The choice between using a third-party warranty company and setting up a reinsurance-backed warranty program directly impacts your profit margins, claims control, customer loyalty, and long-term business value. For established plumbing contractors, this decision represents one of the highest-leverage financial moves available—yet most don't even know reinsurance is an option.

TL;DR

- Third-party warranty companies collect premiums from your customers and keep underwriting profits; you get a referral fee at best

- With reinsurance, you own the warranty company — backed by A-rated insurers — and keep those underwriting profits yourself

- Third-party plans are easier to start but hand over control of claims decisions, pricing, and customer experience to someone else

- Reinsurance takes more setup, but it turns warranty obligations into recurring revenue and a real business asset

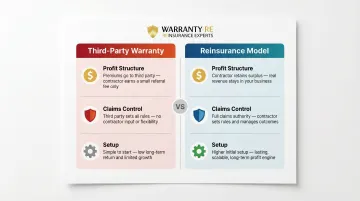

Plumbing Warranty Reinsurance vs. Third-Party Warranty Companies: Quick Comparison

Here's how the two models stack up across the dimensions that matter most to plumbing contractors:

| Dimension | Third-Party Warranty Company | Reinsurance Model |

|---|---|---|

| Profit Structure | Premiums go to the third party; you earn a small referral fee. Underwriting profits stay with the warranty company. | Your reinsurance company retains premium income. The surplus after claims belongs to you. |

| Claims Control | The third party sets approval rules, coverage limits, and exclusions. You have no say in the customer experience. | You control claims adjudication, coverage terms, and customer service—fewer disputes, higher satisfaction. |

| Setup & Management | Simple to start with low upfront effort. Low long-term return. | Requires a compliant reinsurance entity and a reinsurance partner. Ongoing administration covers compliance, tax filings, and reporting. |

What Is a Third-Party Plumbing Warranty Company?

A third-party warranty company is a separate business entity—often a home warranty or extended service contract provider—that creates and administers warranty products plumbing contractors can sell or recommend to customers. The contractor markets the warranty, the customer pays premiums to the third party, and the contractor earns a small sales fee or markup while the third party keeps the bulk of collected premiums and all underwriting profit.

Your customer pays, the warranty company collects, and you receive a fraction. Frontdoor Inc., parent company of American Home Shield, reported a 55% gross margin in FY2025, meaning for every dollar of premium collected, roughly $0.55 was retained as gross profit before operating expenses — that's the margin you forfeit when using a third party.

Typical Coverage Structures

Third-party plumbing warranty plans operate within strict coverage caps and exclusions:

Coverage Caps:

- American Home Shield's ShieldSilver plan carries a $50,000 aggregate limit per agreement term

- ShieldGold allows $2,000 per covered appliance; ShieldPlatinum allows $4,000

- All AHS plans cap HVAC systems at $5,000 and plumbing access through concrete at $1,000

- Service call fees range from $100-$125 per request at AHS, with industry averages between $65-$150

Common Exclusions: Per AHS's plumbing coverage terms, most third-party plans exclude septic tanks (unless purchased as an add-on), fire suppression systems, root intrusion damage, collapsed external lines, water softeners, bathtub and sink fixtures, and consequential water damage to floors or walls.

These caps create a structural problem: when a major plumbing system fails and the claim exceeds coverage limits, the homeowner faces unexpected out-of-pocket costs, leaving your reputation to bear the fallout.

The Claims Experience Risk

Because third parties control claim approvals, contractors routinely see their reputations suffer when customer claims are denied, delayed, or disputed—even though the contractor initially sold the warranty.

A Forbes Home survey of 1,800 customers found 13% experienced a claim denial. A This Old House survey of 2,000 customers reported approximately 4% of claims denied. The top denial reasons were:

- Preexisting conditions (29%)

- Items not covered under the plan (29%)

- Repair costs exceeding coverage limits (20%)

- Lack of maintenance (13%)

Complaint volumes tell the same story. American Home Shield alone accumulated 15,597 BBB complaints over three years, with 4,541 closed in the most recent 12 months.

In January 2026, Arizona's Attorney General secured an $11.8 million settlement with Choice Home Warranty — the largest home warranty settlement in Arizona history — for misrepresenting coverage and failing to replace covered items.

When a third-party provider denies a claim or delays payment, the homeowner blames the contractor who recommended the plan. You lose control of the customer relationship at the exact moment it matters most.

