Introduction

Most contractors and dealers put serious thought into which warranty products to offer and how to price them. The reinsurance structure sitting behind those products rarely gets the same attention — yet it's the structure that determines whether underwriting profits flow to a third-party provider or back to the business owner.

That gap is costly. When a contractor sells a labor warranty through a third-party program, the provider collects the premium reserve, manages claims, and keeps whatever's left over. The contractor gets a commission, maybe a small profit share, and no control over how the money is managed.

Reinsurance program structure design is the process of changing that arrangement — legally, contractually, and financially — so the owner captures those profits directly. The right design depends on program maturity, claims history, and business goals. The structural choices made at setup have a direct, lasting impact on profitability, tax planning, and how much wealth the business actually builds.

This article covers the main structural options available, explains how the admin obligor model works, and identifies the specific design decisions that most affect profitability, tax planning, and wealth accumulation.

TLDR

- Reinsurance structure determines who keeps underwriting profits — not warranty product selection

- Proportional structures suit newer programs; non-proportional works better for mature, stable ones

- The admin obligor model gives owners direct control over the premium reserve, investment income, and claims

- UPR funds earn investment income while held in trust; surplus beyond reserves is accessible to the owner

- Full-service administration covers compliance, claims, and reporting with no added workload on the contractor

What Reinsurance Program Structure Design Really Means

The Core Shift

In practical terms, program structure design refers to how risk, premium income, claims responsibility, and investment authority are legally and contractually arranged among the business owner, the fronting insurer, and any reinsurance entity the owner establishes.

The Insurance Information Institute describes reinsurance as "insurance for insurance companies" — and the same mechanics that large carriers use to manage exposure are available to contractor and dealer-owned programs.

In a traditional third-party warranty arrangement, the provider or insurer controls the premium reserve, manages claims, and retains any unused funds as profit. The contractor's role is passive: receive a commission, sell the product, and move on. The structural question is who sits in the position of the insurer.

Passive Participation vs. Active Ownership

The difference between these two positions determines who keeps the money:

- Passive participation — receiving a commission or small profit share from a third party. The reserve stays with the provider; claims decisions stay with the provider; profits stay with the provider.

- Active ownership — the business owner's reinsurance entity holds the unearned premium reserve (UPR), earns investment income on it between collection and claims payment, and retains surplus after claims are settled.

WarrantyRE puts it directly: if your warranty company weren't making a profit from you selling their products, would they continue doing business with you? The structure answers that question.

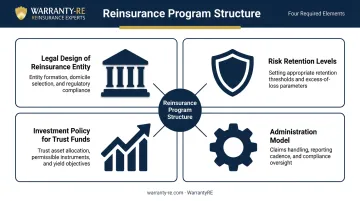

Four elements must align for the structure to work:

- Legal design of the reinsurance entity

- Risk retention levels appropriate to the program's size and loss history

- Investment policy for trust-held funds

- Administration model that maintains compliance without adding operational burden

Get these four right, and the warranty program stops being an overhead line item — it becomes a separate profit center with its own financials, its own reserves, and its own return.

The Main Structural Approaches: Proportional and Non-Proportional in Practice

Proportional Structures: Quota Share and Surplus Share

Proportional — or pro-rata — reinsurance means the fronting insurer cedes a defined percentage of both premiums and losses to the owner's reinsurance entity. The Reinsurance Association of America defines pro-rata reinsurance as an arrangement where the reinsurer shares a pro-rata portion of premiums and losses.

Two main variants apply in contractor and dealer programs:

Quota share — a fixed percentage of every warranty premium is ceded to the owner's reinsurance company. Income is stable and predictable regardless of individual claim variation. This is typically the starting point for newer programs because the economics are straightforward and the participation is immediate.

Surplus share — the owner retains liability up to a set threshold per contract and cedes only the excess. High-volume programs with lower-value contracts benefit most here, since the owner keeps more premium on contracts below the retention threshold. It rewards programs where individual claims are unlikely to exceed the retention threshold.

Non-Proportional Structures and Hybrid Designs

In a non-proportional (excess of loss) structure, the owner's entity retains all losses up to a defined retention, with the fronting insurer or another reinsurance layer covering losses above that threshold. Because the owner keeps all premium income rather than sharing it proportionally, this structure delivers higher net income when claims stay within retention.

