Warranty programs change that math. Done right, they convert one-time installations into contracted, recurring revenue that builds on itself with each job. But there's a second problem hiding inside most warranty arrangements: every dollar a contractor sends to a third-party warranty provider is a dollar of underwriting profit leaving the business permanently.

This article covers five strategies for using warranty programs as a scaling engine — from building tiered offerings that lift close rates to owning the reinsurance structure that keeps underwriting profits inside your business.

TL;DR

- Warranty programs shift HVAC revenue from project-by-project income to predictable, contracted recurring revenue

- Tiered warranty plans increase both close rates and average job value simultaneously

- Third-party warranty providers keep all underwriting profit — a contractor-owned reinsurance structure captures that margin for you

- Customer retention, referral rates, and reduced liability are structural outcomes of a well-run warranty program

- Recurring warranty revenue commands a higher EBITDA multiple than project-based income, raising your business's overall valuation

Why Warranty Programs Are a Proven Lever for HVAC Business Growth

The Revenue Problem Most HVAC Contractors Share

HVAC businesses built on installations and break-fix calls share a structural problem: revenue is unpredictable. Peak season fills the schedule; shoulder seasons drain it. Cash flow swings make it hard to hire confidently, invest in equipment, or plan more than a quarter ahead.

The fix isn't working harder during peak. It's changing the underlying revenue model.

Industry benchmarks suggest service and maintenance should represent 25%-30% of total company sales for a well-structured HVAC contractor — and service agreement programs can operate at gross margins of 48%-50%, according to Contracting Business. That's a meaningful gap above typical project margins, and it compounds as your contracted customer base grows.

Contractors who build toward that mix run a fundamentally different kind of business:

- Payroll is covered by contracted agreements before a single install is booked

- Technicians stay productive in slow months instead of sitting idle

- The company generates predictable income year-round, not just during peak season

What Makes Warranty Programs Different from Standard Maintenance Plans

Maintenance plans and warranty programs are often mentioned in the same breath. They're not the same thing.

A maintenance plan schedules visits. A warranty program creates a defined coverage obligation tied to installed equipment, with your company as the named service provider for the life of that coverage. That distinction matters because:

- Warranty coverage locks in the customer relationship more durably than a visit schedule

- It ties future service calls, replacements, and referrals back to your business by contract

- It signals contractor confidence in the installed work — building trust, differentiating your sales pitch, and generating recurring revenue all at once

In practice, that means a homeowner with an active warranty doesn't shop around when something needs attention. They call you — because the contract says so, and because you've already earned the relationship.

Strategy 1: Build Recurring Revenue with Tiered HVAC Warranty Plans

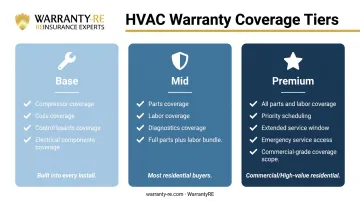

Designing the Three-Tier Structure

A tiered approach gives customers meaningful choices and nudges buyers toward mid-range and premium options. A practical structure looks like this:

| Tier | Coverage | Typical Use Case |

|---|---|---|

| Base | Key parts: compressor, coils, control boards, electrical components | Built into every install quote |

| Mid | Parts + labor + diagnostic coverage | Most residential buyers |

| Premium | All of the above + priority scheduling, longer coverage window, emergency service | Commercial or high-value residential |

The base tier should be incorporated directly into the installation quote — not offered afterward as an add-on. When coverage is part of the core proposal, it frames the value conversation from the start rather than feeling like an upsell at the end.

Pricing and Billing Structure

Regional cost of service, equipment brands, and coverage scope all affect the right price for your market — there's no universal benchmark. What research does confirm: the billing structure matters as much as the number itself.

- Monthly billing reduces friction and increases uptake — residential customers respond well to spreading cost over time

- Annual billing delivers faster cash flow and works better for commercial accounts that budget annually

- Leading with a monthly payment frame tends to result in higher-end equipment choices, not just higher close rates

The Revenue Math Behind a Contracted Customer Base

Get the billing structure right, and the revenue compounds fast. According to Contracting Business, each service agreement generates an average of $650 in recurring replacement revenue beyond the agreement itself — through maintenance-generated replacement and accessory leads that close at 80%+. That's before counting the agreement premium.

Scale that across several hundred active warranty customers and the math changes entirely. A contracted base means revenue that doesn't reset to zero when install volume drops.

