-obligor structure, the contractor sets up their own warranty company (the obligor) backed by an A-rated insurer. You collect premiums from customers, invest them conservatively, and only pay out on actual claims. The contractor keeps the remainder as profit, with a reinsurance administrator handling compliance and operations.

Can small or mid-size roofing contractors afford a reinsurance program?

Reinsurance programs are not exclusively for large contractors. WarrantyRE has worked with contractors at various volume levels since 1994, and the program is often self-funding once you establish a steady warranty-backed install volume. Contractors should consult with a reinsurance provider to assess their specific revenue threshold and profitability potential.