The RAA also recognizes a combination plan — quota share paired with a per-risk excess of loss layer — as a single, industry-standard arrangement. This hybrid approach is often the most balanced design for growing contractor programs:

- The quota share foundation provides immediate, predictable premium participation

- The excess of loss layer protects net retention from outsized individual claims

- The owner benefits from premium income while limiting downside exposure

The right structure depends on where your program is in its development. Quota share gets you into the economics immediately; excess of loss becomes more powerful once you have the claims history to justify a higher retention and the premium volume to make it worthwhile.

The Admin Obligor Model: The Optimal Structure for Contractors and Dealers

How the Structure Works

In an admin obligor structure, the contractor or dealer forms their own reinsurance company. That entity acts as both administrator and obligor, meaning it holds financial responsibility for warranty claims.

A licensed, A-rated fronting insurer issues the warranty contracts to customers, satisfying state regulatory requirements, while contractually transferring the financial risk back to the owner's reinsurance entity in exchange for a fronting fee.

The NAIC Service Contracts Model Act defines an "administrator" as the person responsible for service contract administration and required filings, and a "provider" as the person contractually obligated to perform under a service contract. In the admin obligor model, the owner's entity fills both roles.

Why this matters over simpler participation models:

- The owner holds the reserve, not a third party

- Claims decisions flow through the owner's program

- Investment income on held premiums belongs to the owner's entity

- Surplus after claims are paid accumulates to the owner

The UPR and Surplus Account Mechanics

Premiums collected on each warranty contract flow into a trust held by the owner's reinsurance entity. Per NAIC Model Regulation 786, trust assets can include cash, certificates of deposit, and other permitted investments.

WarrantyRE structures these trust accounts with reserve funds invested conservatively — typically in government bonds — following restrictions set by the underwriting insurance company. Once balance sheet cash exceeds 125% of unearned premiums, excess funds may be invested more aggressively at the direction of the company ownership.

The financial progression works like this:

- Premium collected → flows into trust as UPR

- Investment income earned → belongs to the owner's reinsurance entity

- Claims paid → drawn from trust

- Remaining balance → moves to the surplus ("B") account as contracts expire

- Surplus funds → accessible to the owner with greater investment flexibility

A lower claims loss ratio means more surplus accumulates faster. That surplus is the primary wealth-building mechanism in the structure.

Claims Management and the Owner's Advantage

How quickly claims are resolved directly affects how fast surplus builds. When the owner's entity is financially responsible for claims, they have real oversight of what's being paid, why, and when — something a passive third-party arrangement never provides.

WarrantyRE handles all claims administration, from first call to final resolution, so contractors don't carry the operational burden. The benefit is a managed loss ratio backed by professional adjudication. Faster, accurate claims processing reduces open claims duration and the associated reserve requirements, which frees funds sooner.

Key Design Decisions That Drive Profitability

Three structural decisions have the most direct impact on how profitable a contractor-owned program becomes.

Retention Level Selection

Setting the retention threshold requires balancing two competing risks:

- Too low → the owner keeps less premium; much of the economics transfer to the reinsurance layer

- Too high → outsized individual claims can erode the trust balance significantly

Factors that should guide retention decisions:

- Average warranty contract value across the program

- Historical or projected loss ratio

- Total program volume (higher volume = more statistical stability at higher retentions)

- The owner's personal risk tolerance

- The capital position of the trust at program maturity

WarrantyRE provides business analysis as part of program setup to help owners set retention levels that reflect their actual program data, not generic assumptions.

Investment Policy for Trust Funds

The returns earned on premiums held in trust between collection and claims payment add real income to overall program performance. UPR funds must follow insurer and regulatory investment guidelines — conservative by design. Surplus funds offer more flexibility and can be directed by the owner once reserves are adequately funded.

Yield optimization matters more as the trust grows. Even modest improvement on a large, multi-year balance compounds into meaningful income over the life of the program.

Claims Administration Quality

Administration quality ties directly to financial performance — not just convenience. Under NAIC standards, claim reserves must reflect estimated ultimate settlement costs, meaning slow or inaccurate adjudication creates reserve requirements that tie up funds longer than necessary.