Close Rate Impact of Offering Options

An ACCA and Farmington Consulting survey of more than 1,000 contractors found that contractors offering four or more options closed at 52% versus 42% for those presenting one or two choices. Only 10% of contractors currently present four or more options — meaning this is a competitive gap most markets haven't closed.

Tiered warranty plans create that multi-option structure naturally. Technicians present choices rather than a single price, customers self-select, and close rates improve without changing anything else about the sales conversation.

Strategy 2: Use Warranty Programs to Close More Deals and Lift Average Job Value

The Customer's Real Decision

When homeowners compare HVAC bids, they're not just comparing prices. They're managing risk: what happens if the system fails in July? What does a callback cost me? Who shows up?

A contractor who leads with comprehensive warranty coverage answers those questions before the customer asks them. That shifts the conversation from "who's cheapest" to "who's protecting me" — and on that question, a contractor with strong warranty terms wins more often than one without them.

Lead with Protection, Not Price

The "lead with protection" method means warranty terms appear in the initial quote, not as a line item added after the total is set. Specific language that works naturally in this context:

- "Every system we install includes a two-year labor warranty — here's what that covers and how to use it."

- "We offer three coverage levels. The base is included in every install. Here's what the mid and premium options add."

- "Other contractors will quote you manufacturer coverage. We stand behind the labor ourselves."

This framing positions warranty as a core part of the service — not a sales tactic. Customers respond by asking fewer price objections and more questions about coverage — which means you're already closing.

Premium Positioning and Per-Job Margin

Warranty inclusion lets you price installs above competitors who offer only manufacturer pass-through coverage. You're not more expensive — you're more protected. That distinction gives you a named, concrete reason for a higher price — one customers can understand and accept.

The downstream impact compounds quickly. Customers with active warranty coverage:

- Stay with you longer and generate replacement opportunities

- Refer at higher rates than one-time install customers

- Close on maintenance and service calls at rates that outpace cold leads significantly

Your best lead source isn't advertising — it's your existing warranty base.

Reducing Customer Acquisition Costs Over Time

Those high close rates from existing warranty customers point to a larger financial reality: retaining a customer costs far less than acquiring a new one. A warranty customer who returns for service, replacement, and referral generates revenue at a fraction of the marketing cost of a cold lead. That cost advantage compounds — every year your contracted base grows, your dependence on expensive cold acquisition shrinks.

Strategy 3: Replace Third-Party Warranty Costs with a Contractor-Owned Program

Where the Profit Goes Right Now

Every time an HVAC contractor uses a third-party warranty provider, the economics look like this:

- Customer pays for the warranty (built into the job price or as a separate charge)

- Premium flows to the third-party administrator

- Claims get paid from that pool

- Whatever's left — the underwriting profit — stays with the third party, not with you

Broad service-contract insurers target 10%-20% profit margins on the gap between premiums collected and claims paid, according to Warranty Week. Frontdoor, the largest consumer home service plan company, reported a 54% gross margin in 2024. Those numbers describe what the industry looks like when someone else owns the underwriting structure.

That profit isn't disappearing — it's going to a company you're funding with your own customers' money.

What a Contractor-Owned Reinsurance Program Looks Like

The alternative is an administrator obligor reinsurance structure. Here's how it works in plain terms:

- The contractor establishes their own reinsurance company (legally owned by them)

- A warranty fee is built into every installation quote — customers pay it as part of the job price

- That fee flows into the contractor's reinsurance account, not to an outside company

- Claims are paid from that account when warranty work arises

- Unused funds remain with the contractor as underwriting profit

- An A-rated insurer provides the backstop — if reserves are ever insufficient, the carrier covers the shortfall, limiting the contractor's exposure to formation costs plus accumulated earnings

Administration is handled externally, but the profits stay inside your business.

Where WarrantyRE Fits In

Running this structure requires infrastructure most HVAC businesses can't build internally: state-level compliance filings, claims adjudication, Form 1120PC tax returns, multi-market licensing, and monthly financial reporting.

WarrantyRE, founded in 1994 by Tim Byrd in Southeast Virginia, provides that infrastructure as a full-service administrator. Contractors own their reinsurance company and keep 100% of the underwriting profits. WarrantyRE handles:

- Claims management from first call to final resolution

- All legal forms, filings, tax returns, and renewals

- Monthly financial statements and performance reporting

- Compliance and licensing coordination across all operating states

- Staff onboarding and training (online and in-person)

One point worth clarifying: you don't need to be large-volume to qualify. Programs are designed to scale with business size, and setup costs are typically offset by recaptured underwriting profits as the program builds.

