That's real money left behind.

This guide is written for roofing contractors operating as self-employed business owners — sole proprietors, LLCs, and S-Corps. If you're a homeowner wondering whether your new roof is deductible, that's a separate question entirely (the short answer: generally not as a direct deduction).

What follows covers how contractor deductions work, the most valuable categories to claim, Section 179 and depreciation strategies, insurance and warranty program deductions, commonly missed write-offs, and the recordkeeping practices that protect every deduction if the IRS ever comes knocking.

TLDR

- Self-employed roofing contractors deduct ordinary and necessary business expenses on Schedule C or their business return to reduce taxable income.

- Top deduction categories: vehicles, equipment, subcontractor labor, insurance, tools, marketing, and professional services.

- Use Section 179 to immediately expense qualifying equipment and vehicles instead of depreciating them over several years.

- Don't overlook PPE, licensing fees, cell phone usage, surety bonds, and continuing education — these deductions are routinely missed.

- Keep receipts, mileage logs, and categorized expenses — clean records are what make deductions stick at audit.

How Roofing Contractor Tax Deductions Work

The foundation of every business deduction is the "ordinary and necessary" standard under IRC Section 162. The IRS defines ordinary as common and accepted in your industry, and necessary as helpful and appropriate for your trade (not indispensable, just useful). For roofing contractors, that covers a wide range of expenses from nails to nail guns to liability insurance.

Deductions and credits work differently. A deduction reduces the income subject to tax. A credit reduces your actual tax bill dollar-for-dollar. Roofing contractors benefit primarily from deductions, though certain energy-related credits may apply in specific scenarios.

Which Form You File Depends on Your Entity

| Entity Type | Tax Form |

|---|---|

| Sole Proprietor | Schedule C (Form 1040) |

| S-Corporation | Form 1120-S |

| Partnership / Multi-Member LLC | Form 1065 |

The categories of deductible expenses are largely the same across structures, but the filing mechanics differ. Work with a CPA who knows contractor businesses — the nuances matter.

Understanding those mechanics is useful, but the bigger opportunity is knowing how many deduction categories are actually available to you.

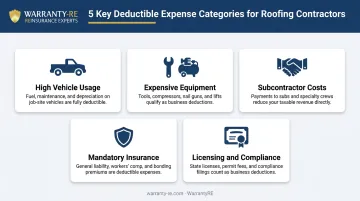

Why Roofing Businesses Have a Strong Deduction Base

Few small business types have as many deductible expense categories as roofing contractors:

- High vehicle usage — trucks running daily to job sites

- Expensive equipment — trailers, compressors, generators, ladders

- Substantial subcontractor costs — often the largest single expense line

- Mandatory insurance — general liability, workers' comp, commercial auto

- Ongoing licensing and compliance — state licenses, permits, safety certifications

That's a wide deductible base. The sections below break down each category so you know exactly what to track — and what to bring to your CPA.

Everyday Business Deductions Every Roofing Contractor Should Claim

Advertising and Marketing

Every dollar spent marketing your roofing business is fully deductible. That includes:

- Website development and hosting

- Google Ads and social media advertising

- Yard signs and door hangers

- Truck wraps used for business branding

- Business cards and direct mail

- Industry sponsorships

One limit to know: client gifts are only deductible up to $25 per recipient per year, per IRS Publication 463.

Contract Labor and Subcontractors

Payments to subcontractors for roofing labor are deductible — but you must issue a Form 1099-NEC to any unincorporated subcontractor paid $600 or more in a tax year, due by January 31.

Worker classification is a separate issue the IRS takes seriously. Misclassifying an employee as an independent contractor creates significant liability. If you're unsure about a worker's status, review the IRS's behavioral control, financial control, and relationship-of-the-parties test before tax season.

Employee Wages and Payroll Taxes

If you have W-2 employees, their gross wages, salaries, bonuses, and commissions are all deductible. So is the employer's share of FICA payroll taxes. Owners' draws or guaranteed payments are handled differently depending on your entity structure — which is why your entity structure should be reviewed with a CPA who understands contractor businesses.

