The answer is obvious — and it points to something most contractors never consider. Every time a customer pays for a warranty or service agreement, a portion of that premium funds someone else's profit center. Not yours.

Most contractors treat insurance as a fixed cost: pay the premium, transfer the risk, move on. That's accurate for general liability and workers' comp. But warranty coverage works differently — and understanding why is the difference between being the customer and being the business that keeps the profits.

This article explains how insurance and reinsurance actually work, why the distinction matters for contractors and dealers, and how a contractor-owned reinsurance structure changes the financial equation entirely.

TL;DR

- Insurance transfers risk from a policyholder to an insurer in exchange for a premium. For the policyholder, it's a cost — not a revenue stream.

- Reinsurance is risk transfer between insurance companies; the original customer has no direct involvement.

- When contractors offer warranties through third-party providers, those providers collect and keep the underwriting profits.

- A contractor-owned reinsurance structure captures those profits, so the same customer premiums fund the contractor's own company instead.

- WarrantyRE has helped contractors and dealers build these structures for over 30 years.

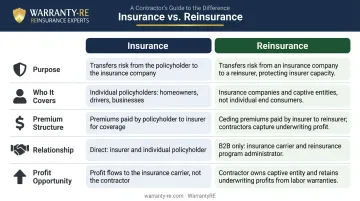

Insurance vs. Reinsurance: Quick Comparison

| Category | Insurance | Reinsurance |

|---|---|---|

| Purpose | Protects individuals or businesses against named losses | Protects insurance companies against excessive claims exposure |

| Who It Covers | End customers — homeowners, vehicle owners, businesses | The insurer (cedent) itself, not the original policyholder |

| Premium Structure | Fixed premiums paid directly by policyholders | Premiums expressed as a percentage of the cedent's premium base |

| Relationship | Insurer–policyholder, governed by consumer protection law | Business-to-business contract governed by general contract law |

| Profit Opportunity | Profits go to the insurer or warranty provider | Underwriting profits go to the reinsurance company owner — such as a contractor or dealer who sets up their own structure |

What Is Insurance?

Insurance reduces financial uncertainty by substituting a known, manageable premium for the risk of a much larger, unpredictable loss. The policyholder pays; the insurer assumes the exposure.

For contractors, this shows up in several essential forms:

- General liability — covers third-party bodily injury and property damage claims

- Workers' compensation — required in most states for contractors with employees (California's CSLB extended this requirement to roofing, HVAC, concrete, and tree service contractors regardless of employee count)

- Commercial auto — covers vehicles used in business operations

- Tools and equipment — protects job-site assets

These policies are necessary, non-negotiable operating expenses — not profit centers.

Where the Money Goes on Warranty

Standard insurance covers what goes wrong on the job. But when a contractor offers a warranty — say, a 2-year labor warranty on an HVAC installation or a 5-year workmanship guarantee on a roof — a different financial arrangement takes over.

That warranty is typically backed by a third-party provider or administrator. The customer pays a premium (often built into the project price), and the provider collects it, invests it, pays claims from it, and keeps what's left. The contractor carries the liability of standing behind the work while the warranty company captures the financial upside. Most contractors are in this arrangement without fully recognizing it.

What Is Reinsurance?

Reinsurance is a transaction in which an assuming insurer indemnifies a ceding insurer against all or part of the losses the ceding insurer may sustain under its policies. Simpler version: it's insurance for insurance companies.

The original policyholder — the homeowner, the car buyer — has no direct involvement in the reinsurance transaction. It operates entirely at the company level.

The Two Types That Matter Here

Proportional (Quota Share): Premiums and losses are split between the cedent and reinsurer by a fixed percentage. If the split is 70/30, the reinsurer takes 30% of premiums and covers 30% of losses.

Non-proportional (Excess of Loss): The reinsurer only pays when claims exceed a defined threshold. Below that threshold, the cedent absorbs losses. According to Swiss Re, excess of loss is the most common non-proportional form.

The Fronting Arrangement

A fronting arrangement is where a licensed, A-rated insurer issues the policy to the end customer, while a separate entity assumes the actual risk and retains the underwriting profits. IRMI defines fronting as the use of a licensed admitted insurer to issue a policy for a self-insured organization or captive, with risk retained through an indemnity or reinsurance agreement.

This is the foundation of contractor-owned reinsurance programs.

The Admin Obligor Model

In an admin obligor structure, the contractor or dealer establishes their own reinsurance company, backed by A-rated insurers, to assume the risk of their warranty products. The A-rated carrier handles regulatory compliance and serves as the backstop; the contractor's entity retains the premiums and, after claims are paid, the underwriting profit.

All funds flow into a trust account at a U.S. trust company. Withdrawals are restricted to four purposes:

- Covered claim payments

- Limited professional fees

- Income taxes

- Excess reserves (with the underwriting insurer's approval)

The contractor's liability is limited to their investment in the corporate structure, not unlimited exposure. WarrantyRE has been building and managing these structures for contractors and dealers since 1994.

One critical clarification: reinsurance doesn't eliminate risk. It redistributes it. In a contractor-owned model, the contractor accepts a defined, manageable level of claims exposure while retaining the premium income that funds those claims — and generates profit when claims come in below projections.

Key Differences Between Insurance and Reinsurance

Who Benefits Financially

In a standard warranty arrangement, the third-party provider collects premiums, invests them, pays claims, and keeps the remainder. The contractor delivers the work and shoulders the reputational risk. The provider captures the financial upside.

In a contractor-owned reinsurance structure, that dynamic reverses. The contractor's entity collects and holds the premiums. Claims get paid from those funds. Unused funds stay with the contractor.

