The right extended warranty partner determines whether warranty profits stay within your business or flow to an outside administrator. Understanding the differences between program types—third-party administrator models versus contractor-owned reinsurance structures—directly impacts your bottom line and long-term business equity.

TL;DR

- HVAC warranty programs range from TPA partnerships (you earn commission) to contractor-owned reinsurance models (you keep underwriting profits)

- Strong programs deliver transparent claims handling, fair coverage terms, and a clear profit-sharing or ownership structure

- Key evaluation factors: claims administration, profit distribution, setup complexity, compliance support, and coverage quality

- Contractor-owned models like WarrantyRE let you replace third-party providers entirely and retain 100% of underwriting profits

- Match your choice to your install volume, claims bandwidth, and growth goals

What Are HVAC Extended Warranty Programs for Contractors?

From a contractor's perspective, HVAC extended warranty programs are service agreements or extended coverage products you sell to customers at installation or during maintenance visits. They cover parts, labor, or both beyond the manufacturer's standard warranty window—and they represent a strategic revenue stream on top of customer protection.

Two primary program structures exist:

- Third-party administrator (TPA) models — A warranty company handles underwriting, claims, and compliance while you earn a commission or flat fee per contract sold

- Contractor-owned or reinsurance models — You establish your own administrator-obligor structure backed by A-rated insurers, keeping the underwriting profit

This choice directly shapes your long-term profitability and business equity. In TPA models, the warranty company holds the "float"—premiums invested between collection and claims payout. In reinsurance models, that float stays with you.

Understanding which structure fits your business is the first step. The companies evaluated below were selected with that distinction in mind—assessed on profit structure, claims quality, setup requirements, compliance support, and contractor-friendliness.

Best HVAC Extended Warranty Companies for Contractors

The following companies were assessed on their value to HVAC contractors as business tools—not on consumer-facing ratings. Evaluation focused on profit structure, claims administration, compliance support, and contractor control.

WarrantyRE

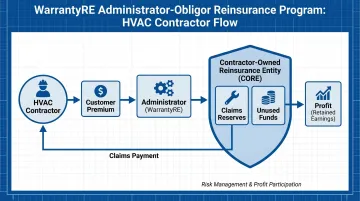

Founded in 1994 in Southeast Virginia, WarrantyRE has over 30 years of experience helping contractors and dealers establish administrator-obligor reinsurance companies. Serving 400+ clients nationwide across HVAC, roofing, plumbing, and electrical trades, the company has roots in the auto dealership F&I space where the reinsurance model proved highly profitable.

Instead of partnering with a third-party warranty company and earning commissions, you work with WarrantyRE to create your own warranty company backed by A-rated insurers. Premiums customers pay fund your own reinsurance entity — so you capture underwriting profits, control the claims experience, and build a tax-advantaged asset.

Services include:

- Complete company setup and compliance

- Claims adjudication and administration

- Bookkeeping and performance reporting

- Staff training and sales enablement

- All legal forms, filings, and tax returns

- Ongoing regulatory compliance management

Warranty fees are built into your installation pricing. When a homeowner buys a $12,000 HVAC system with a 2-year labor warranty, that fee flows into your reinsurance account — not to a third party. When claims occur, WarrantyRE administers them from your funded reserve. Unused funds remain yours, generating investment returns and building equity.

| Factor | Details |

|---|---|

| Program Type | Admin Obligor Reinsurance (Contractor-Owned) |

| Profit Model | Contractor captures 100% of underwriting profits; premiums invested for additional ROI |

| Claims & Administration | Full-service by WarrantyRE: claims adjudication, compliance, filings, tax returns, renewals |

| Coverage Focus | Labor warranties on furnace, AC, heat pump, and mini split installations |

| Minimum Volume | No minimum install requirements—available to contractors of all sizes |

Warrantech (AmTrust Financial Services)

Warrantech, operating under AmTrust Financial Services, has historically been one of North America's largest third-party extended warranty administrators. AmTrust Financial carries an A- (Excellent) AM Best rating, manages $8.8 billion in gross written premiums, and oversees 55 million active contracts across 55 countries.