Office, Software, and Administrative Expenses

Beyond payroll, your day-to-day operational costs are largely deductible too:

- Estimating software, CRM platforms, and project management tools

- Office supplies and postage

- Rent for a commercial office or storage yard

- Home office deduction if you use a dedicated space exclusively for business

For the home office, you have two calculation options: the simplified method ($5 per square foot, up to 300 sq ft) or the actual-cost method. The actual-cost method lets you deduct a proportional share of mortgage interest, utilities, repairs, and depreciation based on the percentage of your home used for business.

Travel, Meals, and Professional Development

- Business travel to job sites, supplier locations, or industry events is fully deductible — transportation, lodging, and related costs

- Daily commuting is not deductible

- Meals with a direct business purpose are deductible at 50%

- Continuing education courses, trade association memberships, and licensing renewal fees are fully deductible

Equipment, Vehicles, and Section 179

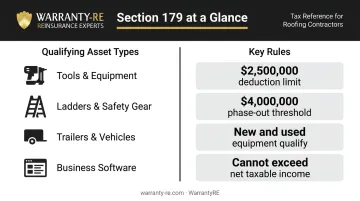

Section 179: Immediate Expensing for Roofing Equipment

Instead of depreciating equipment over several years, Section 179 lets you deduct the full purchase price of qualifying assets in the year you place them in service.

For tax years beginning in 2025, the Section 179 deduction limit is $2,500,000, with the deduction phasing out dollar-for-dollar once purchases exceed $4,000,000 (fully eliminated at $6,500,000), according to IRS Publication 946.

Qualifying assets for roofing contractors include:

- Nail guns, compressors, and generators

- Ladders, scaffolding, and safety harnesses

- Trailers and job-site equipment

- Off-the-shelf business software

Both new and used equipment qualify, as long as it's new to your business and placed in service during the tax year. One important ceiling: the Section 179 deduction cannot exceed your business's net taxable income.

Bonus Depreciation

Bonus depreciation complements Section 179 by allowing an additional first-year deduction on qualifying assets. For property placed in service after December 31, 2024 and before January 1, 2026, the rate is 40% under current tax law (with certain exceptions allowing up to 100% for property acquired and placed in service after January 19, 2025).

Unlike Section 179, bonus depreciation can create a net operating loss, which can then be carried forward to offset future taxable income. That makes it a useful planning tool in lower-revenue years.

Vehicle and Truck Deductions

Two IRS-approved methods exist for deducting vehicle costs:

| Method | How It Works |

|---|---|

| Standard Mileage Rate | Deduct the IRS-published cents-per-mile rate for business use (confirm current rate at IRS.gov) |

| Actual Expense Method | Track and deduct gas, oil, insurance, maintenance, and depreciation |

Vehicles used for both business and personal purposes require a mileage log documenting the date, destination, miles, and business purpose of every trip.

Heavy trucks and vans over 6,000 lbs GVWR used for business may qualify for Section 179 or accelerated depreciation — making purchase timing worth planning carefully. Parking fees, tolls, and trailer rental costs are deductible separately under either method.

Insurance Premiums, Warranty Programs, and Professional Services

Business insurance premiums are fully deductible as ordinary business expenses. For roofing contractors, these can represent one of the largest deductible line items on the return:

- General liability insurance

- Workers' compensation insurance

- Commercial auto insurance

- Tool and equipment coverage

Contractor-Owned Warranty Reinsurance as a Tax Planning Strategy

Roofing contractors who write a high volume of jobs have another option worth knowing about: owning their own warranty reinsurance company.

WarrantyRE, a reinsurance program administrator serving contractors since 1994, helps roofing contractors establish their own administrator obligor reinsurance company — a separate corporate entity legally owned by the contractor. Here's how it works:

- A warranty fee built into each job's contract price flows into the contractor's own reinsurance account

- Claims are paid directly from that account

- Any funds not used for claims stay with the contractor

The structure operates under IRC Section 831(b), which allows qualifying property and casualty insurance companies with less than $2,900,000 in annual net premiums to elect to be taxed only on investment income.

Contributions to the reinsurance account carry significant tax advantages — roofing contractors writing large tax checks each year are, in effect, pre-paying money that could be working inside this structure instead.

