Introduction

Plumbing contractors work punishing hours, shoulder serious capital costs, and juggle complex logistics across multiple job sites daily. Yet when tax season arrives, many hand over far more to the IRS than necessary — not because they're doing anything wrong, but because they're missing deductions that are legally theirs to claim.

The plumbing trade creates a surprisingly wide tax landscape. Heavy equipment purchases, vehicle-dependent operations, multiple job sites, and licensing requirements all generate legitimate deductions most contractors never fully capture. The real gap isn't the tax code — it's knowing which expenses qualify and how to document them so they hold up.

This guide covers the core deductions every plumber should be claiming, the commonly overlooked ones that could save thousands, advanced strategies for growing businesses, and the documentation practices that keep you audit-ready year-round.

TL;DR

- Deduct vehicle expenses, tools and equipment, insurance premiums, labor costs, and marketing

- Commonly missed: home office deduction, work clothing and safety gear, continuing education, business meals

- Advanced strategies include S-Corp election, SEP-IRA contributions (up to $72,000 for 2026), Section 179 expensing, and the 20% QBI deduction

- Proper documentation—mileage logs, receipts, business-purpose notes—separates valid deductions from audit risks

- Year-round tax planning consistently outperforms end-of-year scrambles

Core Tax Deductions Every Plumbing Contractor Should Be Claiming

These deductions apply to nearly every plumbing business regardless of size or structure. Missing even one category can mean leaving thousands on the table annually.

Vehicle and Mileage Expenses

Two methods exist for deducting vehicle costs: the standard mileage rate and the actual expense method. For 2026, the IRS standard mileage rate is 72.5 cents per mile.

Plumbers driving heavy, tool-loaded trucks to multiple sites daily often benefit more from the actual expense method, which includes:

- Fuel and oil changes

- Repairs and maintenance

- Commercial vehicle insurance

- Depreciation

- Registration and licensing fees

Critical distinction: Driving from home to a fixed office location is commuting (not deductible). Driving between job sites, or from home to a customer location when you have no fixed office, is deductible business mileage.

Tools, Equipment, and Section 179

Section 179 allows you to deduct the full purchase price of qualifying equipment in the year you buy it rather than depreciating over multiple years. For 2026, the limit is $2,560,000, with a phase-out threshold of $4,090,000.

Qualifying purchases include:

- Drain machines and pipe threading equipment

- Inspection cameras and pipe locators

- Work vans and trucks

- Software and computer systems

- Hydro-jetting equipment

Strategic timing matters: Purchasing equipment in December versus January can shift a large deduction into the current tax year. 100% bonus depreciation was also restored for property acquired after January 19, 2025, allowing immediate full expensing of qualifying assets.

Insurance Premiums

Plumbing contractors can deduct premiums for business insurance policies, including:

- General liability insurance

- Commercial vehicle insurance

- Workers' compensation (required in most states)

- Inland marine insurance (covers tools and equipment in transit)

- Professional liability coverage

- Business property insurance

Self-employed health insurance deduction: If you're not eligible for coverage through a spouse's employer plan, you can deduct 100% of health, dental, and long-term care insurance premiums for yourself and your family as an above-the-line deduction.

Labor and Subcontractor Costs

Wages paid to employees—including benefits and the employer's share of payroll taxes—are fully deductible. Payments to subcontractors are also 100% deductible.

Compliance requirement: File Form 1099-NEC for any subcontractor paid $600 or more during the year. Missing this filing can jeopardize the deduction.

Marketing and Advertising Expenses

All legitimate marketing costs are fully deductible:

Digital marketing:

- Website hosting and maintenance

- SEO services and online advertising

- CRM software subscriptions

- Social media advertising

Traditional marketing:

- Truck wraps and vehicle graphics

- Door hangers and direct mail

- Yard signs and banners

- Local radio or print ads

Beyond marketing tools, any software subscription used exclusively for business operations—scheduling platforms, estimating software, accounting tools—is 100% deductible in the year paid.

Commonly Overlooked Deductions That Could Save Plumbers Thousands

Most plumbers nail the obvious deductions—tools, trucks, materials. These are the ones that slip through: legal, well-documented, and worth real money if you claim them.

Home Office Deduction

Many plumbers assume they can't claim a home office because most work happens at job sites. Not true. If you handle scheduling, invoicing, estimating, and customer calls from a dedicated home workspace, you qualify—even if you never meet customers there.

Two calculation methods:

- Simplified method: $5 per square foot, up to 300 square feet (maximum $1,500 deduction)

- Actual expense method: Deduct a percentage of mortgage interest, utilities, insurance, and repairs based on the square footage used exclusively for business

Key requirement: The space must be used regularly and exclusively for business. A kitchen table where you also eat dinner doesn't qualify. A garage workshop where you store tools and equipment, or a spare bedroom used only for paperwork, does.