Warrantech's website now focuses primarily on vehicle service contracts. AmTrust's HVAC-adjacent offerings operate through its Home Protection division and OEM partnerships (such as Rheem Protection Plus) — not as standalone contractor-facing programs under the Warrantech brand.

Warrantech/AmTrust operates as a traditional TPA model: contractors earn commission or per-contract fees, while the administrator retains underwriting profits. Specific commission structures and contractor margin details are not publicly disclosed.

| Factor | Details |

|---|---|

| Program Type | Third-Party Administrator (TPA)—Contractor earns commission |

| Profit Model | Revenue share or per-contract fee; underwriting profit retained by administrator |

| Claims & Administration | Handled by Warrantech/AmTrust; contractor has limited claims control |

| Coverage Focus | OEM partnerships and home protection plans |

Residential Warranty Company (RWC)

RWC provides insurance-backed structural warranties for new home construction, following the "1-2-10" model: Year 1 covers workmanship, Year 2 covers distribution systems (plumbing, electrical, HVAC), and Years 3-10 cover major structural defects.

RWC serves builders, not independent HVAC contractors. Their membership model requires conformance to RWC Warranty Standards. The Enhanced Warranty covering HVAC (offered through the Key Estates affiliate) is sold to builders as an add-on — not to HVAC contractors as a standalone program.

RWC's relevance is limited to contractors performing work under builder warranty programs — it is not a commission-per-contract option for independent HVAC contractors.

| Factor | Details |

|---|---|

| Program Type | Builder warranty provider (not contractor-facing) |

| Profit Model | Membership-based; not applicable to independent HVAC contractors |

| Claims & Administration | Managed by RWC for builder members |

| Coverage Focus | New construction structural and system warranties |

Safehold Special Risk

Safehold Special Risk was a specialty warranty and service contract program administrator. As of November 2025, Safehold combined operations with U.S. Risk under the new brand Innovation Growth Partners Specialty, LLC (IGP Specialty).

Neither Safehold Special Risk nor its successor IGP Specialty offers contractor-facing HVAC warranty programs. Their programs cover Builder's Risk and specialty commercial insurance — not residential HVAC service contracts.

| Factor | Details |

|---|---|

| Program Type | Specialty insurance (not HVAC contractor-focused) |

| Profit Model | Not applicable—no active HVAC contractor programs identified |

| Claims & Administration | N/A |

| Coverage Focus | Commercial specialty insurance |

American Home Shield PRO (Contractor Network Program)

American Home Shield operates under Frontdoor, Inc., which manages multiple home warranty brands including AHS, HSA Home Warranty, 2-10 Home Buyers Warranty, Landmark Home Warranty, and OneGuard. Contractors apply through a unified Frontdoor contractor portal.

The AHS contractor program is a service fulfillment/dispatch model, not a warranty sales channel. Contractors fulfill service calls at pre-negotiated rates — they do not sell warranties or build equity.

The dispatch process works as follows:

- Contractors receive dispatched service calls from AHS warranty holders

- Diagnose issues and submit for authorization before performing covered work

- Collect the homeowner's Trade Service Call (TSC) fee at time of visit

- Receive pre-negotiated flat or hourly labor rates for covered work

Key limitations for contractors:

- No co-branding or private-label options

- No control over warranty pricing or claims adjudication

- No underwriting profit participation

- Authorization required for expensive repairs before proceeding

- Contractor brand identity subordinate to AHS brand

Insurance Requirements: $500,000 general liability, workers' comp, $250,000/$500,000 auto insurance, $100,000 property damage insurance.

| Factor | Details |

|---|---|

| Program Type | Contractor Service Network/Dispatch Fulfillment |

| Profit Model | Per-claim labor rate; no warranty sales commission or underwriting profit |

| Claims & Administration | Administered by AHS; contractor serves as labor fulfillment with limited autonomy |

| Coverage Focus | Home warranty claims fulfillment only |

What Contractors Should Look for in an Extended Warranty Partner

The most common mistake HVAC contractors make is treating warranty program selection like a consumer purchase — focusing only on customer coverage rather than evaluating the full business impact on revenue, brand, and liability exposure. Four criteria separate programs that generate long-term profit from those that simply shift cost: profit structure, claims control, compliance support, and sales enablement.

