Introduction

Most HVAC contractors think about warranties in one of two ways: a manufacturer's paperwork obligation they hand off at install, or a third-party program they sign up for and forget. Neither approach is costing them sales today — but both are leaving serious money on the table.

The market has shifted. Homeowners aren't just comparing equipment brands and prices anymore. They're comparing what happens after the install, and warranty coverage has become one of the most visible signals they use to evaluate contractors before signing anything.

This article covers how strategic HVAC warranty programs help contractors:

- Close more jobs by standing out during the estimate stage

- Build lasting customer relationships through post-install touchpoints

- Generate real profit when the program is structured correctly — not just added cost

TLDR

- Homeowners treat warranty quality as a proxy for contractor confidence and workmanship standards.

- 75% of homeowners consider HVAC service agreements important, per a 2023 Clear Seas Research survey.

- Leading with strong warranty terms shifts the buyer conversation from price to value.

- Third-party warranty arrangements funnel underwriting profits away from the contractors who earned them.

- Contractor-owned reinsurance structures allow HVAC companies to capture those profits, control claims, and build recurring revenue.

Why HVAC Warranties Are Now a Competitive Differentiator

Before homeowners schedule an HVAC estimate, most have already done comparison research — on equipment brands, yes, but also on which contractors stand behind their work.

A 2023 Clear Seas Research survey reported by ACHR News found that 75% of homeowners consider HVAC service agreements important, with 18% calling them extremely important. That's a clear majority of buyers who are factoring protection into their decision — before they ever schedule an estimate.

The Real Differentiation Problem

Most contractors compete on three variables: price, brand, and reputation. The problem is those variables have converged. Equipment efficiency ratings are standardized across manufacturers. Pricing gravitates toward a market range. And reputation, while meaningful, is harder to convey in a 20-minute sales visit than a clear, documented warranty.

Warranty terms are concrete and readable — homeowners can pull two proposals and compare coverage line by line.

According to ACHR News, while most service-company owners believe they deliver great customer service, only 10% of customers agree. A documented warranty bridges that gap — it's verifiable proof of commitment, not a claim the contractor has to make about themselves.

The Silence Problem

Contractors who don't actively address warranty terms during the sales conversation create an unintended impression. To a homeowner comparing bids, vague or minimal warranty language reads as hesitation — as if the contractor isn't fully confident in the equipment or the installation.

The contractors winning those comparisons aren't necessarily cheaper or using better equipment. They've simply made it easy for the homeowner to feel protected — and that clarity is doing the selling for them.

What Homeowners Really Want from HVAC Warranty Coverage

A new HVAC system is a $6,000 to $12,000+ decision for most homeowners. The purchase anxiety doesn't end at installation — it shifts. Now they're wondering what happens if something goes wrong in year four. Or year nine.

The Coverage Gap Most Homeowners Don't Know Exists

Manufacturer warranties look comprehensive on paper. In practice, they often aren't. Trane's base limited warranty, for example, covers parts that fail due to manufacturer defects for five years — but not labor, shipping, or service calls. Registration within 60 days can extend parts coverage to 10 years, but labor remains the homeowner's responsibility throughout.

Lennox follows a similar structure: factory warranty covers parts only, with up to three years of labor coverage available upon registration.

Parts covered, labor exposed: that's where the surprise bills land. Contractors who walk homeowners through this distinction during the sales conversation build trust that competitors who skip the explanation simply can't match.

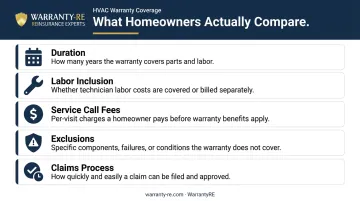

What Homeowners Actually Evaluate

The 2023 Clear Seas Research survey found that 80% of homeowners want parts discounts, 78% want labor discounts, and 77% want priority service as part of any service agreement. They want comprehensive protection, not just a manufacturer slip of paper.