Work Clothing and Safety Equipment

Clothing qualifies only when it meets two conditions: required for work AND unsuitable for everyday wear.

Deductible items:

- Steel-toed boots

- Chemical-resistant coveralls

- Hard hats and safety glasses

- Waterproof gear and gloves

- Uniforms with company logos

Regular jeans and plain t-shirts don't qualify, even if you only wear them for work. Logo uniforms and specialized safety gear do.

Continuing Education and Licensing Fees

Professional development expenses that maintain or improve your current plumbing skills are fully deductible:

- License renewal fees

- Required continuing education units (CEUs)

- OSHA safety certifications

- Trade association dues

- Industry conference registrations

Important limitation: Education that qualifies you for a new trade or profession is not deductible. Training that maintains or improves your existing plumbing skills is fully deductible.

Travel costs to attend qualifying training or trade shows—transportation, lodging, and 50% of meals—are also deductible.

Business Meals

Business meals with clients, general contractors, property managers, or suppliers are 50% deductible when there's a clear business discussion. The temporary 100% restaurant meal deduction expired December 31, 2022.

Required documentation:

- Who attended (names and business relationships)

- Business purpose of the meal

- Date and location

- Amount spent

Specificity matters: "Discussed 2026 commercial project pipeline with John Smith, ABC Property Management" passes IRS scrutiny. "Business meal" written alone does not.

Self-Employment Tax Deduction

Self-employed plumbers pay 15.3% self-employment tax on net earnings (12.4% Social Security + 2.9% Medicare) up to the wage base of $184,500 for 2026.

You can deduct 50% of that SE tax as an above-the-line deduction—reducing your adjusted gross income whether you itemize or not. It's one of the few deductions self-employed contractors get automatically, with no additional record-keeping required.

Advanced Tax Strategies for Growing Plumbing Businesses

These strategies move beyond basic deductions into structural tax planning for contractors generating consistent profit.

S-Corporation Election

Once elected as an S-Corp, you split business income into two categories:

- Reasonable salary (subject to payroll taxes: 15.3% total)

- Distributions (not subject to self-employment tax)

Example scenario: A plumber with $150,000 in net business income might take a $75,000 salary (subject to payroll taxes) and $75,000 in distributions (not subject to SE tax). This could save approximately $11,475 in self-employment tax ($75,000 × 15.3%).

Critical requirement: The IRS aggressively enforces "reasonable compensation" rules. You can't pay yourself $20,000 and take $130,000 in distributions. Your salary must reflect what you'd pay someone with your skills and responsibilities in your market. Court cases like David E. Watson, PC v. U.S. have upheld the IRS's authority to reclassify distributions as wages when salaries are artificially low.

Trade-offs to consider:

- Added payroll compliance and processing costs

- Increased bookkeeping requirements

- Need for professional guidance to set defensible salary levels

Retirement Account Contributions

Self-employed plumbers can make substantial tax-deductible retirement contributions:

SEP-IRA (2026):

- Maximum contribution: $72,000 or 25% of compensation, whichever is less

- Simplified administration

- Contributions are deductible and reduce taxable income dollar-for-dollar

Solo 401(k) (2026):

- Employee deferral: $24,500 (plus $8,000 catch-up if age 50+)

- Employer contribution: up to 25% of compensation

- Total combined limit: $72,000 (or $80,000 with catch-up)

- More complex administration but higher contribution potential

These contributions reduce both ordinary income tax and self-employment tax, creating immediate savings while building retirement security.

Qualified Business Income (QBI) Deduction

Plumbing contractors may deduct up to 20% of qualified business income under Section 199A. This is one of the largest single deductions available to pass-through entities.

Key advantage for plumbers: Plumbing is not classified as a Specified Service Trade or Business (SSTB), so the deduction is available at all income levels, subject only to W-2 wage and property limitations above income thresholds of $197,300 (single) or $394,600 (married filing jointly) for 2025.

A plumber with $150,000 in qualified business income could potentially deduct $30,000 (20% × $150,000), significantly reducing taxable income.

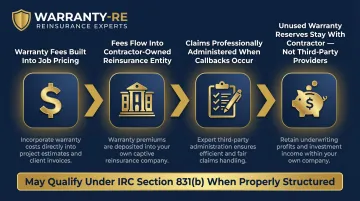

Owning Your Warranty Program as a Tax Strategy

Most plumbing contractors offer labor warranties on installations and service work, including water heater replacements, repiping jobs, fixture installations, and sewer line work. Typically, contractors either absorb callback costs directly or pay premiums to third-party warranty providers. Either way, that money leaves the business for good.

