What rarely gets explained is the financial relationship underneath that arrangement. Who owns the customer? Who controls the claim? And where does the premium revenue actually go?

This post answers those questions directly — comparing what it means to work for a third-party warranty company versus owning your own contractor reinsurance program, and what that difference means for your bottom line.

TLDR

- ARW Home dispatches contractors to fulfill warranty repairs; contractors earn a service fee, but ARW keeps the underwriting profit

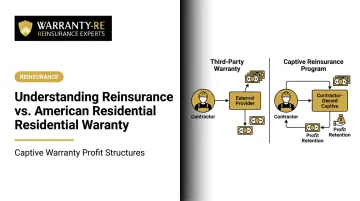

- Contractor-owned reinsurance flips this: the contractor becomes the warranty company and retains the premium pool

- Whoever owns the warranty structure captures the margin between premiums collected and claims paid

- WarrantyRE helps home service contractors set up their own administrator obligor reinsurance companies — covering compliance, claims, and reporting

What Is American Residential Warranty — And How Does It Use Contractors?

ARW Home is the operating brand for American Residential Warranty, a Florida-based company headquartered in Boca Raton (901 W Yamato Rd, Suite 100E). BBB records list the business start date as February 5, 2009. The company sells home warranty service plans directly to homeowners covering appliances and major systems.

When a covered item breaks down, ARW Home assigns a technician from its pre-approved contractor network — typically within 24 to 48 business hours, according to ARW's published claims process.

Contractors in that network are paid to complete the repair. They are not partners sharing in the revenue ARW collects from homeowners. They are subcontractors fulfilling warranty obligations on ARW's behalf.

What Third-Party Review Data Reveals

ARW Home's published coverage terms and third-party reviews offer a useful window into how the company manages claims — and where that process creates friction for the contractors doing the work:

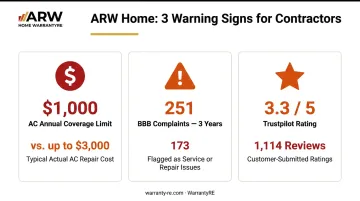

- ARW's official AC page cites a $1,000 annual limit for central air conditioning repairs, which can fall well short of actual costs that average around $350 but can reach $3,000 depending on the system

- BBB lists 251 complaints in the last 3 years, with 173 categorized as service or repair issues — the most common complaint type by a wide margin

- Trustpilot shows 3.3 stars from 1,114 reviews, with recurring themes around denied claims and dispatch dissatisfaction

For contractors, denied claims and delayed authorizations aren't just a customer satisfaction issue — that friction lands directly on the technician who showed up to do the job.

The Hidden Cost of Working for a Third-Party Warranty Company

The economics of a third-party warranty arrangement are rarely spelled out when a contractor joins a network. Here's what's actually happening financially:

The Profit Gap

Home warranty plans cost homeowners roughly $360 to $1,200 per year in premiums. That revenue flows entirely to the warranty company. Claims paid out represent their cost of services. Whatever remains is underwriting profit — and it belongs to the warranty company, not the contractor who did the work.

For context, publicly traded Frontdoor (parent of American Home Shield) reported $1.781 billion in 2025 revenue with $874 million in cost of services — roughly 49 cents of every dollar went to service and claims; the rest stayed with the company. That margin doesn't go to the contractor network.

The Claim Friction Problem

In a third-party network, the warranty company controls claim approval. That means:

- Contractors wait for authorization before proceeding with repairs

- Coverage caps may not reflect actual parts and labor costs

- Claims can be denied after a service call is completed

- The FTC notes that warranty companies may deny claims for lack of maintenance, pre-existing conditions, excluded parts, or use of a non-preferred contractor

The Rate and Customer Control Problems

Claim friction is only part of the problem. Two structural issues make the arrangement harder to sustain long-term:

Rate control: The warranty company sets the service fee, not the contractor. On complex jobs (an HVAC replacement, a full repipe, a panel upgrade), the reimbursement rate may not cover actual labor and parts costs.