The Compounding Advantage

A contractor-owned reinsurance program grows proportionally to install volume. More systems warranted means more premium flowing into the contractor's own account. That compounding effect — underwriting profit on top of install revenue, growing with each job — is structurally unavailable through any third-party arrangement.

There's a second compounding mechanism: premiums held in reserve can be invested — initially in conservative government instruments, then into higher-yield instruments once reserves exceed 125% of unearned premiums. That investment income belongs to the contractor's reinsurance company, not to a third party.

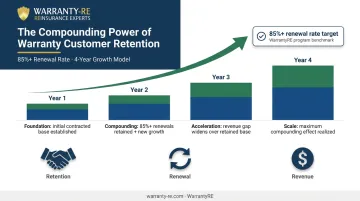

Strategy 4: Strengthen Customer Retention and Reduce Business Liability

Retention as a Revenue Strategy

Customers with active warranty coverage have a functional reason to stay with the contractor who issued it. Service calls, warranty repairs, and eventual equipment replacement all flow back to the same business — by contract.

Industry benchmarks target an 85%+ renewal rate for service agreements, according to Contracting Business. That retention rate, compounded over years, creates a customer base that generates revenue without marketing spend. Each warranty customer in your portfolio is a long-term revenue relationship, not a closed transaction.

Converting Liability into a Managed Obligation

Informal warranty promises create open-ended financial exposure. A verbal "we'll take care of it" or a loosely worded labor guarantee means callbacks are funded from operating cash — unpredictable, unbudgeted, and margin-eroding.

A properly structured, adequately funded warranty program converts that exposure into a defined, administrated obligation:

- Claims are adjudicated through a structured process

- Financial reserves back every coverage commitment

- Unexpected claim volume doesn't hit operating cash directly

- The contractor's liability is known and contained

That's not just better financially — it makes warranty promises credible to customers, which strengthens the sales case for premium coverage options.

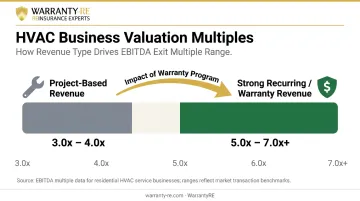

Business Valuation Impact

HVAC businesses with meaningful recurring contracted revenue are valued differently than project-based businesses at exit. M&A advisors place HVAC company valuations at 3.0x to 7.0x+ EBITDA depending on company size, recurring revenue quality, and margin durability, according to Auxo Capital Advisors. Businesses with strong maintenance agreement and warranty revenue portfolios trend toward the higher end of that range.

A well-structured warranty program builds contracted recurring revenue that a future buyer will pay a premium for. That's an asset worth building now, regardless of when — or whether — you plan to sell.

Frequently Asked Questions

How do I scale my HVAC business?

Scaling requires moving beyond one-off installs toward recurring revenue. Warranty programs and service agreements generate contracted income from every system installed — income that grows with your customer base instead of resetting each season. The result is a business that builds financial momentum rather than starting from zero every spring.

What is the difference between a third-party HVAC warranty and a contractor-owned warranty program?

In a third-party arrangement, the provider collects premiums and keeps the underwriting profit — the gap between premiums collected and claims paid. In a contractor-owned reinsurance program, the contractor establishes their own entity, retains those margins, and has an A-rated insurer provide the financial backstop.

How do HVAC warranty programs generate recurring revenue for contractors?

Customers pay warranty premiums as part of their installation price. Those premiums fund the contractor's warranty program. When the contractor owns the structure, the difference between premiums collected and claims paid becomes ongoing profit — rather than funding a third party's bottom line.

Can a small HVAC contractor afford to start their own warranty reinsurance program?

Reinsurance programs scale with business size, and setup costs are offset by the underwriting profits contractors begin recapturing right away. Full-service administrators like WarrantyRE handle setup and compliance, so contractors don't need in-house expertise or high volume to get started.

How do warranty programs affect HVAC business valuation when it comes time to sell?

Businesses with recurring contracted revenue — including warranty agreements — typically command higher EBITDA multiples than project-based competitors. A strong warranty program can shift a business from a 3x to a 5x multiple, making it one of the highest-leverage investments an HVAC owner can make before a sale.

What compliance requirements do HVAC contractors need to understand before offering warranty products?

Warranty products are regulated at the state level and may require service contract licensing, specific contract language, and regular state filings. Working with a program administrator that manages compliance on your behalf is the practical path forward. Navigating state-by-state requirements independently exposes contractors to real legal and financial liability.