Programs where claims are adjudicated accurately and promptly carry lower reserve requirements relative to actual exposure. This is why WarrantyRE's full-service administration model directly affects program profitability.

Structuring for Tax Advantages and Long-Term Wealth

The Tax Planning Opportunity

Because the owner's reinsurance entity is a separate legal entity, premiums flow into it as business revenue. When claims are low and surplus accumulates, that growth can often be deferred from personal income until the owner chooses to access it.

Reinsurance companies with less than $2,900,000 in annual net premiums may elect taxation only on investment income under Internal Revenue Code Section 831(b), rather than on all underwriting income.

Critical caveat: IRS guidance requires genuine risk shifting and risk distribution for a structure to qualify as insurance for federal tax purposes. IRS Notice 2016-66 and IRS Notice 2025-24 flag certain micro-captive transactions as reportable or potentially abusive. Specific tax treatment depends on entity structure and individual circumstances. Qualified tax advisors should be consulted before making any decisions based on anticipated tax outcomes.

Strategic Uses for Accumulated Surplus

Business owners who build surplus in their reinsurance entity commonly direct those funds toward:

- Retirement income — drawing down accumulated surplus at retirement when income may be taxed at lower rates

- Business succession — funding buyouts or ownership transitions without external financing

- Deferred compensation — creating structured benefit vehicles for key employees

- Business capital — reinvesting in equipment, expansion, or acquisitions

A program that runs for 10 or 15 years with a well-managed loss ratio builds a meaningful asset inside the owner's entity — separate from the operating business. That asset belongs to the owner, not a third-party provider.

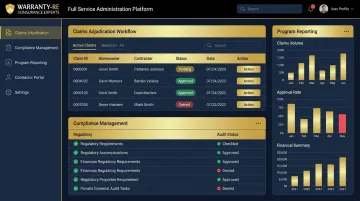

Full-Service Administration Removes the Burden

None of the wealth-building outcomes above happen automatically. Accurate financial reporting, compliance management, and tax return preparation are required to keep the structure functioning — and to keep it defensible.

WarrantyRE handles all of it, including:

- Monthly financial statements and bookkeeping

- Annual report preparation for tax advisors

- Legal forms, filings, and compliance management

- All tax returns and renewals

Contractors and dealers stay focused on their core business. WarrantyRE handles the operational complexity that makes the program work.

Frequently Asked Questions

What is an administrator obligor reinsurance structure?

In an admin obligor structure, the contractor or dealer owns a reinsurance company that takes on financial responsibility for paying warranty claims. A licensed, A-rated fronting insurer issues contracts to customers and handles regulatory requirements, while contractually transferring the actual financial risk back to the owner's entity — allowing the owner to retain underwriting profits while staying compliant.

How do I decide between a proportional and non-proportional reinsurance structure?

The right choice depends on program maturity, claims history, and risk tolerance. Quota share structures suit newer programs with predictable income sharing from day one. Non-proportional structures work better for mature programs with a stable loss ratio, where the owner wants to retain a larger share of premium income.

What is the unearned premium reserve and why does it matter?

The UPR is the portion of collected premiums held in trust to cover future claims under active warranty contracts. As contracts expire without claims, those premiums become earned surplus — which is the primary profit source in a contractor-owned reinsurance program. The faster claims stay below projections, the faster that reserve converts into distributable profit.

Can a contractor own more than one reinsurance company?

Yes. Some owners establish multiple entities to separate programs by product line, geographic market, or succession planning purpose. The right approach depends on your business objectives — work with qualified legal and tax advisors to design the structure that fits.

How does a fronting company relationship work in a contractor-owned warranty program?

The fronting insurer issues warranty contracts to customers and satisfies state regulatory requirements, then contractually transfers the financial risk to the contractor's reinsurance entity in exchange for a fronting fee. WarrantyRE uses A-rated insurer backing on all programs to protect both consumers and regulators.

What ongoing administration is needed to run a contractor-owned reinsurance program?

Core functions include claims adjudication, premium reporting, trust account management, compliance filings, and tax return preparation. WarrantyRE manages all of it — no adjusters to coordinate, no compliance burden on your team's day-to-day operations.