Customer control: When a homeowner files a claim, they call ARW Home, not their contractor. The contractor becomes a dispatched technician rather than a trusted service provider with a long-term relationship. Repeat business, upsell opportunities, and referrals all flow to whoever owns the customer relationship — and in this model, that's the warranty company.

The contractor absorbs the operational risk of servicing aging systems under coverage caps. The warranty company keeps the margin. That's the core imbalance a reinsurance structure is designed to correct.

What Is Contractor-Owned Reinsurance?

Contractor-owned reinsurance inverts the model above. Instead of working for a warranty company's customers, the contractor creates their own warranty vehicle — an administrator obligor reinsurance company — and sells warranty agreements directly to their own customers.

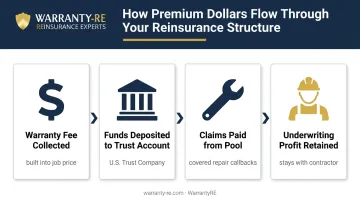

How the Premium Flow Works

When a contractor completes a job, a warranty fee is built into the project price. That fee flows into a reinsurance entity the contractor legally owns, held in a U.S. Trust Company account. The Trust Agreement establishes that funds can be withdrawn for four purposes:

- Payment of covered repair claims

- Limited professional fees

- Income tax payments

- Withdrawal of funds exceeding required reserves

When a warranty callback occurs, the claim is paid from this pool of customer-funded dollars. Whatever isn't paid out in claims — the underwriting profit — stays with the contractor.

That raises a fair question: what happens if claims exceed the pool?

The Risk Protection Layer

Contractor-owned reinsurance is not self-insurance without a backstop. In WarrantyRE's administrator obligor structure, the contractor's reinsurance entity is supported by an A-rated insurance carrier. If the reinsurance company cannot meet its obligations, the ultimate liability for claim payments rests with the direct writing insurance company. The contractor's exposure is limited to formation costs plus accumulated earnings — not unlimited liability.

The Investment and Tax Dimension

Premiums held in the trust account are invested in conservative instruments, with investment income belonging to the contractor's company. Once reserves exceed 125% of unearned premiums, excess funds can be invested more aggressively at the owner's direction.

The tax dimension adds another layer of financial benefit. Under IRS Code 831(b), property and casualty insurance companies with less than $2.9 million in annual net premiums may elect to be taxed only on investment income — not on underwriting profit. This is a complex area: IRS Notice 2016-66 and 2025 final regulations identify certain micro-captive structures as listed transactions or transactions of interest. Any tax planning around a reinsurance entity should involve a qualified CPA and legal counsel before implementation.

WarrantyRE's Role

WarrantyRE, founded by Tim Byrd in 1994 in Southeast Virginia, helps HVAC, roofing, plumbing, and electrical contractors establish and manage their own administrator obligor reinsurance companies. The company handles everything the contractor shouldn't have to build from scratch:

- Forms the entity and handles all legal filings, licensing, and state approvals

- Manages every tax return, renewal, and ongoing regulatory requirement

- Adjudicates claims from first call to final resolution

- Delivers monthly financial statements, annual reports, and performance analysis

Contractors own the company and keep the profits. WarrantyRE handles the administration so they don't have to.

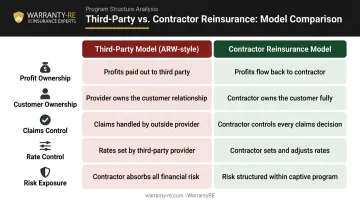

Reinsurance vs. American Residential Warranty: What the Difference Means for Your Bottom Line

| Factor | Third-Party Model (ARW-style) | Contractor Reinsurance Model |

|---|---|---|

| Profit ownership | Warranty company keeps underwriting margin | Contractor retains unused premium pool |

| Customer ownership | Customer belongs to warranty company | Customer belongs to contractor |

| Claims control | Warranty company approves/denies | Administrator obligor structure, claims managed by WarrantyRE |

| Rate control | Set by warranty company | Warranty fee built into contractor's own pricing |

| Risk exposure | Low reimbursement, authorization delays, volume loss | Regulatory compliance, actuarial discipline, reserve requirements |

The Profit Ownership Gap in Practice

Consider a contractor completing 200 warranty service calls per year for a third-party network. They earn a service fee on each call. The premium pool funding those service fees — collected from homeowners — stays entirely with the warranty company.