This is an advanced structure — evaluate it with both a tax advisor and a reinsurance specialist before moving forward. WarrantyRE manages all legal forms, filings, and tax returns for the reinsurance entity, and works alongside CPAs and legal counsel to ensure compliance.

Professional Service Fees

Accounting fees, CPA tax preparation fees, attorney fees for contract review, and business consulting fees are all deductible as legal and professional services. A CPA who specializes in contractor businesses typically saves far more than their fee — and that fee is itself deductible.

Tax Deductions Roofing Contractors Commonly Miss

These are legitimate deductions that often go unclaimed simply because they're not top of mind at tax time:

Safety and PPE: Hard hats, fall protection harnesses, safety glasses, gloves, and steel-toed boots are all deductible business supplies. OSHA mandates fall protection for roofing work at 6 feet or more, making those purchases a clear business expense — yet many contractors lump PPE into materials and lose the deduction entirely.

Business phone and utilities: If a cell phone is used 80% for business, 80% of the bill is deductible. A dedicated business landline, office internet connection, and utilities for a commercial shop or storage yard are fully deductible.

Licensing, permits, and bonding: State contractor license fees, local business license renewals, routine permit-pulling fees, and surety bond premiums are all deductible business expenses.

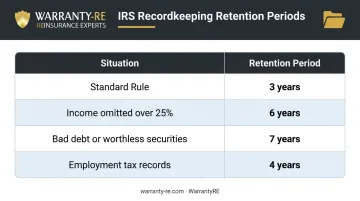

Record-Keeping Best Practices to Protect Your Deductions

The IRS requires adequate records to substantiate every deduction. In an audit, undocumented deductions get disallowed — no exceptions.

What to Keep

- Itemized receipts for all expenses

- A mileage log with date, destination, miles, and business purpose for every trip

- Bank statements and credit card records organized by expense category

- Copies of all 1099-NECs issued to subcontractors

- Documentation for all asset purchases and placed-in-service dates

How Long to Keep It

| Situation | Retention Period |

|---|---|

| Standard rule | 3 years from filing date |

| Income omitted exceeds 25% of gross income | 6 years |

| Bad debt or worthless securities claim | 7 years |

| Employment tax records | 4 years after tax due or paid |

Source: IRS recordkeeping guidance

Keep business and personal finances completely separate. Dedicated business bank accounts and credit cards make this straightforward and give you a clean paper trail if questions arise. Accounting software that categorizes expenses throughout the year saves significant time and prevents last-minute reconstruction come tax time.

Frequently Asked Questions

Is re-roofing tax-deductible?

For homeowners, replacing a roof is generally treated as a capital improvement added to the home's cost basis — not a direct deduction. For roofing contractors, the costs of running the business (labor, equipment, vehicles, insurance) are deductible as ordinary and necessary business expenses.

Can roofing contractors deduct vehicle and truck expenses?

Yes. Trucks and vehicles used for business are deductible using either the IRS standard mileage rate (72.5 cents per mile for 2026) or the actual expense method. Heavy vehicles over 6,000 lbs GVWR may also qualify for Section 179. Keep a mileage log to document the business-use percentage for any method you choose.

What is Section 179 and how does it benefit roofing contractors?

Section 179 lets roofing contractors deduct the full purchase cost of qualifying equipment and vehicles in the year bought, rather than depreciating it over time. The 2025 deduction limit is $2,500,000 — particularly useful in years when major equipment investments are made.

Are roofing tools and safety equipment tax deductible?

Hand tools, power tools, ladders, compressors, and OSHA-required PPE are all deductible. Smaller items used within a year are expensed as supplies; larger assets with a longer useful life are depreciated or expensed under Section 179.

Can roofing contractors deduct workers' compensation and liability insurance?

Yes. Workers' compensation premiums, general liability insurance, commercial auto insurance, and other business insurance costs are fully deductible as ordinary and necessary business expenses — typically among the largest deductible line items for roofing contractors.

What records do roofing contractors need to keep for tax deductions?

Keep itemized receipts, a mileage log for all business vehicle trips, bank and credit card statements, copies of 1099s issued to subcontractors, and records of asset purchases. The IRS recommends retaining business records for three years on standard returns and up to seven years if income was significantly underreported.