Use Cases for Third-Party Plumbing Warranty Plans

Third-party plans make sense in limited scenarios:

- New contractors entering the warranty space who want minimal administrative overhead and aren't ready to establish their own program

- Low install volume operations that haven't reached the scale needed to make a captive warranty program profitable

- Testing warranty offerings as an occasional add-on rather than a core service component

- Businesses without capital to fund reserve requirements for a reinsurance structure

If you're just starting to offer warranties and want a plug-and-play solution, a third party provides immediate access. But the moment your volume justifies it, continuing to rely on a third party means permanently ceding a profit center that could be owned in-house.

What Is Plumbing Warranty Reinsurance?

Plumbing warranty reinsurance is a structure where the plumbing contractor establishes their own administrator-obligor warranty company (meaning they both administer the warranties and are obligated to pay claims) while a reinsurance arrangement with an A-rated insurer provides a financial backstop against catastrophic claim losses.

How the Profit Flow Works

The contractor's own warranty company collects customer premiums. A portion is ceded to the reinsurer for risk protection. The remaining underwriting profit (the surplus after claims and reinsurance costs) stays inside the contractor's company, building equity and investment capital over time.

Practical example: On an $8,000 full-house repiping job with a 1-year labor warranty, the warranty fee is built into the job price. That fee flows into your reinsurance account, not to an outside company. When a callback occurs, it's covered by your reinsurance structure. The money that wasn't used for claims stays with you as profit.

Tax and Investment Advantages

Under IRC Section 831(b), qualifying small captive insurance companies pay 0% federal income tax on underwriting profits-election-for-captives); only investment income is taxable. The premium threshold is capped at $2.2 million per taxable year (inflation-adjusted). For plumbing contractors running consistent install volume, warranty fees that would otherwise go straight to the IRS instead stay inside a structure that's building value for your business.

Under an 831(b) election, only investment income generated on reserves is taxable — premiums themselves accumulate to fund losses. Here's how the investment progression works:

- Premiums collected accumulate in the captive and are available to pay claims

- Initial reserves are invested conservatively in government bonds per insurance regulatory guidelines

- Once cash reserves exceed 125% of unearned premiums, ownership can redirect excess funds into higher-yield investments

- That additional investment income becomes a secondary ROI stream on top of underwriting profits

Important: All tax-related decisions require consultation with a qualified tax professional. Premium deductibility requires meeting a four-part test: presence of insurance risk, risk shifting, risk distribution, and transaction recognized as insurance in its commonly accepted sense.

Compliance and Administration Requirements

Owning a warranty reinsurance company involves state-level compliance, contract filings, financial reporting, and actuarial considerations. Forty-two states have adopted the NAIC Service Contracts Model Act (#685), placing service contracts under Department of Insurance oversight. Eight jurisdictions (DE, DC, IN, MI, NJ, PA, SD, TN) regulate through non-DOI mechanisms.

Key compliance requirements under Model #685 include:

- Maintaining contractual liability insurance (CLIP) to ensure claims are paid if the provider becomes insolvent

- Meeting financial stability provisions for contract administrators

- Disclosing specific information in contracts and regarding reimbursement insurance

- Keeping accurate transaction and contract records

- Avoiding any deceptive or unfair business practices

The compliance requirements are substantive, and proper structuring from the start makes them manageable. A full-service reinsurance partner like WarrantyRE manages all legal forms, filings, tax returns, renewals, and claims adjudication, making the program operationally accessible for plumbing contractors without in-house insurance expertise.

Use Cases for Plumbing Warranty Reinsurance

Reinsurance fits established plumbing contractors with consistent install volume who want to convert their warranty program from a cost line into a profit center and customer retention engine.

How reinsurance turns installs into recurring revenue: Every system installed and warranted creates an ongoing relationship. You receive premiums, control service, and build a reserve pool that is your own business asset, not a third party's. Over time, as claims are paid and reserves accumulate, the unused surplus becomes equity in a tax-advantaged entity you own outright.

Reinsurance vs. Third-Party Warranty: Which Model Wins for Plumbing Contractors?

The core financial trade-off is simple: third-party plans offer simplicity at the cost of profit leakage. Reinsurance requires setup investment but recaptures those margins permanently.