Now consider a contractor who sells 200 warranty agreements per year through their own reinsurance entity. The warranty fee is included in each job price. Claims come out of the pool. The remaining underwriting profit stays in the contractor's own company, available for withdrawal once reserves are properly funded.

The logic is straightforward: your third-party warranty provider is in business because the arrangement is profitable for them. Every dollar of underwriting margin they keep is a dollar that could stay in your company instead.

Customer Ownership and Lifetime Value

When the contractor owns the warranty program, they are the primary point of contact when something goes wrong. That direct relationship has compounding value. When a customer calls you about a warranty issue, that conversation creates natural openings for repeat maintenance visits, equipment upgrade discussions, and referrals to neighbors or family members. None of those opportunities exist when a third-party dispatcher owns the customer relationship instead.

The difference shows up in lifetime value. A contractor managing their own warranty program builds customer touchpoints that generate revenue well beyond the original job. A contractor feeding customers into a third-party network builds loyalty for someone else's brand.

Signs It Might Be Time to Build Your Own Warranty Program

These are practical indicators worth evaluating honestly:

- Reimbursement rates don't cover your actual costs. On HVAC, roofing, or plumbing jobs with significant parts and labor, the service fee from a third-party network may not reflect what the job actually costs you to complete

- Customers call the warranty company, not you. If homeowners are filing claims through ARW Home or similar companies, you're not building the service relationship — you're fulfilling someone else's obligation

- Your volume is consistent enough to model the math. The biggest misconception is that you need to be a large operation to qualify. Most smaller contractors were never introduced to reinsurance because they weren't marketed to — not because they're ineligible

- You have predictable failure data. Contractors with documented service history and consistent job volume are better positioned to price warranties accurately and reserve for claims responsibly

If two or more of these apply to your business, it's worth running the numbers. WarrantyRE offers a direct analysis of your volume and service history to show whether a contractor-owned program makes financial sense for your operation.

Frequently Asked Questions

Is American Residential Warranty any good?

Reviews are mixed. BBB lists 251 complaints over 3 years, predominantly service and repair issues, while Trustpilot shows 3.3 stars. From a contractor's perspective, third-party networks like ARW's come with claim authorization friction, coverage cap limitations, and reimbursement rates the contractor doesn't control. Know what you're agreeing to before joining.

Who owns American Residential Warranty?

ARW Home is the operating brand for American Residential Warranty, headquartered in Boca Raton, Florida. Coverage obligations are carried by entities including Ironwood Warranty, LLC and AMT Home Protection Company depending on state, with American Protection Plans, LLC serving as the listed administrator.

What is the difference between a home warranty and contractor reinsurance?

A home warranty is a consumer product sold to homeowners — the warranty company holds the contract and captures the premium. Contractor reinsurance is a business structure that lets the contractor own the warranty vehicle itself, retaining the premium pool and underwriting profit rather than performing service work for someone else's program.

Can a home service contractor own their own warranty company?

Yes. Contractors can establish their own administrator obligor reinsurance companies through an experienced administrator like WarrantyRE, which handles company formation, licensing, compliance, claims adjudication, and financial reporting — so the contractor owns the structure without building the infrastructure independently.

How does reinsurance protect contractors from warranty risk?

The administrator obligor structure is backed by an A-rated insurance carrier, meaning if the contractor's reinsurance entity cannot meet its obligations, the direct writing insurance company carries the ultimate liability. The contractor's exposure is limited to formation costs plus accumulated earnings, not open-ended downside.

What should a contractor evaluate before joining a third-party warranty network?

Review the reimbursement rate structure relative to your actual cost of service, understand how claims are authorized and what happens when they're denied, and assess whether the arrangement builds any long-term business value — or simply generates revenue you can't compound, retain, or exit on.