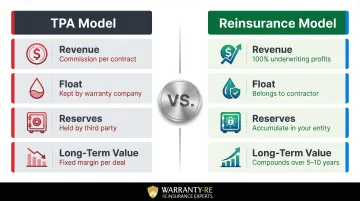

Profit Structure: Who Keeps the Underwriting Income?

The difference between earning a flat commission per contract and owning the underwriting entity can represent hundreds of thousands of dollars over a contractor's lifetime.

| TPA Model | Reinsurance Model | |

|---|---|---|

| Revenue | Commission or spread per contract | 100% of underwriting profits |

| Float | Warranty company keeps it | Belongs to you |

| Reserves | Held by third party | Accumulate in your entity |

| Long-Term Value | Fixed margin per deal | Compounds over 5-10 years |

For a contractor doing 200+ installs annually, the reinsurance model's reserve accumulation and investment income create a material financial advantage that the TPA model can't match.

Service agreement revenue yields 40-55% gross margins versus 18-25% on transactional emergency calls — a 42% margin improvement. Maintenance agreement margins can reach 60-70%, making this the highest-margin category in the trades.

Claims Administration: Control vs. Convenience

When a third-party administrator denies or delays a claim, your customer calls you — not them. Choose programs where you either control claims directly or work with administrators with documented fast-resolution track records.

With a TPA, the administrator controls approval, timelines, and coverage interpretations — you have limited visibility over decisions that directly affect your customer relationships. In a contractor-owned model like WarrantyRE's, claims are paid from your reserves and you maintain oversight. WarrantyRE handles the administration, but you control the experience. That distinction protects your brand without adding operational burden.

Compliance, Licensing, and Regulatory Support

Offering service agreements requires compliance with state-by-state service contract regulations. Most states require providers to register, post surety bonds, or maintain reimbursement insurance — requirements most contractors haven't considered before entering this space.

What the Best Programs Provide:

- Company formation and entity registration

- State-by-state service contract filings

- Compliant contract language and disclosures

- Annual renewals and ongoing compliance monitoring

- Tax return preparation and IRS Code 831(b) compliance (for reinsurance models)

Operating without proper registrations exposes you to regulatory penalties and potential contract voidability. Compliance support isn't optional — it determines whether your customer contracts hold up legally.

Sales Enablement and Customer Attachment Rate

The best extended warranty programs include tools and training to help your team sell coverage at the point of installation.

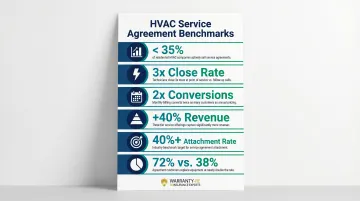

Attachment Rate Benchmarks:

- Fewer than 35% of residential HVAC companies actively sell service agreements

- Technicians who present agreements at point of service close at 3x the rate of follow-up sales calls

- Monthly billing options convert 2x more prospects than annual upfront pricing

- Companies offering three tiers of service capture 40% more revenue than single-option agreements

- Target attachment rate: 40%+ of eligible customers

- Agreement customers have 72% equipment replacement rate versus 38% for non-agreement customers

Look for programs that include:

- Onboarding programs and sales scripts

- Presentation tools and proposal templates

- Ongoing training for technicians and sales teams

Programs that invest in your team's sales capability translate directly to higher attachment rates — and higher profitability.

How We Chose the Best HVAC Extended Warranty Companies for Contractors

We assessed each company on its value to HVAC contractors as a business tool—not on consumer-facing ratings or homeowner reviews.