Key elements homeowners compare when evaluating warranty coverage:

- Duration: Years of coverage matter — but only if both parts AND labor are included

- Labor inclusion: A parts-only warranty leaves the technician's time as the homeowner's bill

- Service call fees: Some agreements charge per visit even during the coverage window

- Exclusions: Filters, wiring, and consumables are common voids homeowners don't notice until they file a claim

- Claims process: Response time and who controls approval decisions matter as much as the coverage itself

The Credibility Signal

Strong warranty coverage communicates something that no sales pitch replicates: the contractor is confident enough in their work to stand behind it financially. That's unspoken proof — and competitors without equivalent coverage can't replicate it.

Beyond the initial sale, an active warranty relationship keeps the customer connected. Service visits, renewal conversations, and referral opportunities all follow. A homeowner under warranty has a reason to call you first — not search for someone else.

How a Strong Warranty Program Helps Contractors Close More Jobs

Changing the Decision Framework

When three contractors quote similar equipment at comparable prices, the one offering clearly superior warranty terms shifts the buyer's evaluation from "who is cheapest" to "who protects me best." That's a different conversation — and one where price pressure matters far less.

ACHR News data shows that the average HVAC installation close rate is 43%, rising to 52% when contractors offer four or more proposal options. Warranty tiers are a natural way to create those options without just discounting.

Making the Financial Case to Hesitant Buyers

Homeowners aren't irrational about cost — they're uncertain about future risk. Help them quantify that risk concretely:

| Component | Typical Repair Cost Without Coverage |

|---|---|

| AC compressor replacement | $800 – $2,300 |

| Furnace blower motor | $560 average (up to $2,400) |

| Furnace control board | $300 – $700 |

Source: Angi/HomeAdvisor 2025–2026 repair benchmarks.

Years 8–12 of a system's life are when these failures cluster. A compressor replacement in year nine isn't a freak event — it's a predictable category of exposure. Contractors who frame warranty coverage as converting that unpredictable future cost into a manageable, known line item are helping buyers make a rational decision, not selling them on something they don't need.

Justifying a Premium Price Point — and Building What Comes After

Comprehensive warranty coverage gives contractors room to hold margin. Buyers who understand what they're getting — genuine parts-and-labor protection with a contractor-controlled claims process — will often pay more for that certainty than they would for a cheaper bid with vague or minimal coverage.

That margin advantage extends well beyond the close. Warranty relationships don't end at contract signing — service visits, annual check-ins, and renewal conversations create consistent touchpoints with customers who already trust you. That's recurring workflow that requires no lead generation spend to produce, and it compounds into referral networks over time.

The revenue math is straightforward: industry benchmarks from Contracting Business put maintenance agreement renewal rates at 85%+ with 42%–45% gross margins. Contractors hitting those numbers have built warranty and maintenance into their core business model — not treated them as add-ons.

What Third-Party Warranties Are Actually Costing HVAC Contractors

Most HVAC contractors who offer extended warranties use third-party providers. That's better than no program, but it comes with a structural problem that's easy to miss until you look at the numbers.

The Profit Flow Problem

When a contractor sells a third-party warranty, the arrangement looks straightforward: contractor sells, contractor earns a portion of the premium, third-party provider handles claims. What the contractor doesn't see is the underwriting profit sitting in that premium after claims are paid.

As WarrantyRE puts it directly: "If your warranty company were not making a profit off of you selling their products, would they continue to do business with you?" That profit exists. It's generated by the contractor's customer base. Under a third-party arrangement, it flows to the provider — not the contractor.

Across hundreds of installations per year, that's a substantial amount of money contractors are giving away, often without realizing it.

The Control Problem

That financial drain compounds a second problem: control. Third-party warranty administrators own the claims process entirely. When a homeowner experiences a delayed approval, a denied claim, or a slow resolution, they don't call the warranty company. They call the contractor who installed the system.

The contractor absorbs the reputation hit for a process they had no authority over.

The Competitive Ceiling

Lost profits and reputational exposure are costly on their own. The third problem is strategic. Contractors locked into third-party programs can't differentiate their warranty product. They're limited to the terms, pricing, and service experience the provider offers — with no ability to improve coverage, adjust pricing, or build a program that reflects their own standards.