The Financial Reality

Frontdoor's FY2025 results show cost of services at approximately 45% of revenue, retaining roughly 55 cents of every premium dollar as gross profit. After selling and administrative expenses, adjusted EBITDA margin reached approximately 26%. For context, IRS Notice 2016-66 flags captive insurance arrangements as "transactions of interest" when the loss ratio falls below 70% over five years-election-for-captives). Frontdoor's implied loss ratio of 45% illustrates the scale of underwriting profit embedded in the home warranty business model. That's profit you're handing to a third party with every warranty you sell.

Those margins exist inside a growing market. The US home warranty sector reached $8.87 billion, growing at an average 3.9% annually over the past five years, and that demand isn't slowing down. Contractors who own their warranty programs capture that growth directly.

The Customer Experience Advantage

When you control claims, you can resolve issues faster, approve more reasonable claims, and use warranty service calls as touchpoints to deepen the customer relationship—driving repeat business, referrals, and maintenance agreements.

Third-party providers create structural conflict. Contractor forum data indicates effective hourly rates of $35-$50 for warranty work versus $125-$175 for retail work, with warranty companies expecting contractors to maintain average cost of $350 per call. Warranty work reportedly has a 15-20% higher callback rate than retail work due to older, deteriorated equipment. Contractors describe being caught between homeowner expectations and warranty company pressure to repair rather than replace—creating service delays and dissatisfaction.

When you own the warranty program, those conflicts disappear. You decide what's covered, how claims are handled, and how to balance cost control with customer satisfaction. Your brand, your rules.

Which Model Fits Your Business?

Choose third-party if:

- You're a newer or lower-volume operation testing the warranty market without capital commitment

- You prefer simplicity over long-term profit potential

- Your install volume doesn't yet justify the infrastructure of a captive program

Choose reinsurance if:

- You're an established contractor looking to build long-term business value

- You want to control your brand reputation and customer experience

- You're ready to stop funding a third party's profits and capture underwriting margins yourself

WarrantyRE has over 30 years of experience helping more than 400 business owners build reinsurance programs, now including plumbing contractors. If you're ready to explore whether reinsurance makes sense for your plumbing business, WarrantyRE offers a no-obligation business analysis.

Conclusion

Third-party warranty companies serve a real purpose for contractors in early stages or low volume. But for established plumbing businesses, continuing to rely on a third party means permanently ceding a profit center that could be owned in-house.

The most profitable plumbing contractors of the next decade will be those who treat warranty programs as a business asset—not just a line item on a service agreement. The shift from third-party dependency to reinsurance ownership puts underwriting profits back in your pocket instead of a provider's. For contractors already selling warranties at volume, that gap between what you pay out and what you keep is real money left on the table every year.

Frequently Asked Questions

Should my home warranty cover plumbing?

Most standard home warranty plans include plumbing system coverage, but specifics vary by provider. According to American Home Shield's coverage page, commonly covered items include interior pipes, water heaters, drain lines, toilets, and fixtures, while septic systems, sprinkler lines, and damage from root intrusion are typically excluded.

Why isn't plumbing covered by insurance?

According to the Insurance Information Institute, standard homeowners insurance covers sudden, accidental damage like a pipe burst from a storm, but not wear-and-tear breakdowns. That's the gap plumbing warranties fill — coverage for mechanical breakdown and component failure over time, not sudden accidents.

Why would a plumber need professional liability?

Professional liability (errors and omissions) insurance protects a plumber if a client claims financial harm due to faulty advice or workmanship errors. This is separate from warranty coverage—warranties cover component failure; professional liability covers negligence claims.

Can a plumbing contractor set up their own warranty company?

Yes. Through an administrator-obligor reinsurance structure, a plumbing contractor can establish their own warranty entity, backed by an A-rated reinsurer, and retain underwriting profits rather than paying a third-party provider. WarrantyRE manages all compliance, claims, and administration.

What is the difference between a third-party warranty and an administrator-obligor reinsurance structure?

In a third-party warranty, an outside company collects premiums and controls claims. In an administrator-obligor reinsurance structure, the contractor's own company administers and is obligated to pay claims, with a reinsurer providing a financial backstop. Profits and control stay with the contractor.

How much profit do third-party warranty companies keep from plumbing warranties?

Frontdoor Inc. reported FY2025 gross margin of 55%, retaining approximately $0.55 of every premium dollar as gross profit. Adjusted EBITDA margin reached approximately 26%, representing operational profit after all costs. This is the margin a contractor could capture through reinsurance instead.