A common mistake contractors make: choosing programs based on brand recognition or customer-facing coverage terms, without evaluating profit structure or administrative burden.

Evaluation Factors:

- Profit model and contractor income structure — Commission-based TPA versus contractor ownership; who retains underwriting profits and investment float

- Claims administration quality and brand protection — Who controls the claims experience and how quickly claims are resolved; impact on contractor reputation

- Compliance and regulatory support — Company formation, state filings, contract language, annual renewals, IRS compliance

- Program scalability as contractor grows — Whether the program supports small contractors and scales to high-volume operations without switching providers

- Support resources — Staff training, onboarding programs, reporting tools, ongoing optimization

- Financial backing — Whether the program is supported by A-rated insurers with verified solvency

- Long-term equity versus short-term cash flow — Whether the program builds contractor-owned business value or just pays commissions

- Protection from unexpected warranty exposure — Structural safeguards that prevent claims from eroding contractor margins

Each factor maps to a concrete business outcome. Profit retention builds equity. Claims control protects customer relationships. Compliance avoids legal exposure. Scalability prevents costly provider switches as volume grows.

Conclusion

Choosing an HVAC extended warranty partner is a structural business decision — one that shapes customer loyalty, claims risk exposure, and long-term profitability. The gap between a commission-based TPA arrangement and a contractor-owned reinsurance structure can represent hundreds of thousands of dollars in captured profits over time, particularly as your install volume grows and warranty reserves accumulate.

Look beyond customer-facing coverage terms. Before committing to any program, evaluate:

- Who controls claims decisions and approval speed

- Who retains underwriting profits (you or a third party)

- Whether the structure scales with 200+ installs per year

- Whether the program builds equity inside your business

If you're ready to stop sending underwriting profits to third-party warranty companies and build your own program, WarrantyRE has helped contractors nationwide establish and manage administrator-obligor reinsurance companies since 1994. Contact WarrantyRE at (804) 824-9533 or visit warranty-re.com/quote/ to learn how the reinsurance model can work for your business.

Frequently Asked Questions

What is the difference between a manufacturer warranty and an extended warranty for HVAC systems?

A manufacturer warranty (typically 5-10 years on parts, 1 year on labor) comes standard with HVAC equipment and is backed by the brand. An extended warranty or service agreement is an optional contract sold by the contractor or third-party administrator that extends or broadens coverage—often adding labor, refrigerant, and components—beyond what the manufacturer covers.

How do HVAC contractors make money from extended warranty programs?

Contractors earn through two main models. The first is a commission or margin on each agreement sold through a third-party administrator. The second—and more profitable—is owning a reinsurance-backed warranty company, where customer premiums fund the contractor's own entity and unused reserves become profit.

What should HVAC contractors look for when choosing an extended warranty partner?

Start by evaluating profit structure—commission-based vs. ownership—since that determines your long-term upside. From there, look at:

- Claims administration speed and quality

- Compliance support for state service contract regulations

- Sales training and enablement tools

- Whether the program scales with your business and builds equity

Can an HVAC contractor own their own warranty company?

Yes. Through an administrator-obligor reinsurance structure, HVAC contractors can establish their own warranty company backed by A-rated insurers—allowing them to capture underwriting profits, control the claims experience, and build a business asset rather than paying margins to a third-party provider.

How do reinsurance-backed warranty programs differ from standard third-party programs?

With a standard third-party program, contractors earn a commission on each agreement sold—but the administrator keeps the underwriting profit. A reinsurance-backed structure flips that model: contractors own a captive warranty company funded by customer premiums, retaining unused reserves as profit and controlling the entire claims experience.

How does an HVAC extended warranty protect a contractor's business?

Extended warranties shift the financial risk of post-install failures—especially costly callbacks and labor-intensive repairs—off the contractor's books. A reinsurance model goes further: customer premiums fund a reserve that absorbs claims costs, protecting cash flow while building a long-term business asset.