Without ownership, differentiation isn't possible. Any competitor offering the same third-party program can always undercut on price.

Contractor-Owned Warranty Reinsurance: The Next Level of Competitive Advantage

How the Structure Works

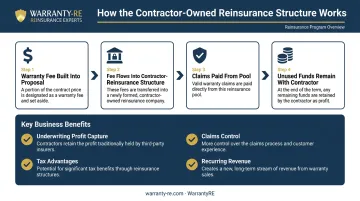

Contractor-owned warranty reinsurance is the alternative to handing that profit and control to a third party. Under this model, the HVAC contractor establishes their own administrator obligor reinsurance company — backed by A-rated insurers — that reinsures the labor warranties their business generates.

Here's how it works in practice:

- A warranty fee is built into every installation proposal.

- That fee flows into a reinsurance structure legally owned by the contractor.

- When warranty claims arise, they're covered from this pool.

- Unused funds remain with the contractor.

The A-rated insurer backing provides financial security and regulatory compliance. If the contractor's reinsurance company cannot meet its obligations, the direct writing insurance company carries the ultimate liability — limiting the contractor's exposure to formation costs and accumulated earnings.

The Business Benefits

Owning the program changes the financial structure of every installation:

- Captures underwriting profits that previously went to a third-party provider

- Controls the claims experience directly, protecting customer relationships and reputation

- Gains tax advantages on reinsurance contributions, keeping funds inside the contractor's own company structure rather than sending them to the IRS

- Converts each install into an ongoing financial relationship through recurring warranty fees

What WarrantyRE Handles

Setting up a contractor-owned reinsurance structure involves compliance, company formation, and ongoing administration — but contractors don't have to manage any of that themselves. WarrantyRE has helped business owners across home service industries, including HVAC, build and manage these programs since 1994.

Their full-service administration covers:

- All legal filings, tax returns, and renewals

- Claims adjudication from first call to final resolution

- Monthly financial statements and performance reporting

- Staff onboarding and training (online and in-person)

- Compliance management across state requirements

Contractors focus on installs. WarrantyRE runs the program. And the entry point is lower than most contractors expect — you don't need to be a high-volume operation to qualify. Smaller shops have built profitable reinsurance structures with WarrantyRE the same way larger ones have.

Frequently Asked Questions

What is the difference between a manufacturer's HVAC warranty and a contractor-backed warranty?

Manufacturer warranties typically cover parts only for a set term and require registration to activate full coverage — leaving labor, shipping, and service call costs as the homeowner's responsibility. Contractor-backed warranties can extend coverage to include labor, service visits, and longer durations, closing the gap that most homeowners don't know exists until they receive a repair bill.

How can offering extended warranties help HVAC contractors win more bids?

Superior warranty terms shift the buyer's focus from price comparison to value comparison, addressing the "what if it breaks?" concern before the homeowner raises it. Presenting coverage clearly during the initial quote positions contractors as advisors rather than commodity vendors — improving close rates and reducing price pressure on every bid.

Are there legal or compliance requirements for HVAC contractors offering extended warranties?

Most states regulate contractor-offered extended warranties and service contracts as quasi-insurance products, requiring registration, contract form approval, and in some cases reserve accounts or surety bonds. Requirements vary significantly by state, making qualified compliance guidance from a reinsurance partner essential before launching any program.

How do HVAC contractors make money from warranty programs?

Under a contractor-owned reinsurance structure, warranty fees collected on every installation flow into a reinsurance account the contractor owns. After claims are paid, the remaining underwriting profit stays with the contractor — rather than flowing to an external provider — while the structure also creates tax planning opportunities and recurring revenue that grows with each new installation.

What is contractor-owned warranty reinsurance, and how does it work?

Contractor-owned reinsurance means establishing an administrator obligor company — backed by A-rated insurers — that lets HVAC contractors administer their own warranty program, control the claims experience, and retain profits that third-party providers currently keep. WarrantyRE handles legal setup, compliance, and claims administration, so contractors can run the program without adding operational overhead.