Regulatory and Contractual Differences

Consumer insurance contracts are regulated by state insurance commissioners, follow standardized policy forms, and carry consumer protection obligations. Reinsurance contracts are business-to-business agreements governed by general contract law — more flexible in structure, but still requiring proper licensing, compliance, and administration.

One practical consequence: the original policyholder has no direct legal relationship with the reinsurer. A New York appellate court confirmed this principle — without a specific "cut-through" clause, an original insured cannot bring suit directly against reinsurers.

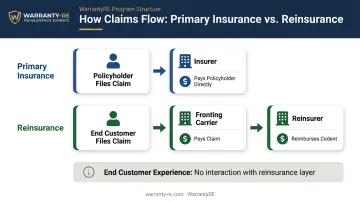

How Claims Actually Flow

In primary insurance, the insurer pays the policyholder directly. In reinsurance, the reinsurer reimburses the cedent (the fronting insurer) after the cedent has already paid the underlying claim. The end customer never interacts with the reinsurance layer — they deal with the contractor and the fronting carrier.

The practical flow looks like this:

- Primary insurance: Insurer pays the policyholder directly

- Reinsurance: Reinsurer reimburses the cedent after the cedent pays the underlying claim first

- End customer experience: No interaction with the reinsurance layer — they deal only with the contractor and fronting carrier

What This Means for a Contractor

Standard insurance is a risk management line item. A contractor-owned reinsurance structure is a business strategy. Those premiums still flow from the same customers — but now they build equity in a company the contractor owns, creating a second revenue stream alongside the core business.

How Contractors Can Turn Reinsurance Into a Profit Center

The Financial Logic

When a contractor sells a service agreement or warranty, the customer pays a premium — usually built into the project price. Under a third-party arrangement, most of that premium leaves the contractor's business permanently.

Under a contractor-owned reinsurance structure:

- The warranty fee is built into the contract price (the customer is already paying it)

- That fee flows into the contractor's reinsurance entity

- Claims are paid from the reinsurance pool

- Unused funds remain with the contractor as underwriting profit

WarrantyRE serves HVAC, roofing, plumbing, and electrical contractors, as well as auto dealers. The core structure stays consistent across trades while adapting to each industry's warranty profile. An HVAC contractor who builds a 2-year labor warranty into a $12,000 system replacement, for example, captures premium that would otherwise exit the business entirely.

Investment Income and Tax Planning

The trust company invests reserves in conservative government bonds, and that investment income belongs to the contractor's reinsurance entity. As the program matures and reserve balances exceed 125% of unearned premiums, investment flexibility increases.

The structure also carries tax planning implications through IRS Code 831(b), which allows qualifying property and casualty insurance companies to elect taxation on investment income only. These are areas where a qualified CPA and legal counsel should guide decisions — WarrantyRE coordinates with insurance tax specialists and legal counsel on behalf of clients to keep programs compliant and properly structured.

Risk Is Defined, Not Unlimited

Those tax and investment benefits come with a defined risk profile, not an open-ended one. The A-rated fronting insurer provides the financial backstop. If the contractor's reinsurance entity cannot meet its obligations, the ultimate liability rests with the direct writing insurance company. The contractor's exposure is limited to their corporate investment — not an open-ended claims liability.

What WarrantyRE Handles

WarrantyRE manages the full administrative layer so contractors can stay focused on their trade:

- Company formation and setup

- Licensing, legal filings, tax returns, and renewals

- Claims adjudication from first call to final resolution

- Monthly financial statements and performance reporting

- Ongoing compliance and program monitoring

- Staff onboarding and training (online and in person)

Contractors offering any warranty or service agreement are already generating reinsurance-style economics. The structure WarrantyRE provides simply routes those profits back to the contractor's own entity instead of a third party.

To find out what a contractor-owned structure could look like for your operation, contact WarrantyRE at (804) 824-9533 or request a free Owner Analysis consultation.

Frequently Asked Questions

What is the difference between insurance and reinsurance for contractors?

Insurance protects contractors against business risks like liability, property damage, and workers' comp claims. It's a cost of doing business. Reinsurance is a tool contractors can use to back their own warranty programs and capture the underwriting profits that third-party warranty providers currently keep. One costs money; the other can generate it.

What type of insurance does a contractor have?

Most contractors carry general liability, workers' compensation, commercial auto, and tools and equipment coverage. Contractors who offer warranties or service agreements may also work with warranty-backed products, which is where reinsurance enters the picture as a profit opportunity rather than just another expense.

Can a contractor own their own reinsurance company?

Yes. Through an admin obligor reinsurance structure, a contractor can establish their own reinsurance entity backed by A-rated insurers. The contractor owns 100% of the company, which reinsures only the business their own operation writes — and retains the underwriting profits from their warranty and service agreement programs.

How does warranty reinsurance work for home service businesses?

Warranty fees built into job pricing flow into the contractor's reinsurance entity instead of a third-party provider. The entity covers claims as they arise, and whatever remains after claims are paid becomes profit for the contractor. WarrantyRE handles administration, compliance, and financial reporting throughout.

What is the difference between a warranty and an insurance policy?

A warranty is a promise by the seller or contractor to repair or replace work within a defined period, tied directly to the transaction itself. An insurance policy is a regulated contract between an insurer and policyholder covering specified risks. Warranties can be backed by insurance or reinsurance structures, which is what makes the admin obligor model possible.

Is reinsurance regulated the same way as standard insurance?

Reinsurance contracts are generally governed by general contract law rather than consumer insurance regulations, since they're business-to-business arrangements. Contractor-owned reinsurance programs must still meet state licensing requirements, comply with IRS rules, and operate under proper administrative oversight — which is why working with an experienced program manager is essential to keeping the structure compliant and defensible.