There's a third option: establishing your own reinsurance structure to capture warranty underwriting profits rather than paying them to external companies. Contractors who set up a properly structured reinsurance entity — as WarrantyRE helps plumbing contractors do — can deduct warranty-related contributions while retaining unused warranty reserves within their own company instead of handing them to a third party.

The mechanics work like this:

- Warranty fees are built into job pricing and flow into a contractor-owned reinsurance company

- When callbacks occur, claims are administered professionally

- Unused funds remain with the contractor's entity rather than enriching a third-party provider

- These structures can qualify for favorable tax treatment under IRC Section 831(b) when properly established

Important: This strategy requires professional legal and financial setup, comprehensive administration (claims handling, compliance management, tax filings), and consistent job volume to be viable. For established contractors, it's a legitimate way to retain warranty profits that would otherwise flow out of the business permanently.

How to Document Your Deductions and Stay Audit-Ready

The IRS doesn't disallow well-documented deductions—it disallows undocumented ones. The burden of proof always rests with you.

Minimum documentation standards by category:

Mileage

- Date of each trip

- Starting and ending locations

- Business purpose

- Odometer readings

Business Meals

- Receipt showing amount

- Names of attendees

- Business relationship and discussion topic

- Date and location

Home Office

- Square footage measurements

- Photos showing exclusive business use

- Records of home expenses (mortgage, utilities, insurance)

Equipment Purchases

- Receipts or invoices

- Proof of business use

- Section 179 election forms (if applicable)

Tracking what to document is only half the equation. These habits will keep your records defensible year-round:

Best practices:

- Open a dedicated business bank account and credit card — never mix personal and business expenses

- Capture expenses in real-time with accounting software rather than reconstructing records at tax time (the subscription fee is itself deductible)

- Store receipts digitally — the IRS accepts electronic records provided they're legible, complete, and accessible

- Keep records for at least three years, the standard IRS audit window (six years if you underreport income by more than 25%)

Conclusion

The plumbing trade creates a wide range of legitimate tax deductions—from daily vehicle expenses and equipment purchases to advanced structural strategies like S-Corp elections and retirement contributions. But only contractors who track expenses deliberately and plan proactively throughout the year capture them fully.

A $5,000 deduction you miss because you didn't log mileage or save receipts is $5,000 you can't claim. Multiply that across vehicle expenses, equipment purchases, home office use, continuing education, and business meals, and the annual cost of poor documentation can easily reach five figures.

Work with a tax professional who understands contractor businesses, especially before making entity structure decisions or large equipment purchases. The upfront investment in proper planning consistently pays for itself many times over.

Tax planning is one part of the financial picture. Some plumbing contractors take it further by building their own warranty programs—capturing underwriting profits that would otherwise flow to third-party providers—which compounds the gains from smart tax strategy. If you're interested in how reinsurance structures work for plumbing businesses, WarrantyRE offers owner analysis consultations to help you evaluate whether this approach fits your operation.

Frequently Asked Questions

What tax deductions can plumbing contractors write off?

Common deductions for plumbing contractors include:

- Vehicle expenses (standard mileage or actual costs)

- Tools and equipment (including Section 179 expensing)

- Insurance premiums and licensing fees

- Labor and subcontractor costs

- Home office expenses

- Work clothing, safety gear, and business meals

Self-employed plumbers report all of these on Schedule C.

What business expenses are 100% tax deductible?

Fully deductible expenses include:

- Tools and equipment

- Insurance premiums

- Advertising and marketing costs

- Licensing and permit fees

- Subcontractor payments

- Software subscriptions

Business meals are only 50% deductible. Vehicle deductions depend on whether you use the standard mileage rate or the actual expense method.

What is the $1,000 instant tax deduction?

This likely refers to the de minimis safe harbor — a rule that allows immediate expensing of items costing $2,500 or less per invoice or item for taxpayers without an applicable financial statement. Plumbers can use it to write off small tool purchases right away, skipping Section 179 elections and depreciation tracking.

How do you avoid the 22% tax bracket?

Maximizing deductions, contributing to a SEP-IRA or Solo 401(k) (up to $72,000 for 2026), and electing S-Corp status are the three most effective ways to reduce taxable income and stay in a lower bracket. A tax professional can model which combination works best for your income level.

Can plumbing contractors deduct the full cost of tools and equipment immediately?

Yes. Section 179 allows plumbers to deduct the full purchase price of qualifying tools, equipment, and vehicles in the year of purchase rather than depreciating over time. For 2026, the limit is $2,560,000. Additionally, 100% bonus depreciation was restored for property acquired after January 19, 2025.

Do I need receipts for every plumbing business deduction?

Yes. The IRS requires substantiation for all deductions—receipts, bank statements, or detailed mileage logs depending on the expense type. Digital records are acceptable and often easier to organize than paper files. The absence of documentation is the most common reason valid deductions are disallowed in audits.